Transcript: Temasek Review 2023 Media Conference

The following is transcript of the Presentation of the Temasek Review 2023. The text should be read in conjunction with the slides shown in this transcript. It has been edited from delivery only for readability.

To refer to a selected transcript of the Question & Answer session which followed, click here.

To see all of the key financial metrics and diagrams in the 2022 Temasek Review, please click here.

Lena Goh:

Good afternoon everyone.

Welcome to Temasek Review 2023!

I am Lena Goh from Temasek and I will be your host for today.

Our theme for this year is “Our Compass in a Complex World”.

Our panellists for this year include our CEO, Dilhan Pillay, our deputy CEO Chia Song Hwee, our CIO Rohit Sipahimalani and our CFO Png Chin Yee.

Before that, I would like to share three key points with you.

- The data that will be presented is for our financial year ended 31 March 2023.

- All currencies quoted in today’s briefing will be in Singapore dollars unless otherwise stated.

- Also, all information is embargoed till 4pm Singapore time today.

For those online, if you experience any technical issues, please reach out to us via the Whatsapp hotline that has been shared with you.

A recording of this media briefing will also be made available online after the session.

Before Chin Yee starts her presentation on our performance results, let us kick off with a short video recapping our year in review.

Png Chin Yee:

Good afternoon everyone. My name is Chin Yee.

As you can see, the theme for this year’s Temasek Review is

‘Our Compass in a Complex World’.

Today, we will be sharing with you our performance

and our T2030 strategy

which will guide us towards our Purpose,

- So Every Generation Prospers.

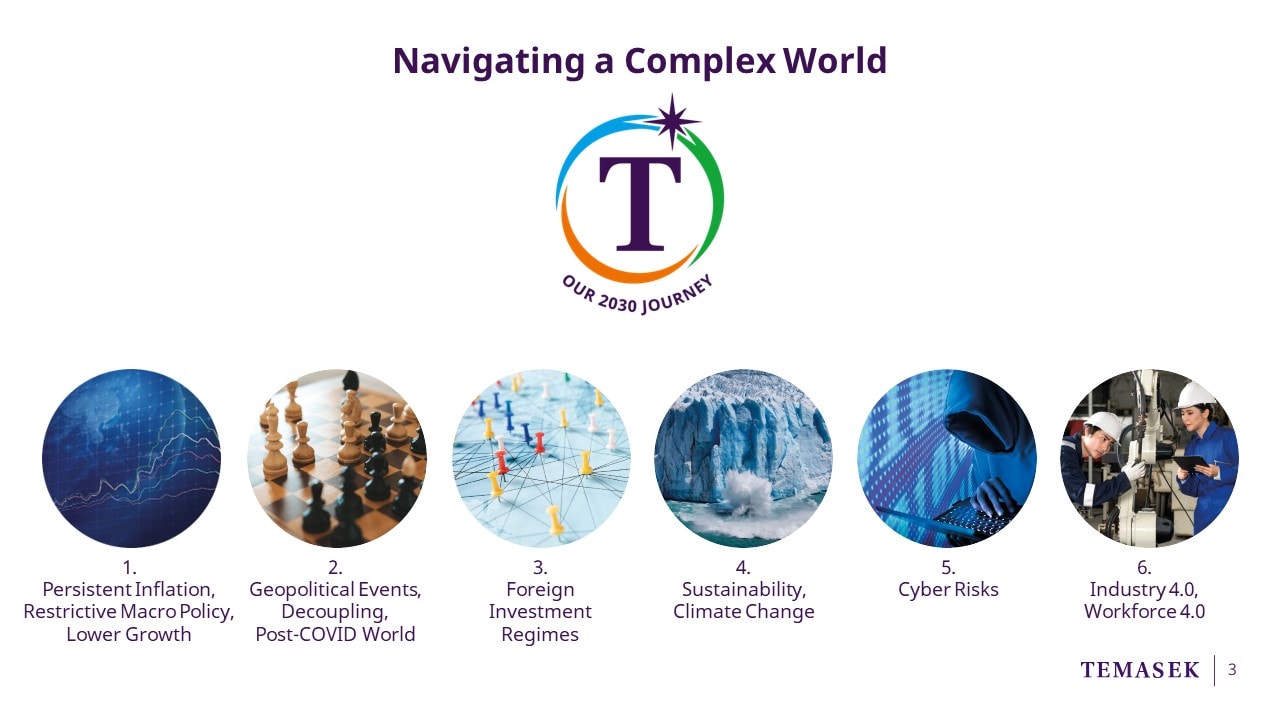

You can see on this slide six top-of-mind issues

that we see as key challenges in the decade ahead.

For the first time in a long time,

we are seeing persistent inflation

and tighter monetary conditions

manifesting themselves in higher interest rates,

leading to potentially lower real returns.

Stagflation, a phenomenon that the world

has not seen since the 1970s,

remains a risk.

The US-China rivalry has now become wider.

What’s happening in Ukraine,

has an impact on food and energy security,

and also the future of Europe.

Reconfiguring supply chains from

"just in time" to "just in case”

will add to inflationary pressures.

We’ve seen a proliferation of

foreign investment regimes and restrictions

that has impacted the investment climate.

Trade restrictions will also lead to global output losses,

which will be felt most acutely by developing economies.

The climate crisis is increasing in urgency.

Businesses have to pivot towards sustainability.

Additionally, as the world

becomes more dependent on technology,

cyber risks have heightened

and cyber resilience is ever more critical.

The advent of Industry 4.0 and industry 5.0, with human-AI interactions,

has social, economic and political consequences,

which requires businesses and their workforce to transform themselves.

Against this backdrop,

the challenge for us at Temasek

is to chart a steady course in the decade ahead.

Rohit will be taking you through our outlook and investment stance,

and Dilhan will share our T2030 strategy.

Before that, let me take you through our performance.

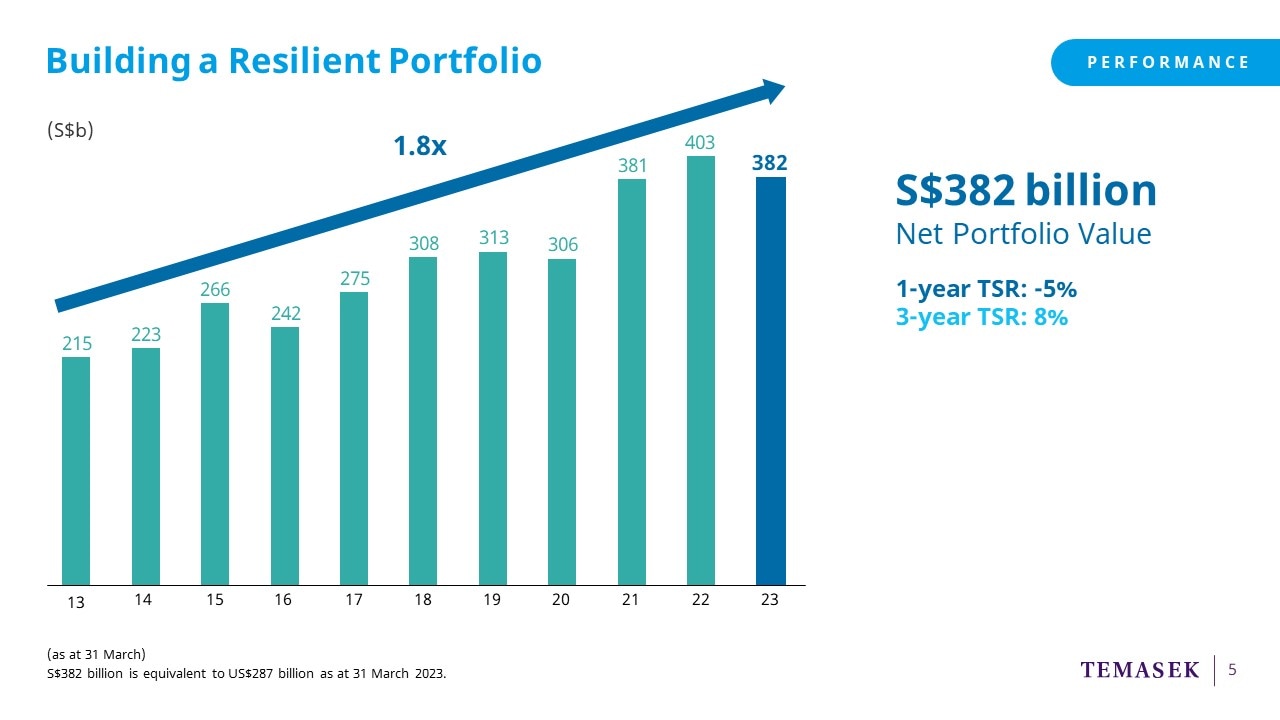

We ended the financial year with a Net Portfolio Value

of 382 billion dollars.

That is 1.8x of our portfolio value in 2013.

Our 1-year total shareholder return was negative 5%.

This was largely due to a fall in equity valuations,

both in the public and private markets.

Our Singapore portfolios have remained resilient

but our global investments saw a reversal of gains

from the high valuations in the last 2 years,

as higher interest rates drove valuations lower,

particularly in the Technology, Healthcare, and Payments space.

Despite the de-rating in valuations,

our portfolio value has sustained its recovery from the lows during COVID,

with a 3-year TSR of 8%.

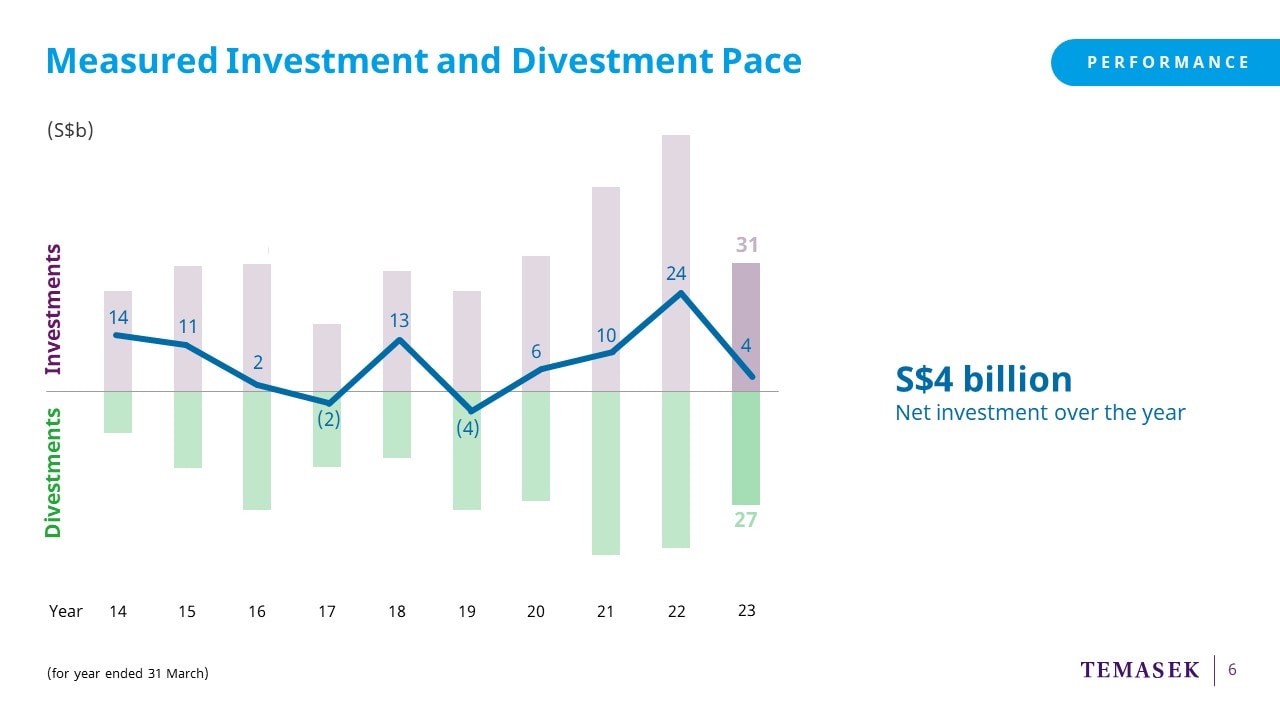

We adopted a cautious approach amidst the global uncertainties last year

and slowed down our investment and divestment pace.

We also saw deal activity globally slow, as liquidity tightened.

We invested 31 billion and divested 27 billion,

resulting in a net investment of 4 billion dollars.

This compares to our net investment of 24 billion dollars

in the prior financial year.

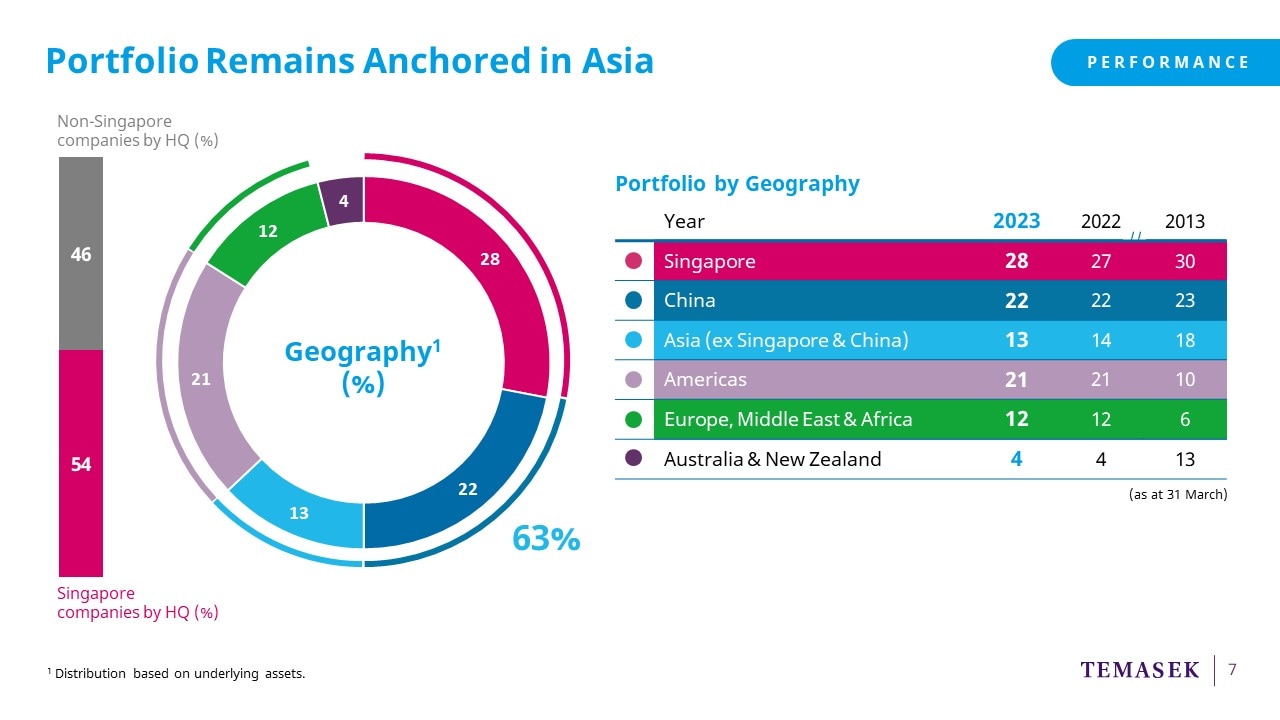

This slide provides a view of our portfolio by geography

based on our underlying exposure.

So while Singapore companies made up 54% of our portfolio,

if you look at the bar in pink,

you will see that by underlying assets,

Singapore represents 28% of our exposure

that is because many of our Singapore companies

have extensive businesses outside of Singapore.

We remain anchored in Asia,

with almost two thirds of our portfolio based in this region.

Singapore remains our largest market,

followed by China and the Americas.

As you can see, our exposure outside of Asia

into the Americas and Europe

has more than doubled over the last decade.

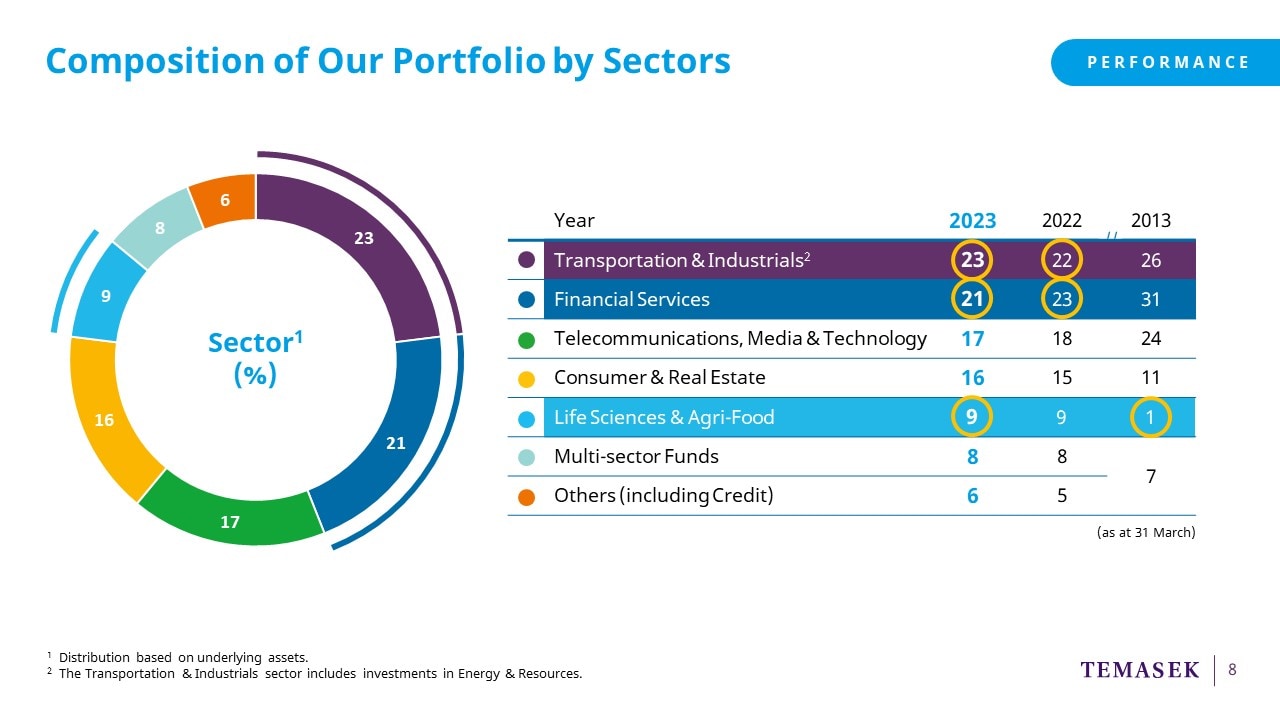

Looking at our portfolio composition by sectors.

Transportation & Industrials and Financial Services

are our two largest sectors.

Our exposure to Transportation & Industrials have

increased this year due mainly to our investment

into UK-based Element Materials Technology.

Our exposure to Financial Services fell slightly,

due to net divestments and a decline in market value,

particularly of our payments portfolio.

Compared to a decade ago,

our sectoral composition has evolved.

Our Life Sciences & Agri-Food portfolio, for example,

has grown from 1% to 9%.

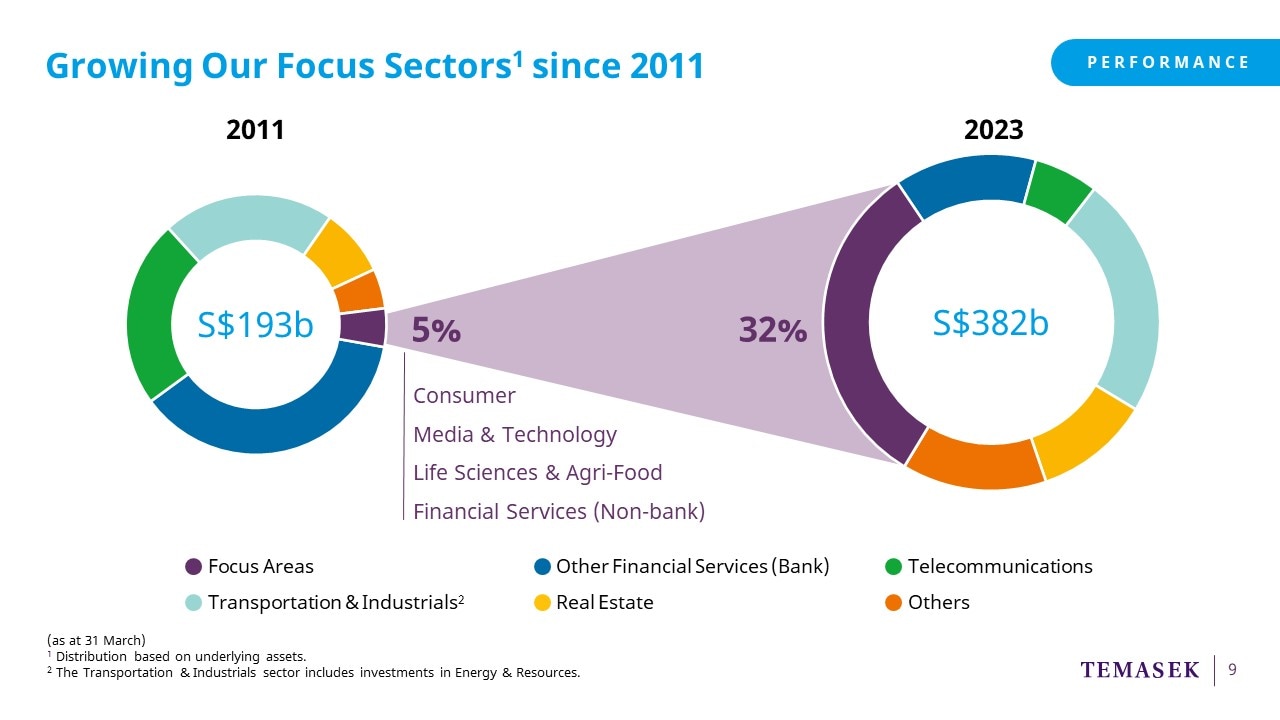

Let me share a little more about how the portfolio has evolved.

In 2011, we identified focus sectors

which would benefit from longer term and emerging trends.

These included Consumer, Media & Technology,

Life Sciences & Agri-Food and

Non-Bank Financial Services.

Here, in purple, you can see they’ve grown

from 5% to 32% of the portfolio.

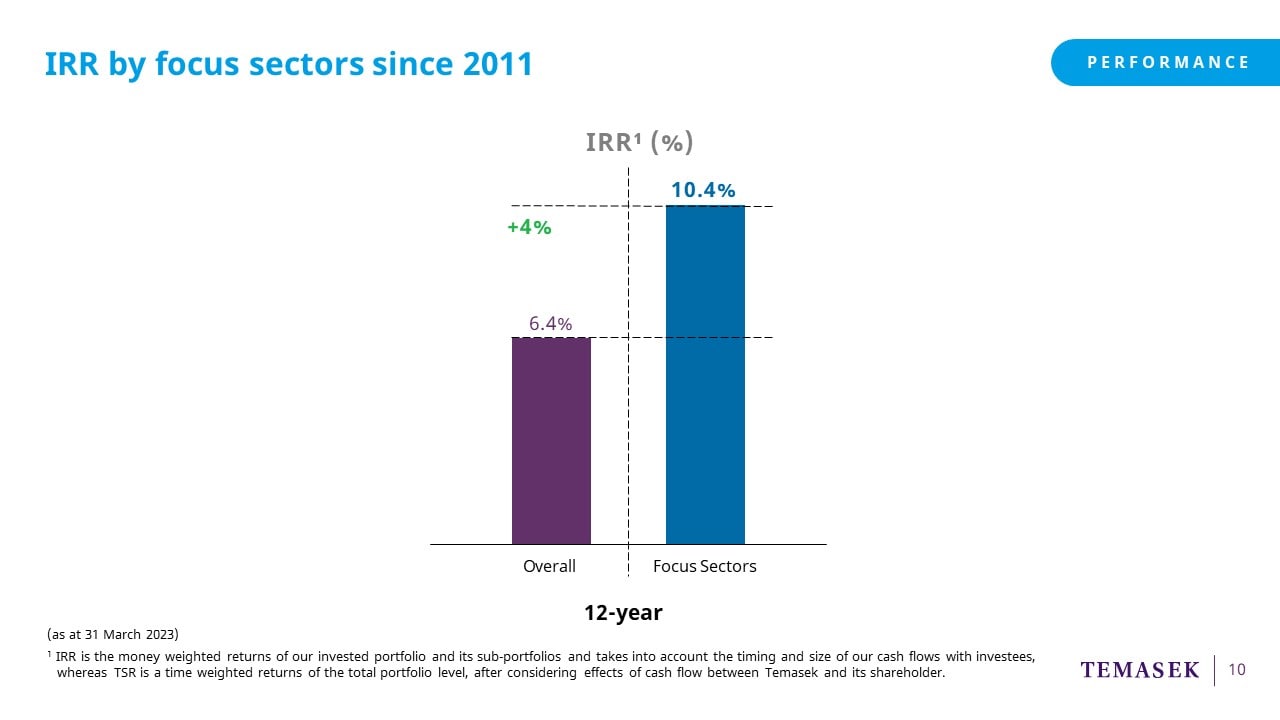

The focus sectors have generated better returns for us.

Since 2011, the returns of our focus sectors

have outperformed our overall portfolio by about 4 percentage points.

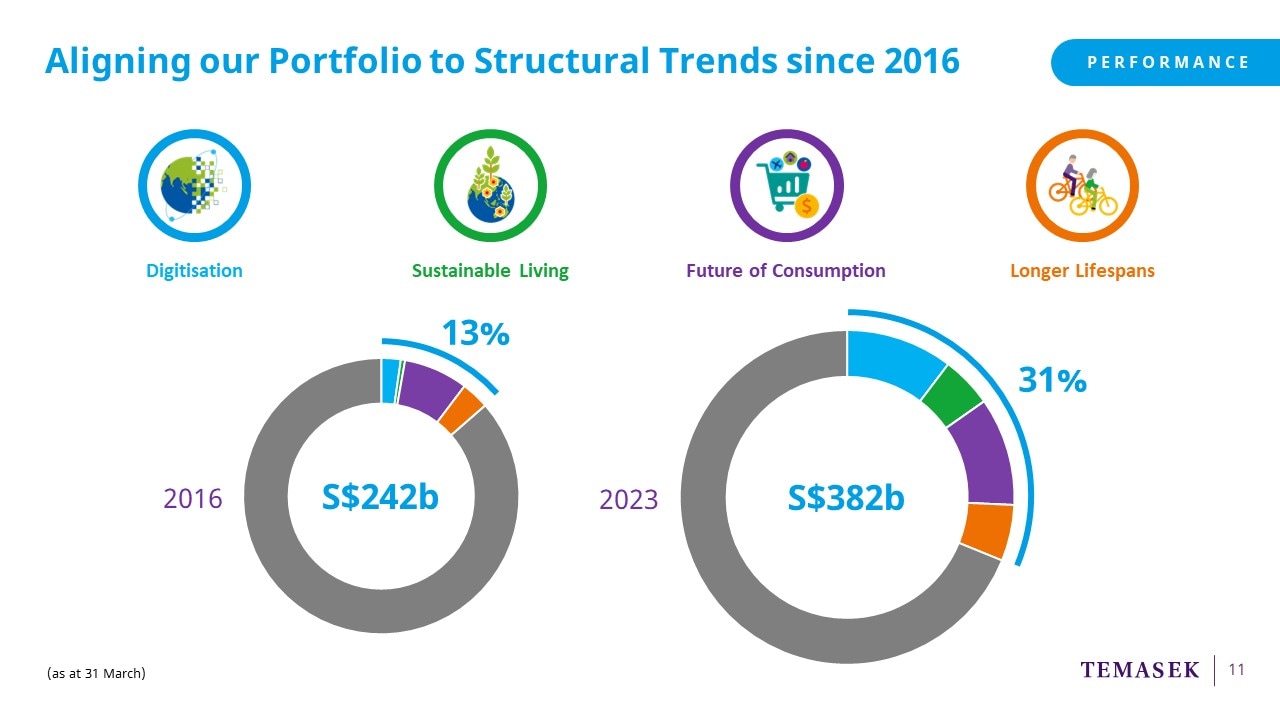

Learning from this,

we refined our areas of focus.

In 2016, we identified structural trends

that guide our portfolio construction, as we look

to build a portfolio that is resilient to shocks

and relevant for the future.

Digitisation and Sustainable Living

have a pervasive impact across all sectors and business models.

Future of Consumption and Longer Lifespans

reflect shifts in consumption patterns,

and also addresses the needs of a growing and aging population.

In 2016, investments aligned to these trends accounted for about 13% of our portfolio.

Today, they account for 31%.

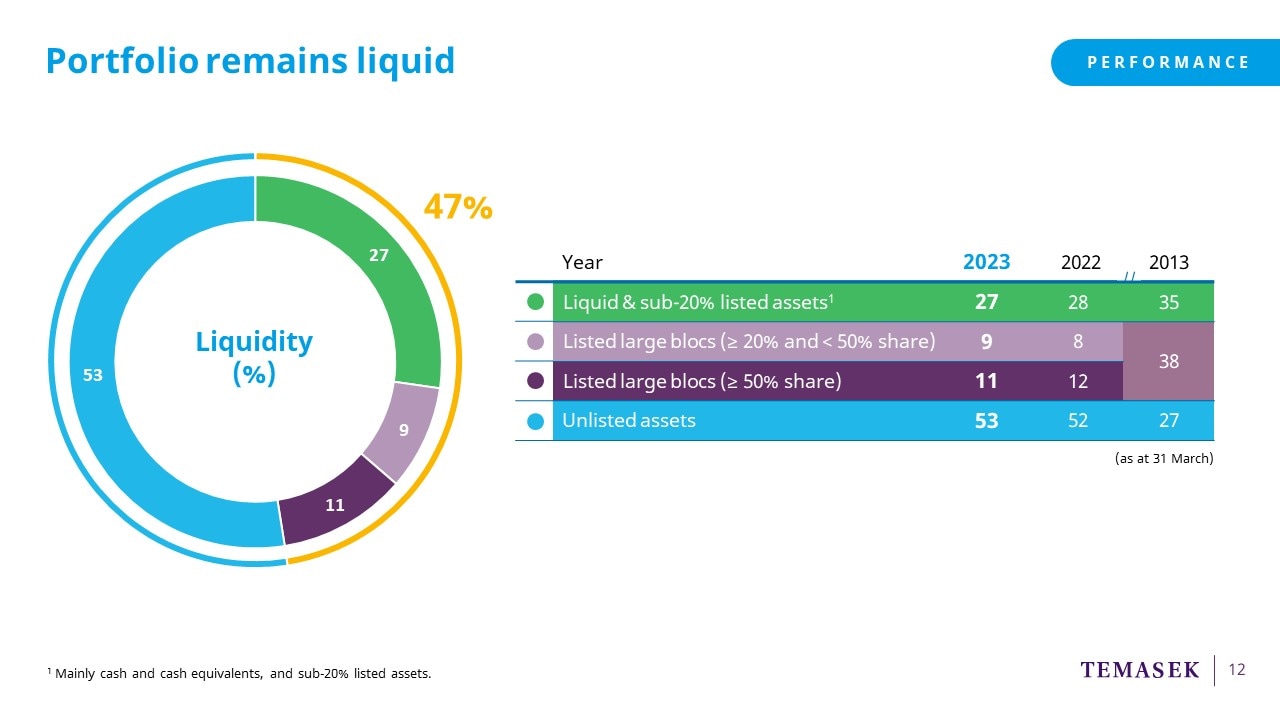

Let me now turn to the liquidity profile of our portfolio.

Our portfolio remains liquid.

47% of our portfolio is invested in liquid and/or listed assets.

Unlisted assets made up 53%.

The unlisted portfolio has benefitted from increase in the value of the portfolio, but we have also found opportunities to invest in attractive opportunities in the private space.

Our unlisted assets do provide liquidity

through dividends, distributions and divestments.

We also achieve liquidity when these companies list.

For example, in the last five years, some of our holdings, such as

Adyen, Meituan, and Roblox have been listed with significant value uplift.

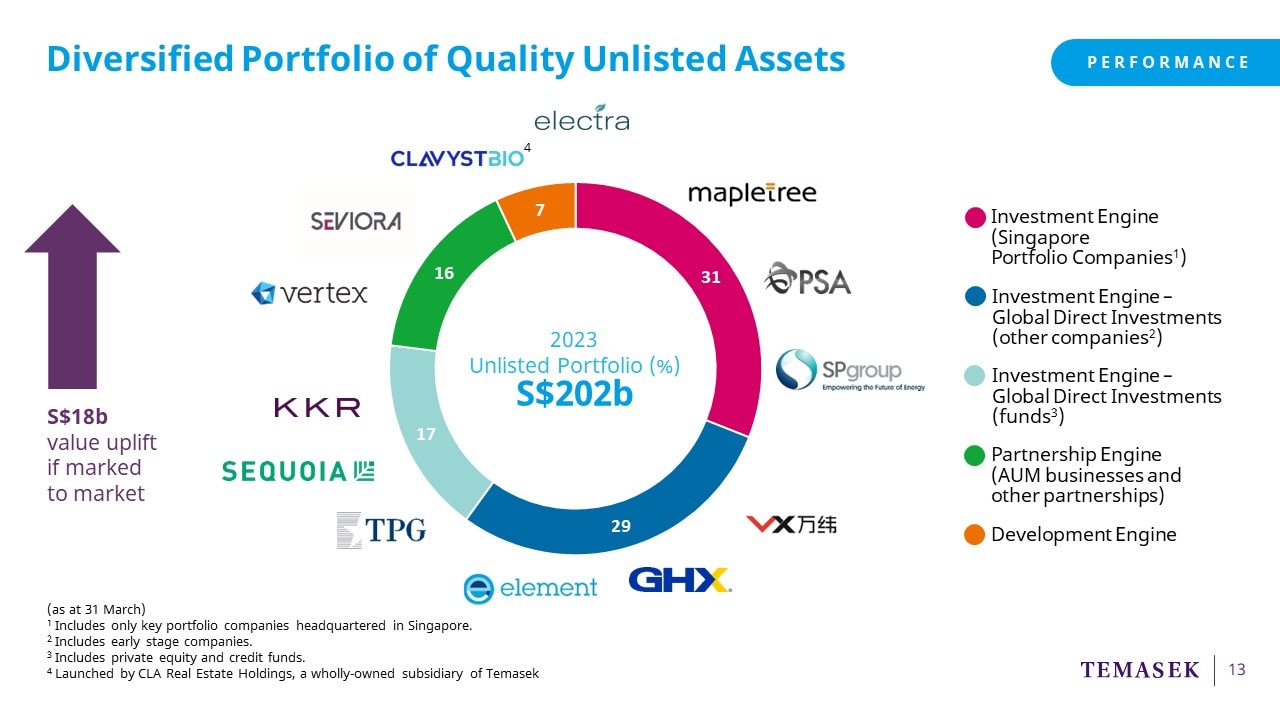

Let me share a little more about our unlisted portfolio.

Here, you can see a breakdown.

We value our unlisted investments at book value less impairment.

But if we were to mark it to market,

it would provide an uplift of about 18 billion dollars to our portfolio.

In pink, we have our Singapore companies,

which make up about a third of our unlisted portfolio.

In dark blue, our direct investments into other private companies,

including the early stage companies.

In light blue, our investments in third party funds.

Investing in funds enabled us to gain insights into

new sub-sectors, new markets,

and also provided co-investment opportunities.

In green, we have our asset management businesses and other partnerships.

Our asset management businesses manage about $80 billion in assets. That includes our assets, but also third-party capital.

And lastly, our Development Engine is in orange.

These include longer gestation investments in new promising areas.

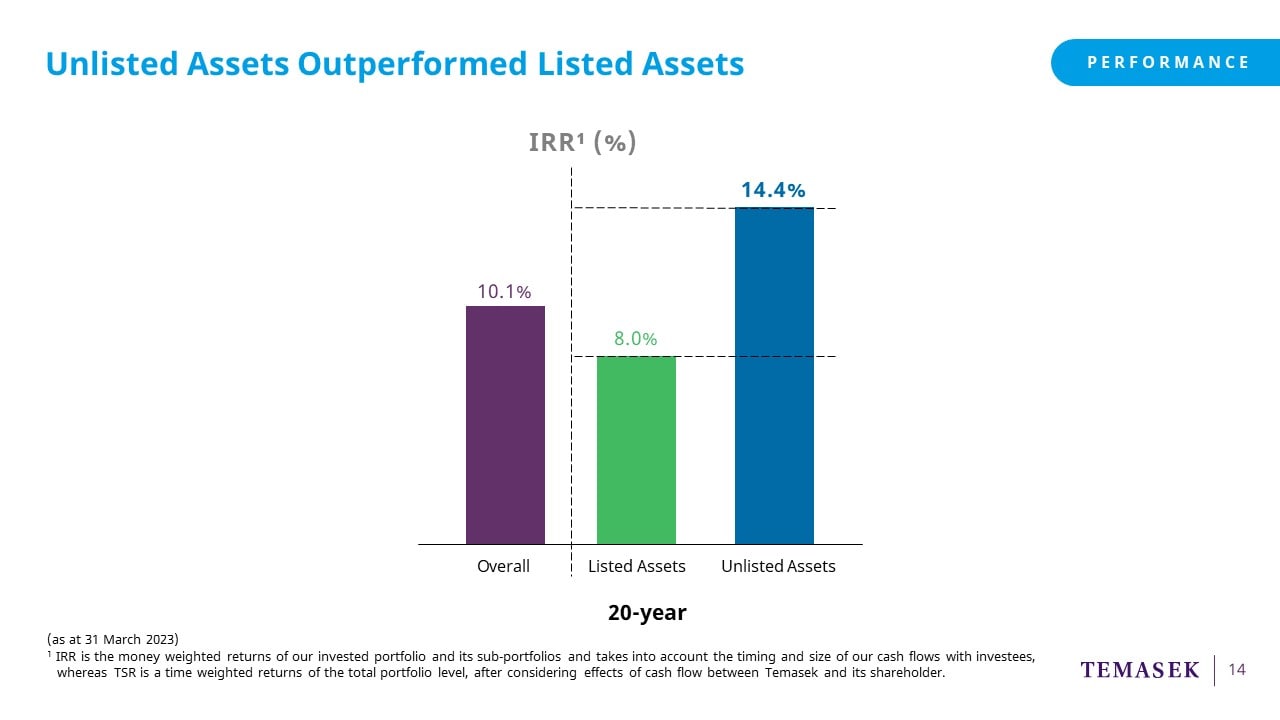

Our unlisted assets

have generated good returns for us consistently.

You can see here that over the last 20 years,

returns of our unlisted assets

have outperformed our listed ones.

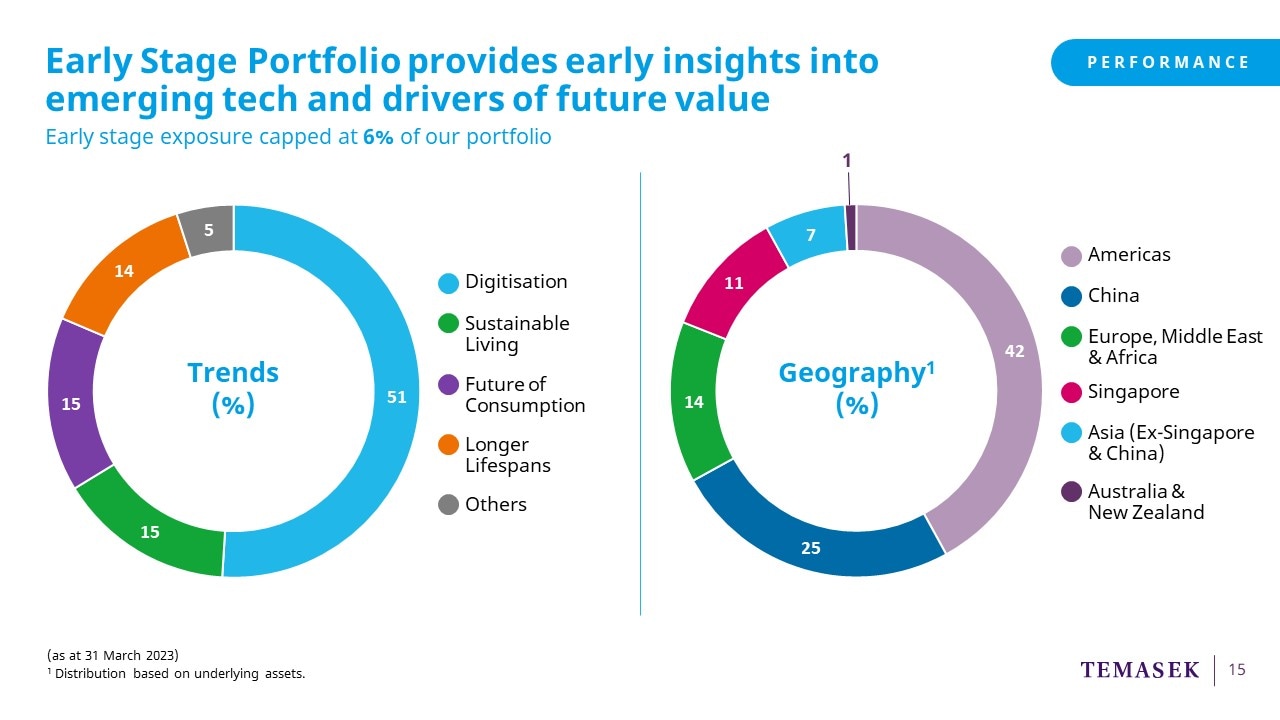

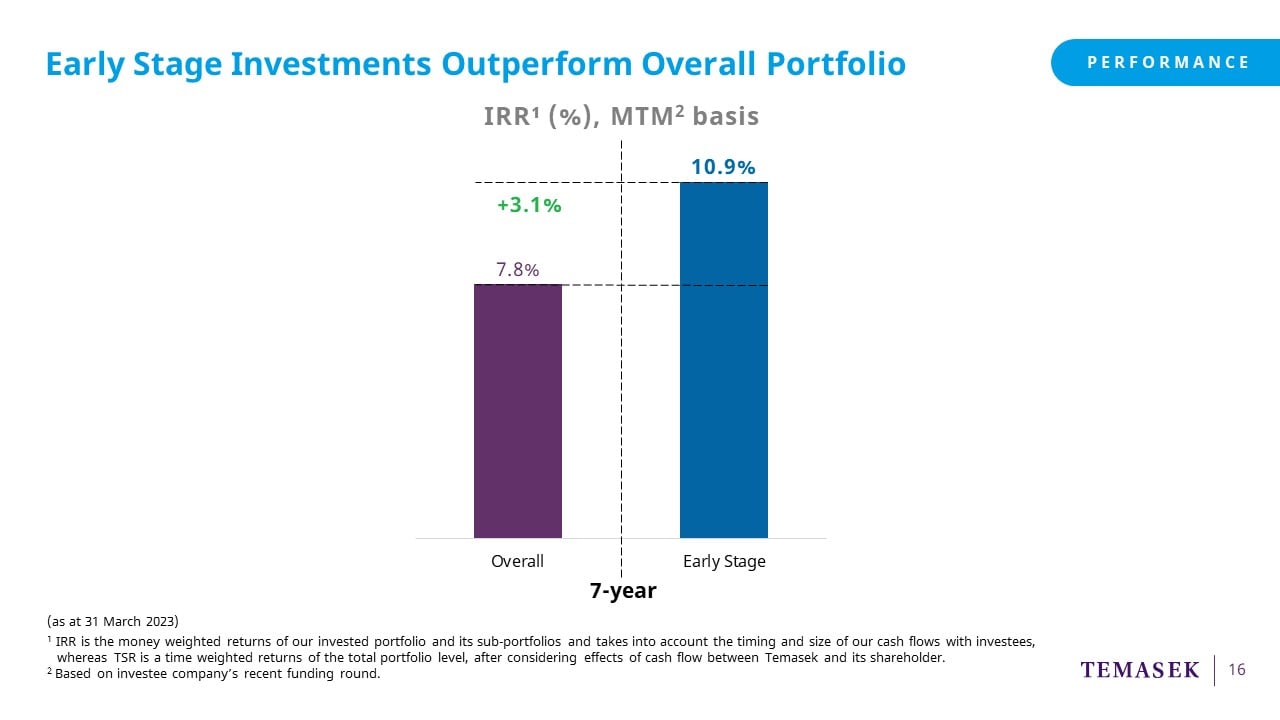

Some of you have asked about our early stage portfolio.

We invest in early stage to identify trends of the future,

and to gain insights into emerging technologies and business models.

This allows us to invest in winners early

and double down, as these companies scale,

and drive future value.

This also allows our portfolio companies to track developments in

new technology and business models,

and this helps them to stay relevant.

To manage the higher risks that come with our early stage companies,

we cap our exposure to this segment to 6% of the portfolio.

On the left, you can see, most of our early stage investments

are aligned with our four structural trends.

On the right, you will see that the portfolio is well diversified,

with 42% in America,

followed by 25% in China;

this excludes previously early stage investments

in China that have since matured,

for example, Meituan and Alibaba.

From this, you can see that early stage companies

may mature into successful growth stage companies. They may list, and generate good returns for us.

Our early stage returns since 2016,

when we stepped up this strategy,

has exceeded that of our overall portfolio.

Further,

when marked to market for comparability to industry benchmarks,

our early stage investments

have generated returns above industry averages.

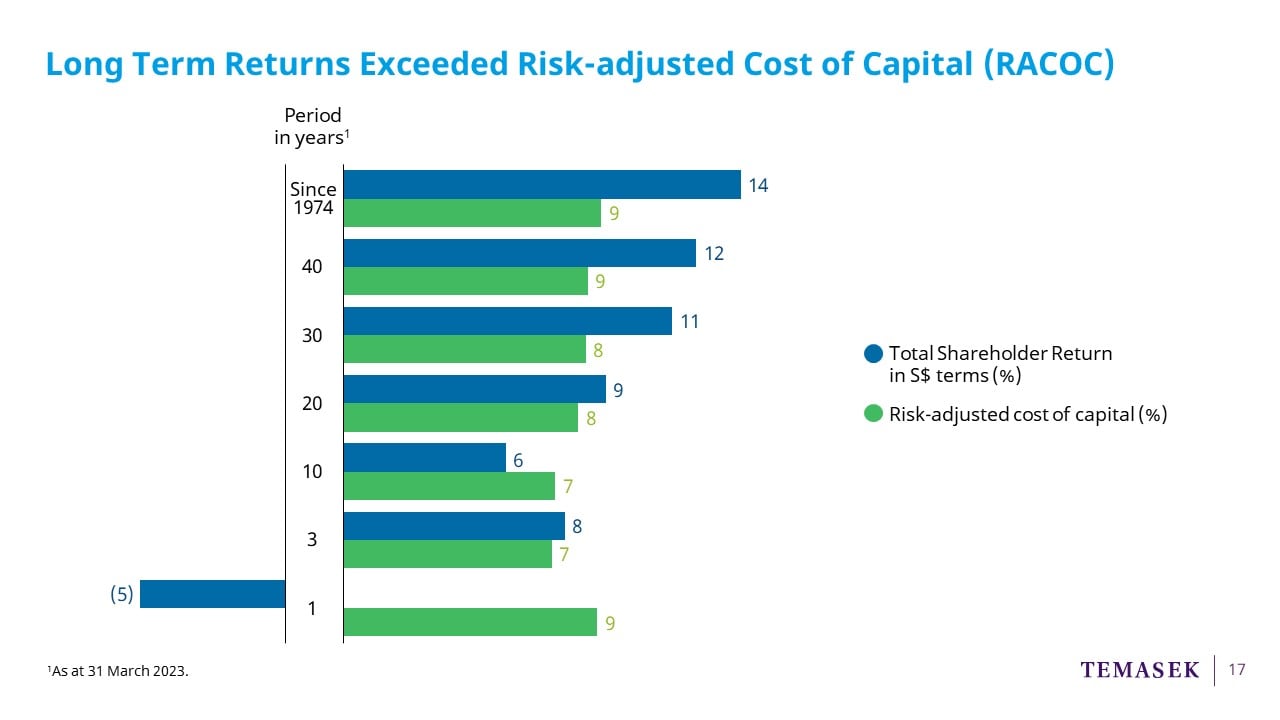

Stepping back to look at our overall performance.

We measure our returns over the long term

against our overall risk-adjusted cost of capital.

Our cost of capital this year has increased,

due to increase in interest rates.

As you can see from the blue bars,

our long term returns have generally exceeded our cost of capital,

as shown by the green bars.

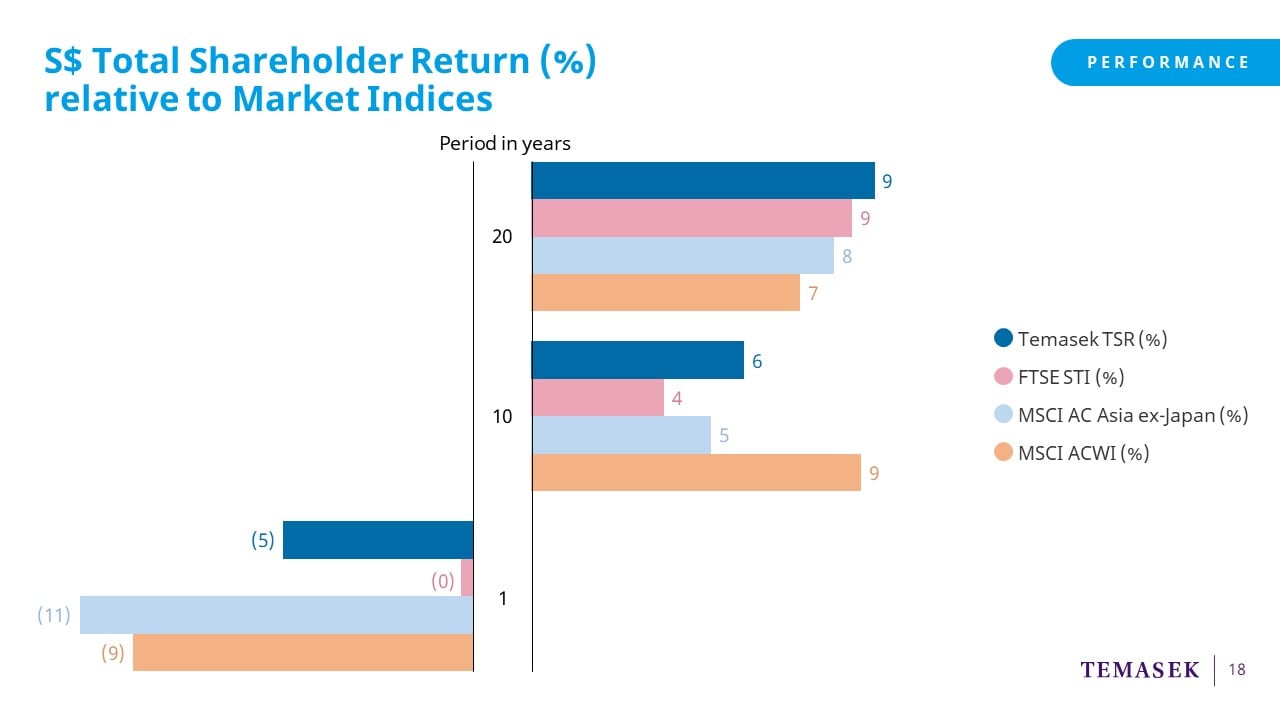

You would know that we don’t manage our portfolio to benchmarks.

But some of you have found market index performance

a useful reference point.

This slide shows you our TSR in dark blue against

the STI in pink

MSCI Asia ex Japan in light blue and

MSCI AC World in orange.

As you can see,

we have outperformed the indices

in the 20-year period.

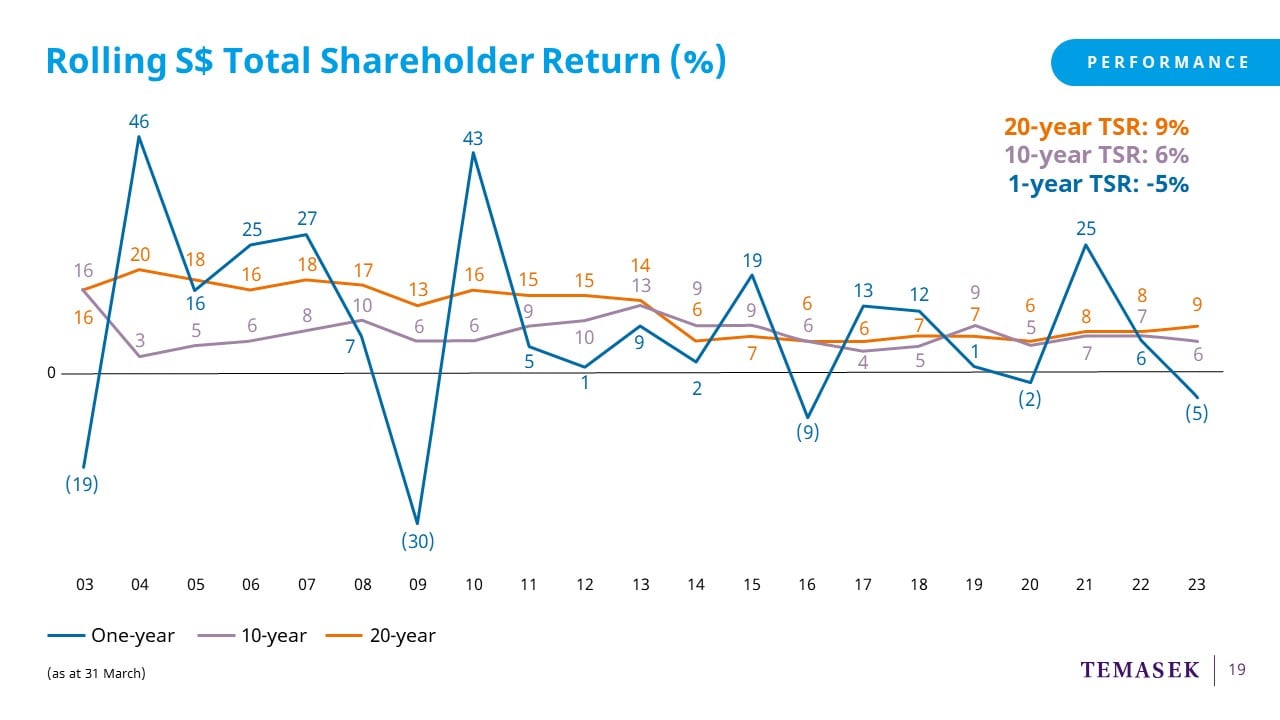

This chart shows our TSR over the last two decades.

You can see from the blue line, which shows our one-year TSR, that as a predominantly equities-based investor, we are not immune to year-to-year market volatility.

But as a long term investor,

we are prepared to weather short term volatility in our performance.

The purple and orange lines,

represents our longer term 10 and 20-year TSRs,

which stood at 6% and 9% respectively.

You can see that these are more stable

and representative

of our performance.

In summary,

while our performance has been impacted by challenging markets,

we continue to evolve our portfolio

to be resilient and forward looking.

We ended the year in a net cash position,

which gives us flexibility to take advantage of the opportunities ahead.

I will hand over the time to Rohit,

who will take you through our outlook.

Rohit Sipahimalani:

Good afternoon. My name is Rohit, and I will be taking you through our global outlook and investment stance.

The global economy is still quite fragile.

Geopolitical tensions are high

and are showing no signs of easing.

Inflation is elevated in most developed markets,

which is causing most central banks

to maintain tight monetary policy.

Growth is also slowing with tighter credit conditions.

There is a risk of a recession in key developed markets. I know we and everyone else has been saying this for a while now. It is the most anticipated recession which still has not happened.

But we do believe that to keep inflation under control, we probably will need to see a recession, although the timing for that is uncertain.

Having said that, there are still some bright sparks.

The most significant of them in recent months has been

in generative AI, which is going to have a significant impact on productivity,

change and reshape many industries,

as well as drive innovation.

It, however, will also have significant societal implications, which both companies and governments

will need to deal with over the next few years.

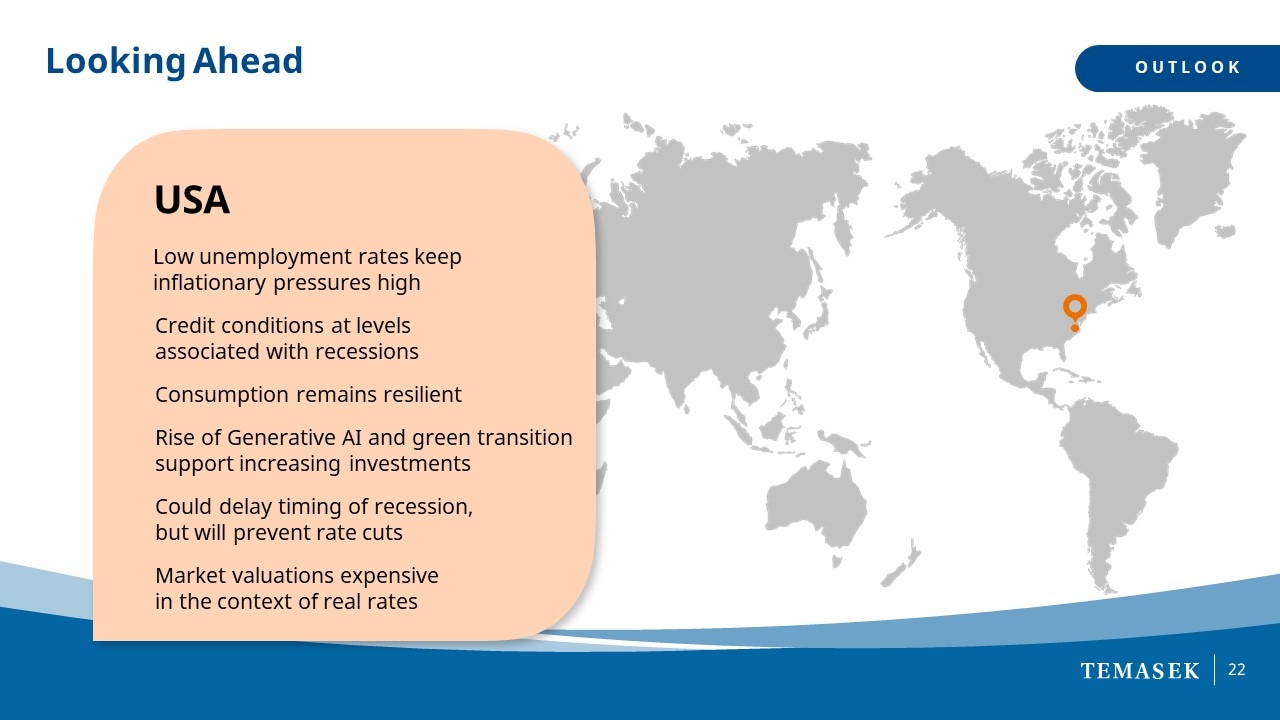

In the US, we are seeing tight credit conditions and restrictive monetary policy. Both of these are strong headwinds to growth.

This could lead to a recession sometime in the next few quarters,

even though I know it is not imminent right now.

Unemployment in the US is close to all-time lows.

That is creating inflationary pressures and

will make it difficult for the Fed to cut rates this year, unless we see a recession.

Bank lending conditions have also tightened meaningfully,

especially after the regional banking crisis in March.

Credit conditions are at levels that you normally associate with recessions.

However, we see consumption still very resilient in this environment, and that is because people still have jobs.

Companies prefer to reduce hours worked,

rather than lay off people. This is improving consumer confidence, encouraging them to spend the excess savings that they still have left over from the pandemic.

The biggest surprise in the last few months

has been Generative AI, which has pushed the S&P500 into a bull market.

The wealth effect from that rally also adds to consumer confidence and spending.

AI should also lead to an increase in investment activity.

As you know, every board is asking their management what they are doing to invest in AI. We should also see fiscal policy in the US supporting investment spending.

For example, you have got industrial policies like the IRA, which is leading to significant investments in the green transition.

All these factors could prop up growth and delay the timing of any recession,

but it also means inflation is likely to remain stubbornly high,

which will require the Fed to keep pushing up rates,

or at the minimum, preclude any rate cuts.

With that context, we find current valuations of the S&P500 at 19x P/E

very expensive, especially when you have real rates today at 1.7 to 1.8%.

Just for context, in the decade before COVID-19, from 2010 to 2019, the average S&P500 P/E was 15x and real rates average of only 0.4%.

This is something we are very conscious of, as we evaluate opportunities in the US.

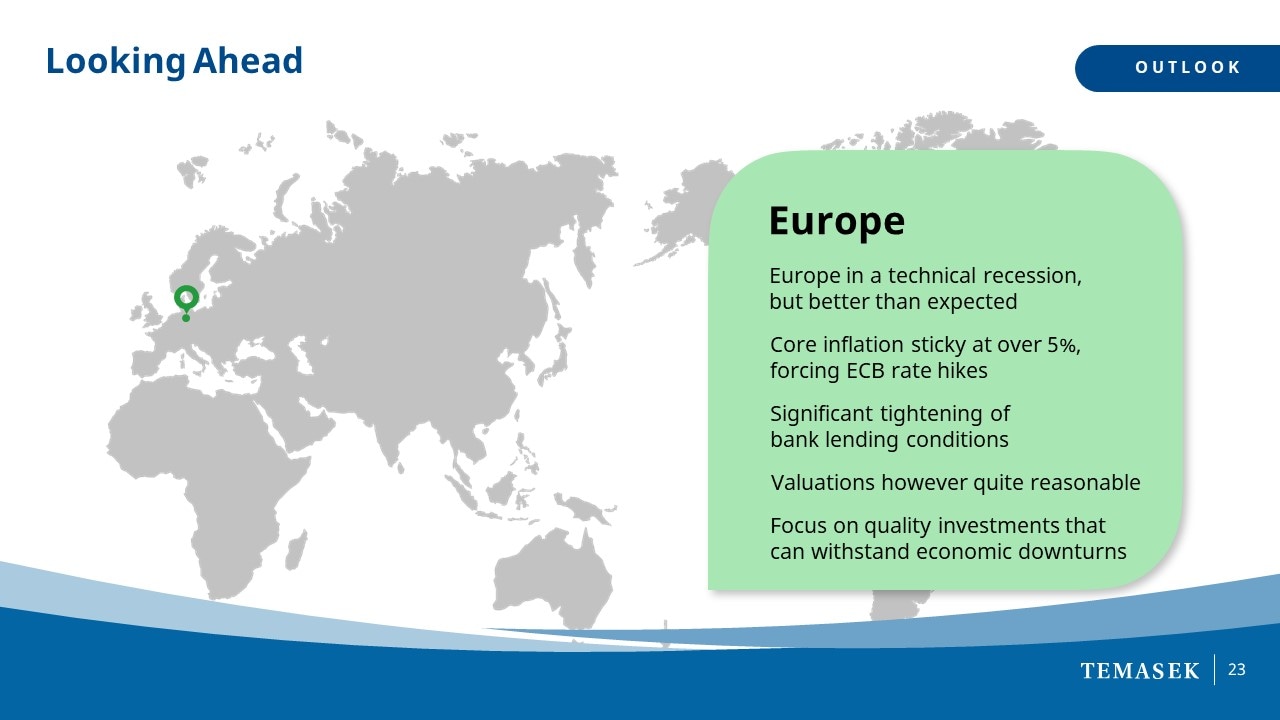

Europe is already in a technical recession,

having had 2 quarters of -0.1% GDP growth.

However, the growth outlook and the growth we have actually seen has been much better than what anyone expected,

largely because of the 80% fall in gas prices since Q4 2022,

and the reopening of China earlier this year.

However, inflation is very sticky at over 5%, and that means that the ECB will have to keep hiking rates until they see a significant slowdown in growth.

We are also seeing a significant tightening of credit conditions.

ECB Bank Lending Survey showed credit conditions to be the tightest we have seen since the GFC.

However, valuations in Europe are still quite reasonable, at around 12x our earnings, slightly below historical averages, and that is what makes the risk/reward more balanced in Europe.

From our perspective, we continue to see opportunities to invest

in high quality companies that are global in nature, that can withstand economic shocks and also companies in Europe that will benefit from the green transition.

China is at the complete other end of the economic cycle.

It is coming into a cyclical recovery out of COVID,

but the pace of recovery is slower than expected.

China seems to be on track to achieve its 5% GDP growth target for this year,

but could fall short of market expectations which are for higher growth.

We started the year, Q1, quite promisingly with a COVID reopening bounce.

But we have seen momentum slow down meaningfully in the last quarter.

Property sales have fallen, infrastructure spending has slowed, and exports growth have slowed.

The only engine we need to rely on to achieve the growth targets for this year is consumption, and that too, the lack of job opportunities has been impacting consumer confidence and holding back spending.

There are expectations that the government will provide stimulus to step up growth like they have done in the past. While you see some signs of that, we expect that the stimulus this year will be much lower and much more modest than what you have historically seen.

This calibrated growth outlook is already being reflected in market valuations.

MSCI China is trading at less than 10x P/E,

which is more than 1 standard deviation below historical averages.

While uncertainties exist for long term investors,

there will continue to be opportunities to invest in China

in either areas of domestic consumption

or other sectors, where China has leadership.

For example, EVs and the entire supply chain.

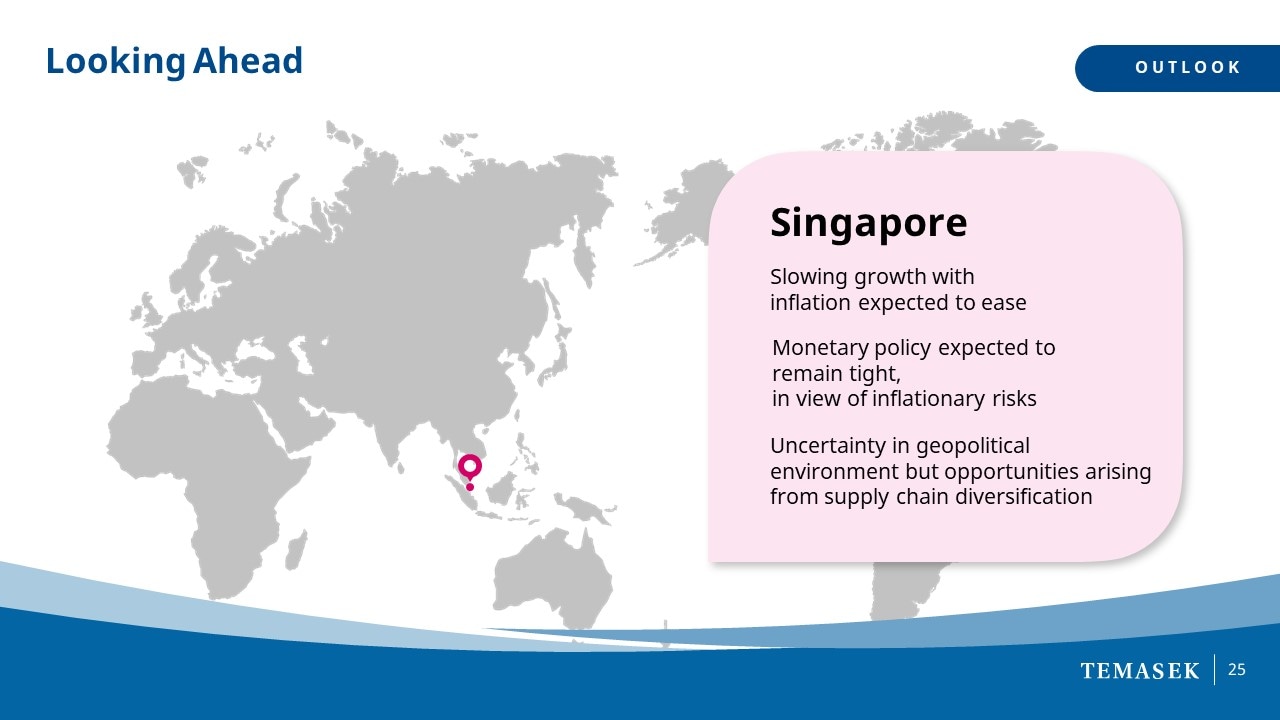

Now coming to Singapore, Singapore as you know is a very open country,

and so when you have a global growth slowdown, Singapore always gets impacted, and we are seeing that today.

Inflation is also high, and while we expect it to moderate over the course of this year, thanks to a stronger Singapore dollar, it is likely to be elevated compared to history.

There are also risks from geopolitics, but that also provides opportunities,

as people look to diversify supply chains around the region.

Given these macro uncertainties,

we have moderated our investment pace,

and have adopted a more cautious stance.

However, as Chin Yee pointed out, we have a lot of liquidity.

We are ready to step up our investments

in cases where there are market dislocations.

We are also ready to step up our investments if we see specific

opportunities aligned to our long term portfolio construction objectives.

We will continue to invest in line with our four major trends,

which are even more relevant today in a post-COVID environment,

and contribute to the resilience of the portfolio.

However, compared to the past,

there are a few changes and a few additional factors to look at while making investments:

First, we need to apply a geopolitical lens to all our investments.

For example, we wouldn’t invest in areas

that are in the cross hairs of US China tensions.

Similarly, in a fragmented world,

we prefer investing in companies that have access to large domestic markets.

Secondly, we have to be prepared for an environment of higher inflation

and higher interest rates that requires us to invest in companies which have strong pricing power.

We will have also increasingly favoured companies that have strong cash flows compared to the past.

Finally, we need to look at AI and the green transition and the impact of that on all our investments, both existing portfolio and new opportunities.

With that, I will hand over the time to Dilhan, who will talk about our Temasek 2030 strategy.

Dilhan Pillay:

Good afternoon everyone.

I’m Dilhan and I am here to present to you our T2030 Strategy.

To know where we are heading,

we must know where we have come from

and the journey we have taken to be where we are today.

As with everything that is sustainable for the long term,

T2030 is evolutionary.

Our objective is to deliver a resilient and forward looking portfolio in 2030,

that will generate a return above our risk-adjusted cost of capital,

which today hovers around 9%, compounded through to the end of this decade.

I will explain over the course of the presentation how we will get there.

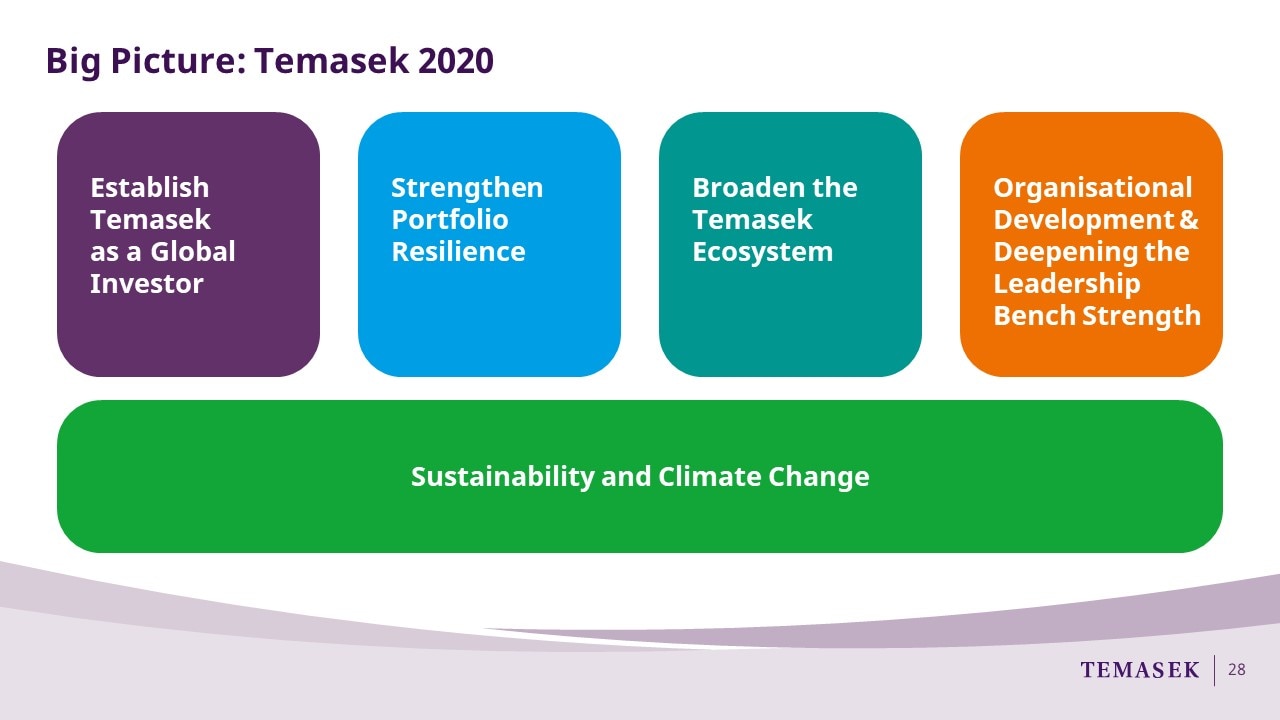

T2030 builds on the foundations that have been laid by T2020.

And so, I thought I should share a bit about T2020,

and how we have performed according to the objectives we had set for ourselves back in 2011.

T2020 was launched in April 2011.

The objective was to become a global investment house by 2020,

with the clear expectation that we would have to brave new frontiers and overcome new challenges along the way.

It was launched against the backdrop of a world emerging from the GFC;

Europe being ensnared by the economic crisis enveloping the PIIGS countries (Portugal, Italy, Ireland, Greece and Spain); the BRICS countries (Brazil, Russia, India, China, South Africa) still seen as emergent;

and the belief that emerging markets will continue to bring higher returns.

The 4 Pillars of the T2020 strategy were:

First, Establish Temasek as a Global Investor.

Second, to Strengthen Portfolio Resilience. To build a quality portfolio tapping on trends, such as transformation of economies, improving demographics and the advent of technology.

Third, to Broaden the Temasek Ecosystem, by establishing new platforms to enhance operational synergies, as well as to develop a wider partnership ecosystem.

And finally, Organisational Development and Deepening the Leadership Bench Strength, bringing in talent with new capabilities and renewal.

Sustainability and Climate Change was an add on that we believed we should pay attention to.

We should be cognisant of the issues in the decade ahead.

Our aim was to keep pace with innovation and the new solutions.

We achieved our goals.

In the decade prior to 2011, we grew with emerging Asia – Singapore and Southeast Asia, China and India.

Our exposure to the US and Europe was not significant.

We broadened our footprint opening our offices in the US and Europe in 2014, and today we have 6 offices across both continents.

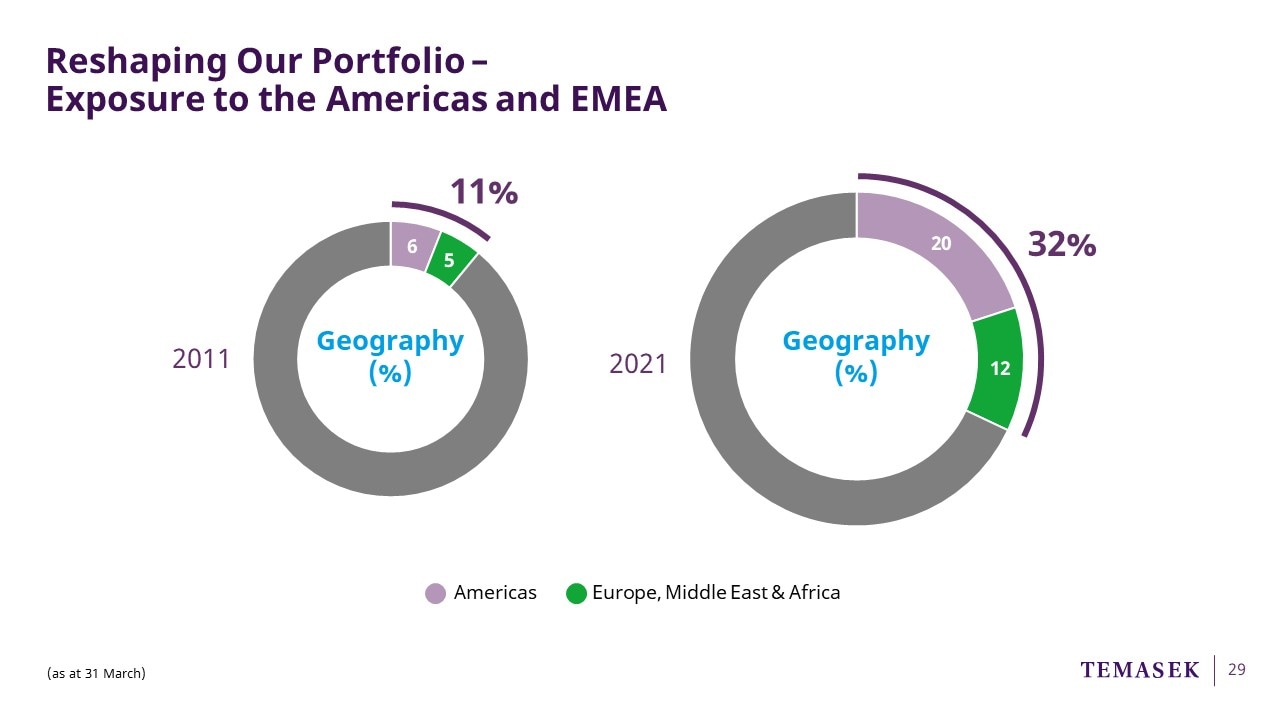

Our Americas and EMEA exposure in 2011 were a combined 11%,

or approximately $21 billion in 2011.

By 2021, it was 32%, which was $122 billion, or roughly 6 times of what it was in 2011.

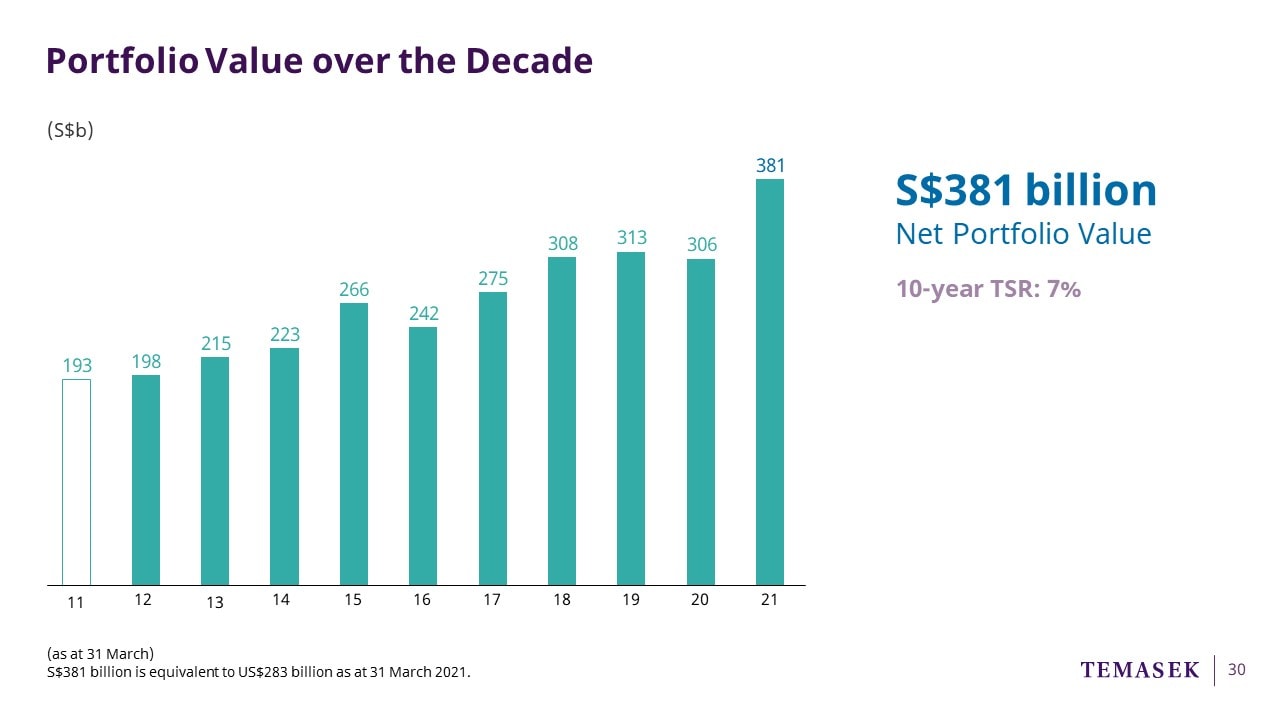

We started T2020 with a net portfolio value of S$193b dollars,

and ended the decade with an NPV of S$381b,

for a compounded annual TSR of 7%.

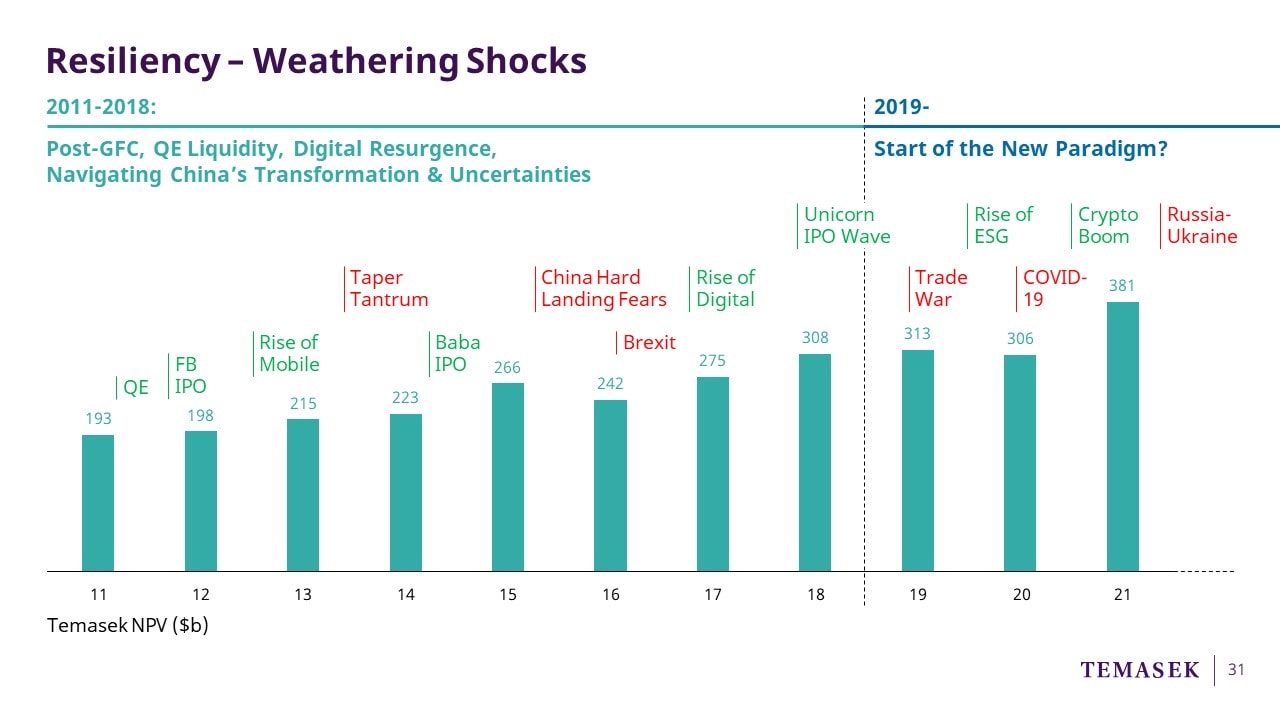

We achieved a more resilient portfolio that was able to not just take advantage of the opportunities,

but, more importantly, to better weather shocks.

This was evident by the fact that the portfolio declined by just 2.3%, when COVID-19 hit us in early 2020.

Alongside what we were doing on the investment side,

we were also building and growing new capabilities as a firm.

We created new platforms, which deepened our asset management capabilities, such as Pavilion Capital, Azalea, Clifford Capital, Heliconia and Innoven Capital.

We also set up the Enterprise Development Group,

which catalysed our early stage investing,

and was the forerunner of what we call today, our Development Engine.

Finally, we also deepened our bench strength,

including at the senior management team.

In fact, of our current Global Executive Council,

the senior leadership responsible for delivering on our T2030 strategy,

more than half had joined the firm in that decade.

Others were promoted through the ranks,

speaking to the leadership succession that we had undertaken as part of T2020.

In 2019, Temasek developed its T2030 Strategy.

Our 10-year roadmap for the decade ahead to follow on from our T2020 Strategy.

It guides our strategic planning, our allocation of capital,

capability building and institutional initiatives.

We were, and had been for some years, already in a Complex world – what we call, a VUCA world.

We recognised that the strategy had to encompass agility and adaptability.

More importantly, we had to be able to anticipate trends and visualise,

not just the road ahead, but the road around the corner.

That requires us to move beyond strategic planning to scenario planning.

And so, we started with our six top-of-mind Issues,

which Chin Yee presented earlier today.

There were two big differences from where we started in 2019,

to where we are today.

First, back then in 2019, we were anticipating a decade continuing with low inflation and low interest rates.

Second, little did we know that barely 8 months later,

we would find ourselves in a chaotic world as a result of the COVID-19 pandemic.

Low inflation has morphed into persistent inflation;

low interest rates became higher interest rates for longer;

and lower returns is now lower real returns.

We had to grapple with COVID,

and still grapple with a COVID cum post-COVID world,

which has seen increasing nationalism and protectionism with its consequences on globalisation.

In addition to sustainability and climate change,

the issue of energy security has now become ever more pressing.

You can’t look at energy transition without consideration of energy security.

And to add to Industry 4.0, we now have to deal with the impact of Generative AI, both in terms of opportunities and challenges.

We have not, in almost 40 years, seen such a confluence of different factors

that would affect any global financial investor.

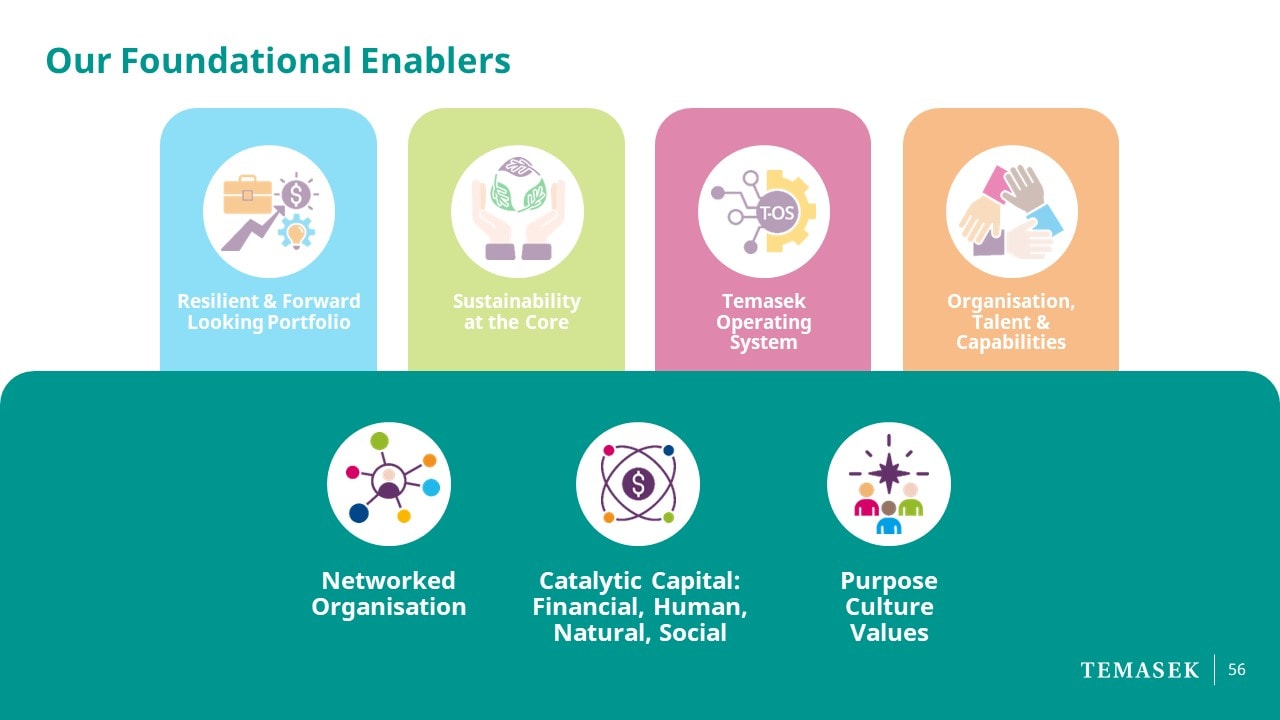

These are the four pillars of our T2030 Portfolio, and the three foundational enablers.

The four pillars are to build a resilient and forward looking portfolio,

with sustainability at the core of everything we do.

Building new capabilities and catalysing solutions under a Temasek Operating System, and focusing, yet again, on Organisation, Talent, and Capabilities.

To achieve, this we need our three foundational enablers.

One is our Networked Organisation.

The second is that we believe that our Capital must be catalytic in terms of Financial, Human, Natural, and Social elements.

You may notice that two of our pillars, the Resilient Portfolio and Organisational Development, mirror pillars in T2020, while Sustainability has been elevated to a pillar.

Hence, the evolutionary aspect of T2030.

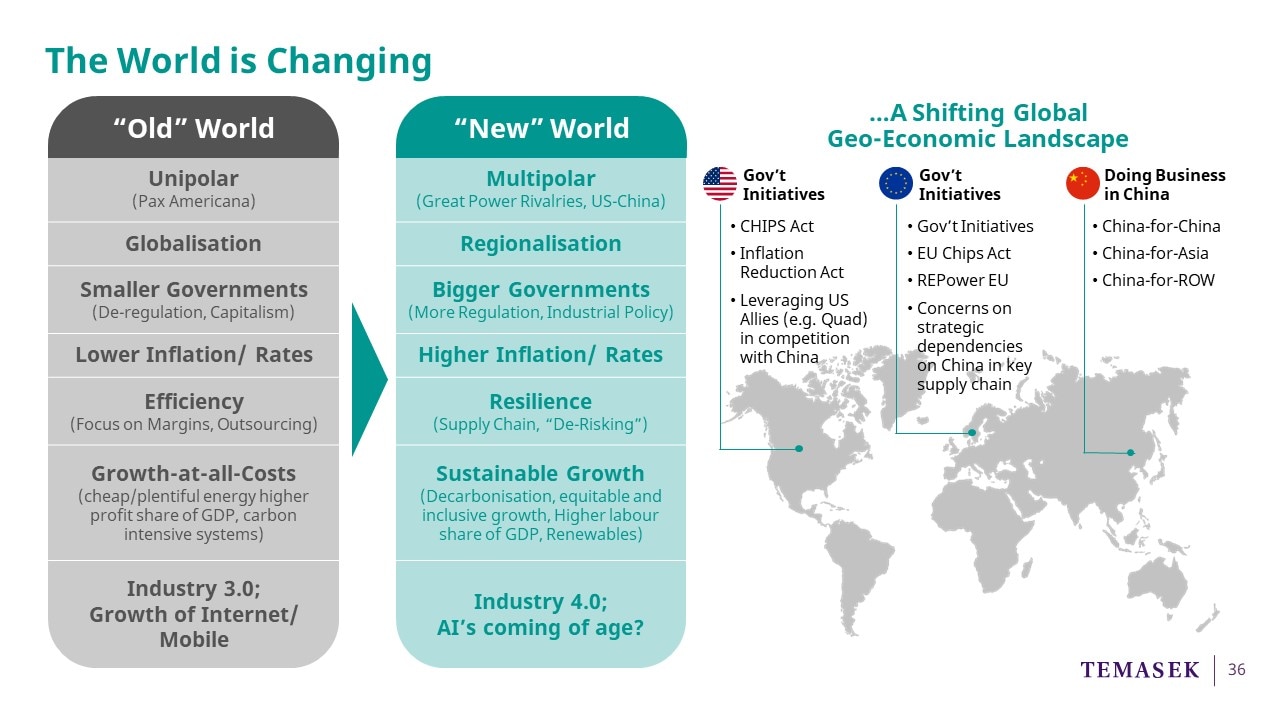

The world is changing.

The Old World, if I can call it that, was one where globalisation was celebrated, and one where there was significant global growth that lifted many emerging economies.

China became the main manufacturing hub of the world (creating the second largest economy in the world),

and consequently became the largest trading partner of many countries,

in place of the US and others.

It reduced the unit cost of production, with disinflationary aspects.

Today, Security and Resilience takes precedence over globalisation.

De-risking, decoupling and fragmentation are now the watchwords.

It may well become a more expensive world in the years ahead in this decade.

Going on to our four pillars.

The first is to build a resilient and forward looking portfolio.

Our focus for portfolio construction for this decade is to build a portfolio,

which can withstand exogenous shocks and perform through market cycles,

both up and down.

And in doing so, we want to continue our focus on growth opportunities,

for both our existing portfolio companies and the new investments we will make.

All for the purpose of generating sustainable returns over the long term.

For that, we have to do three things:

First, maintain a very Strong Balance Sheet.

Second, Protect the Core of the Portfolio

by supporting the strategies of the portfolio companies,

and being an enabler for their success.

And third, Position the Portfolio for Growth.

To deliver sustainable portfolio value over the long term,

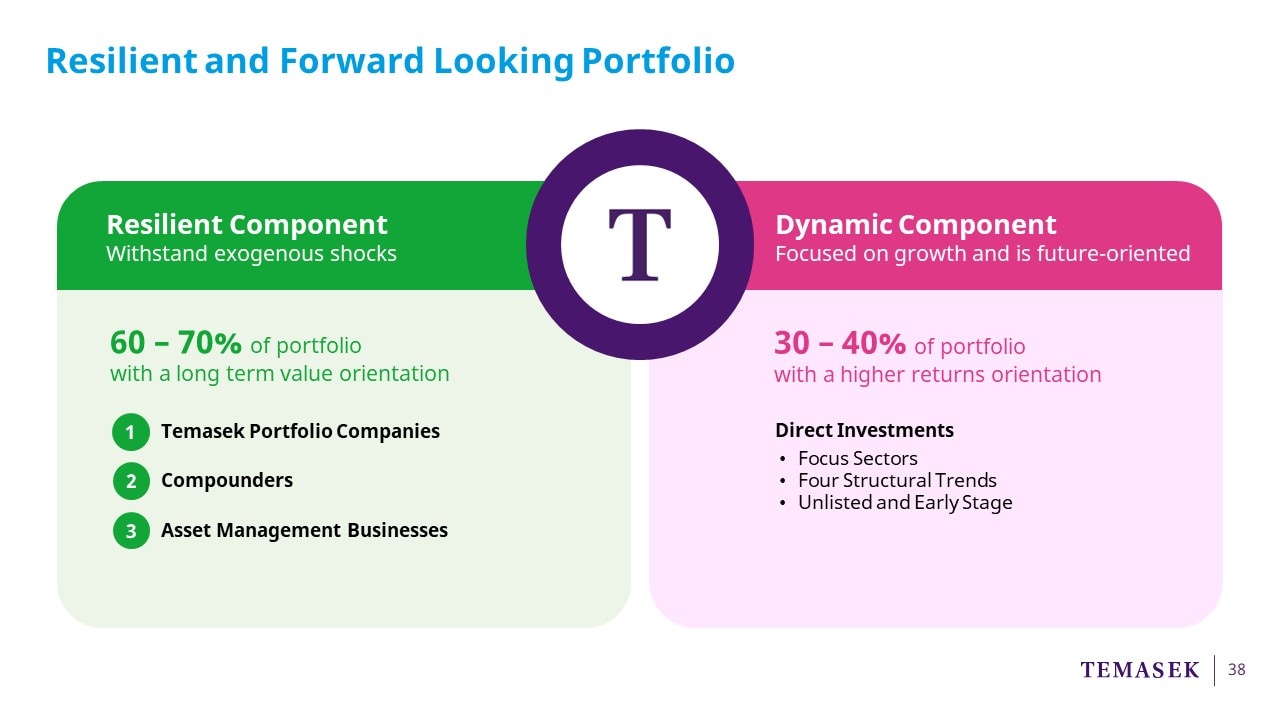

our portfolio has to encompass 2 components:

First, a resilient component which should be about 60-70% of portfolio value, comprising long term investments with stable and sustainable returns,

generating liquidity from dividends and distributions.

Second, a forward looking component that is more dynamic,

potentially shorter duration with capital continually recycled for reinvestment in higher growth opportunities for higher returns.

In generating sustainable returns over the long term, the shorter term results are also important,

as returns generated in the short term allow for recycling of capital,

contributing towards building and enhancing the goal of long term returns for our portfolio.

And some of these investments under the dynamic component may well emerge as compounders over the long term, and be part of the resilient component.

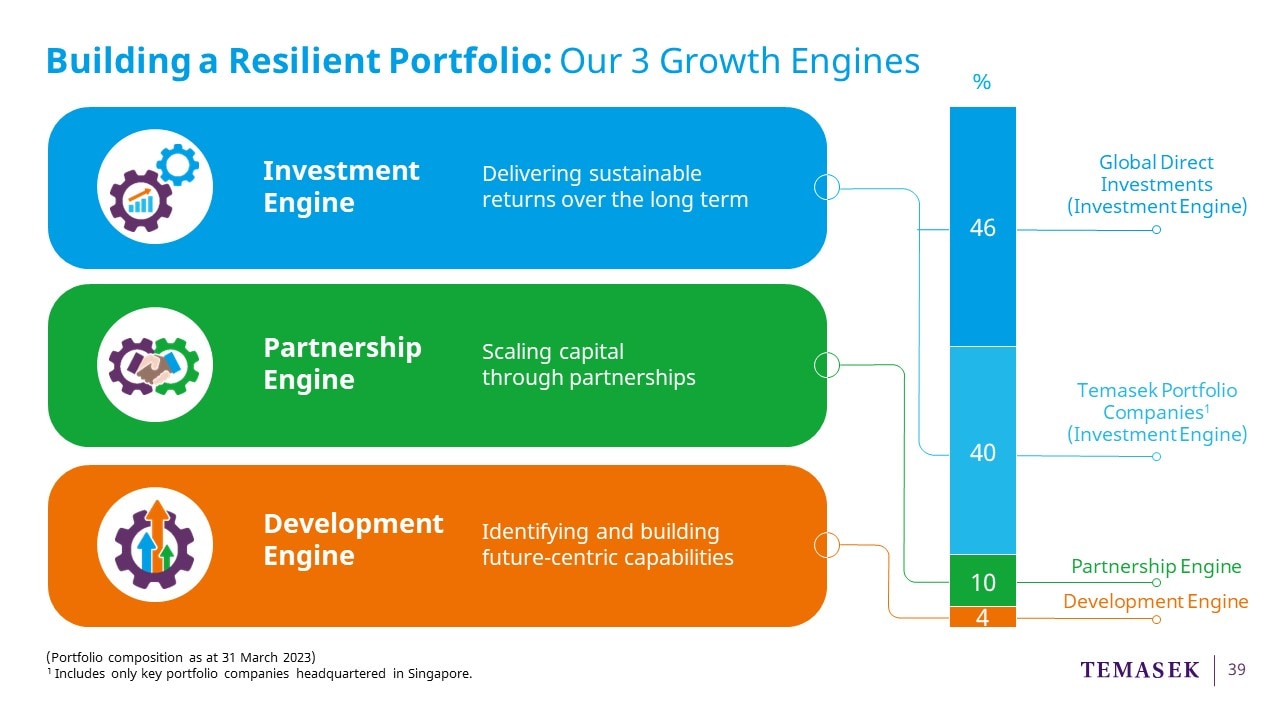

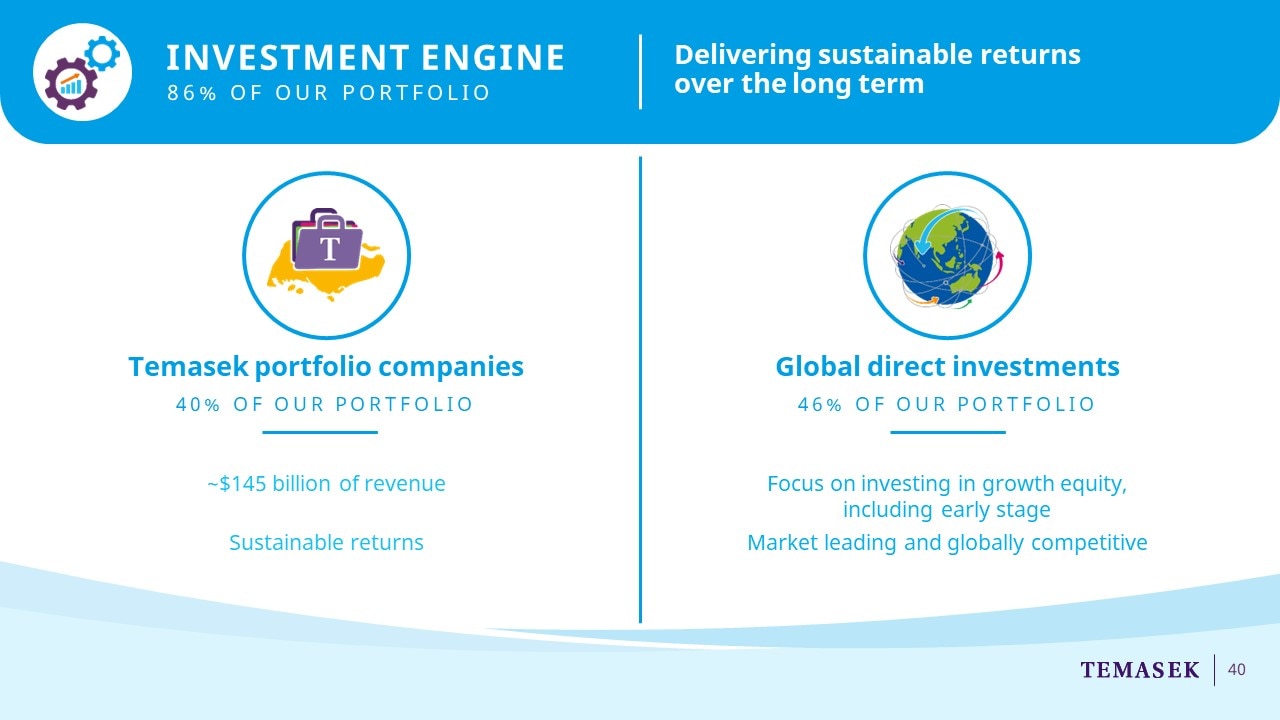

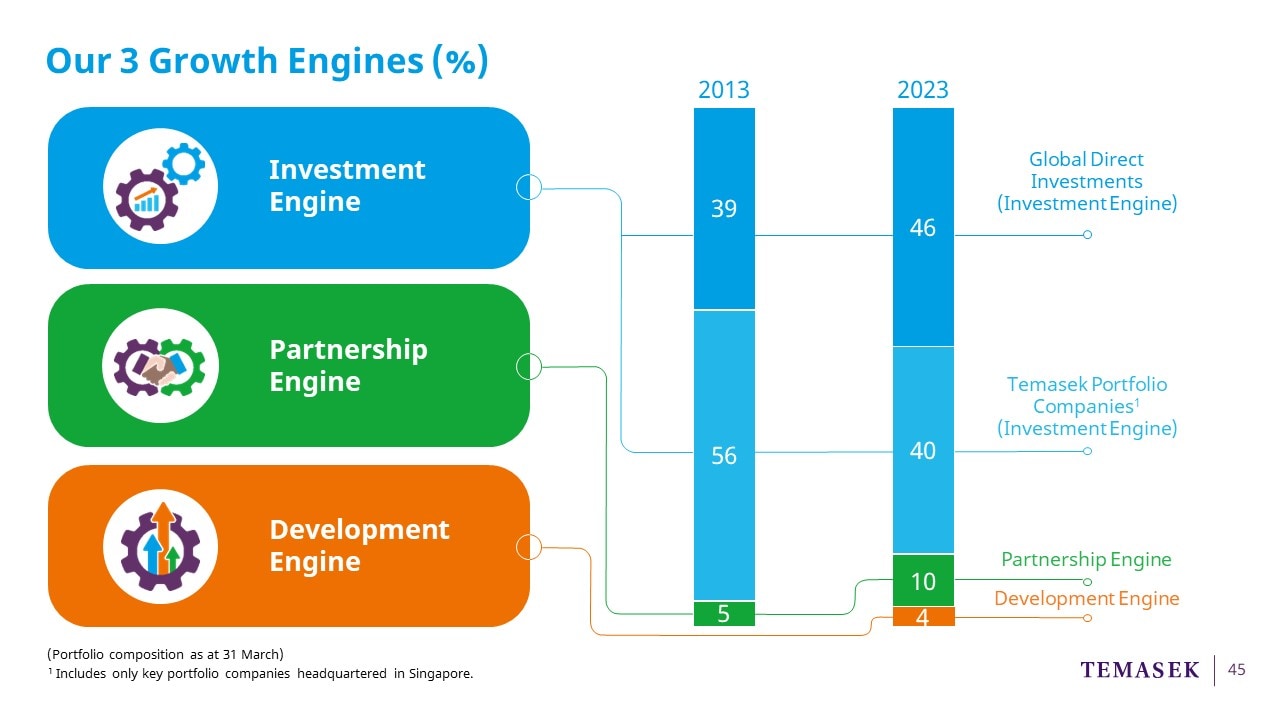

Our portfolio comprises three engines:

The first is the Investment Engine, which includes our:

Longer term Temasek Portfolio Companies, which I will call them TPCs in this presentation, in which we hold a minimum shareholding interest of 20%.

For the time being, they are all Singapore-based,

but we expect this group to be expanded to include non-Singapore-based companies in the years ahead.

Our Global Direct Investments, what we call Global DIs.

Together, they account for 86% of portfolio value,

with the TPCs being 40% and the Global DI now being 46%.

The Partnership Engine, which comprises our platforms where we partner with third parties to scale capital in areas where we believe we can generate stable and sustainable returns over the long term.

Currently, this comprises 10% of our portfolio value.

Finally, the Development Engine is where we identify and build future-centric capabilities to fill gaps in our long term portfolio.

Our TPCs, which comprise 40% of portfolio value generate S$145 billion dollars of consolidated revenue.

The Global DI has been the recipient of most of our capital in the last decade,

and is mainly in growth equity with a small component in early stage investments.

We invest in innovation and growth, and some of these investments have already emerged as long term compounders.

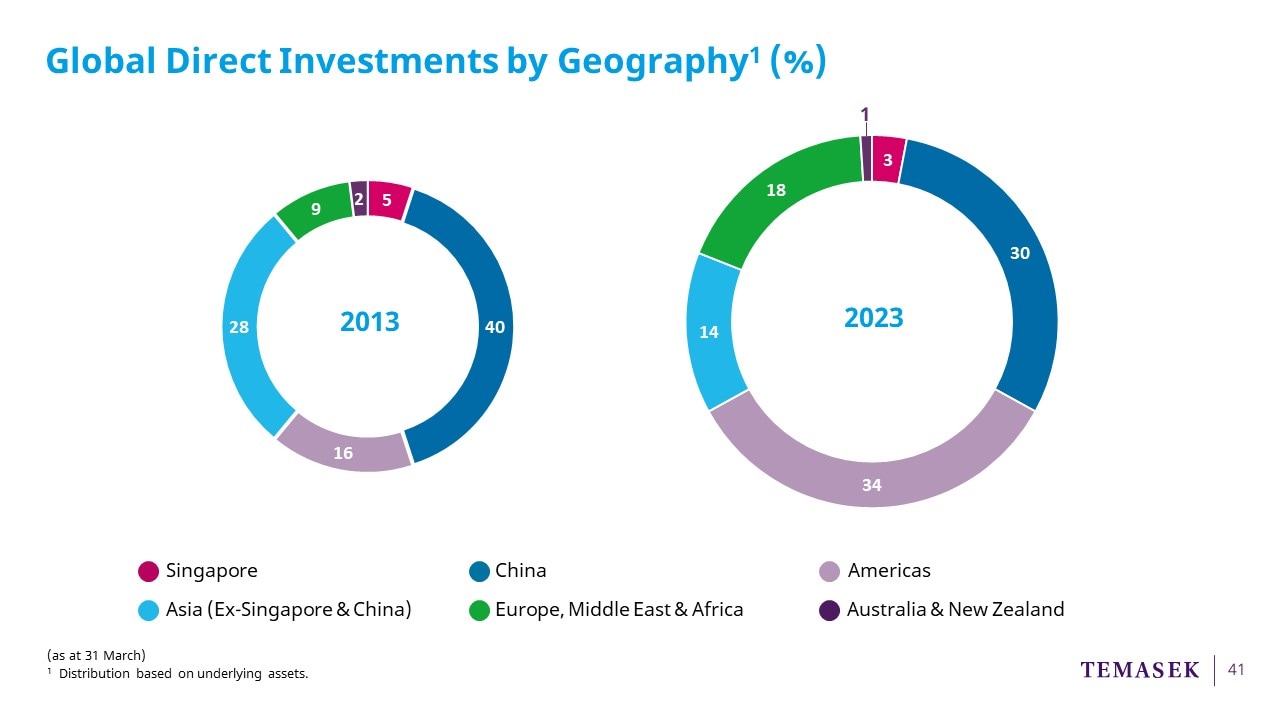

The four largest recipients of our capital over the last decade have been

the US, China, Europe and India.

You will note that back in 2013, if you see from the pie chart on the left,

China was the largest for Global DI,

and together with the rest of Asia, was 73% of Global DI.

The US and EMEA comprised just 25% of Global DI back in 2013.

Today, the US is the largest for Global DI, and together with EMEA, constitutes 52% of Global DI, a doubling of our exposure there.

The majority of our capital each year gets allocated to the US and EMEA.

In the past 10 years, we have invested $224 billion and divested $185 billion in Global DI,

and hence the dynamic component for the recycling of capital for higher returns over time.

It has generated a return higher than that of our 10-year total portfolio return.

Our capital allocation for the foreseeable future will continue to focus on these four regions identified.

But we are now looking to deploy more capital into SEA than we have in the past given the potential of the internet economy in the region, China + 1 and favourable demographics.

One reason is the emergence of the Southeast Asia digital economy.

Based on last year’s Google-Temasek-Bain report, Southeast Asia’s digital economy achieved revenues of almost US$200 billion,

which is expected to hit US$330 billion by 2025, up from US$200 million,

which was projected in the first report back in 2016, and grow to US$1 trillion potentially by 2030.

That’s twice as fast as the GDP in these countries in the region.

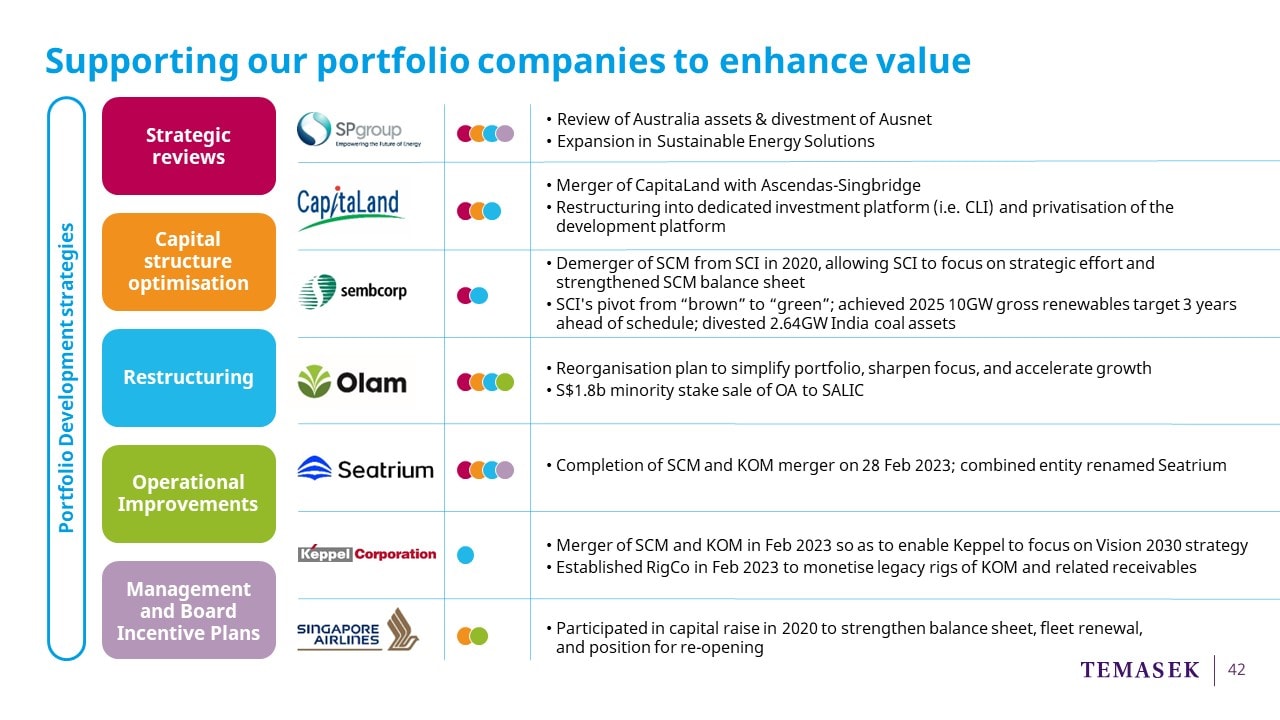

Our TPCs have historically been a mainstay for the stability of our portfolio.

But, with increasing uncertainties and complexity in the external environment, there is a greater need for us to engage more deeply with them on global trends, their strategies, and financial performance,

especially if we are to achieve our targeted return of exceeding our risk adjusted cost of capital for this decade.

We do not, and will not, involve ourselves in the day to day running of these companies.

Instead, we hold the Boards and management teams accountable for the running of the companies and the resultant performance.

As a snapshot, since we got more engaged with them since 2020, we have observed a value uplift north of S$10 billion.

By the way, these are just some of the key companies in the TPC portfolio, so there is much potential in this portfolio for sustainable value creation.

The Partnership Engine is 10% of portfolio value and has AUM of about $80 billion dollars.

Its purpose is to scale capital through partnerships.

Some of the platforms you see here are wholly-owned,

but in the last few years we have gone into partnerships with others.

For example, Decarbonization Partners is our joint venture with BlackRock. Leapfrog is an investment that we have made to support the efforts of a very pioneering person in Impact Investment, Andy Cooper and his co-founders.

ABC Impact, our own Impact Investment fund that we have sponsored with Temasek Trust.

Azalea issues bonds to retail and institutional investors secured by our LP interests in PE funds.

It also allows us to achieve an uplift in returns from these funds. It currently has AUM of $9 billion dollars.

It has also started vehicles for direct investments in PE funds.

It is part of the Seviora Group, which is the umbrella company for holding some of our asset management platforms.

The most recent is 65 Equity Partners. It provides capital solutions to businesses in the US, Europe and Singapore with an AUM of $4.5 billion dollars.

It also oversees the Anchor Fund that invests in companies seeking a primary or secondary listing on the Singapore Exchange.

Finally, Heliconia was established in 2012. Heliconia has AUM of $1.8 billion dollars, and is a provider of capital to Singapore-based SMEs with a mandate to be an enabler for them to regionalise.

The Development Engine is 4% of our portfolio.

Its aim is to invest in or build future-centric capabilities and business models.

It comprises, identifying cutting-edge innovation and investing in these business models early in their cycle such as the 4 on the left.

You have just seen a video of Electra, which uses an electrochemical process to reduce carbon emissions in the steel making process.

These companies are in decarbonisation solutions, quantum computing and nuclear fusion.

The second objective is to build new businesses for Temasek’s longer term portfolio, such as the four companies on the right.

ClavystBio accelerates the commercialisation of life sciences research and innovation in Singapore.

Ensign, our Singapore-based cyber group. It has close to 500 cyber professionals

who serve Singapore and the regional markets, and not just our portfolio companies.

Its revenue in 2022 was S$250 million, and continues to exhibit favourable growth prospects.

This is the composition of our growth engines, with a comparison between 2013 and 2023.

You will notice that for the Investment Engine, the TPCs were 56% in 2013 and 40% today.

The global direct investments were 39% in 2013 and 46% today.

The Partnership Engine has doubled from 5% to 10% today.

Our Development Engine has gone from a negligible amount to 4% of our portfolio value today.

So you can see that we have been diversifying our portfolio beyond our Temasek Portfolio Companies which are Singapore based, into global direct investments, the Partnership Engine, and the Development Engine, in the past 10 years, in line with our aim of being a global investment house.

And this has been positive for our longer term returns.

Having said that, the absolute value of our Temasek Portfolio Companies has increased substantially in value over the past 10 years.

The second pillar is Sustainability at the Core of everything we do.

We embed sustainability in all that we do.

We aim to deliver sustainable value over the long term for all our stakeholders.

To build a sustainable portfolio and institution through our strategy,

we do so by how we operate as an institution,

how we shape our portfolio,

and how we engage our portfolio companies on their sustainability journeys.

For example, we inaugurated the TPC Sustainability Council in 2021

to encourage discourse and collaboration across our portfolio companies around climate and ESG,

so that we can learn from each other and attain best in class standards.

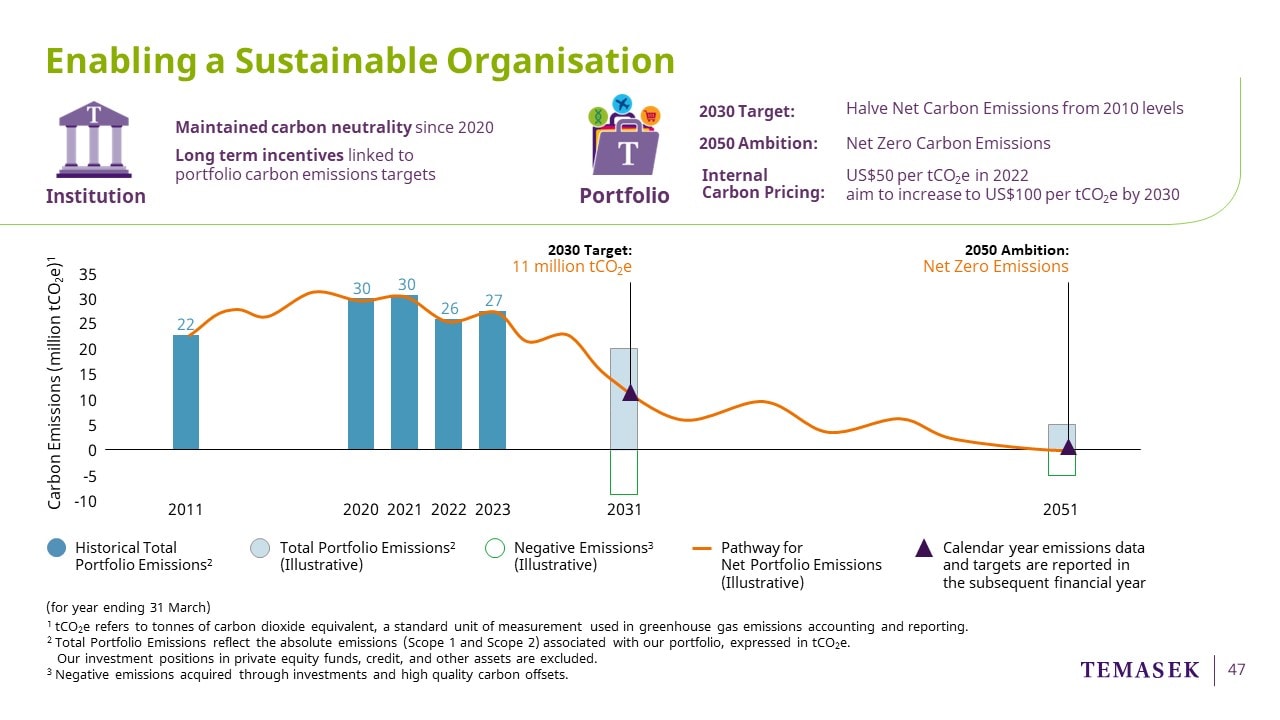

What are our carbon goals?

We have committed to be carbon neutral as a company, and we have been so for every year since 2020.

We have set a target to halve our net carbon emissions across our entire portfolio by 2030, as compared to the number in 2010.

So, we have to go from 27 million tCO2e today to 11 million tCO2e by 2030.

It is not easy when we have long term interests in power and utilities, the built environment and the aviation and maritime sectors.

But, we are committed to achieving net zero in 2050.

We have instituted an internal carbon price in 2021 of US$42 per tCO2e.

We increased it last year to US$50 and we will progressively increase it to US$100 by 2030.

We have also aligned our long term incentives as Temasek employees to our portfolio carbon emission targets.

Why have we done this?

So that we take the issue of carbon emissions seriously and that means cutting down both absolute emissions and carbon intensity.

Anyone who has a long term interest in assets and businesses bears the tail risks of businesses that fail to mitigate, adapt and transition.

Companies that fail to act face higher spreads on financial instruments, may bear increased premia for insurance, or may well have uninsurable stranded assets, resulting in potentially lower valuations reflecting a higher cost of capital in the asset pricing model. It will also guide us on where we should invest.

This does not mean that we will not invest in carbon emitting businesses. We already have investments in carbon emitting businesses. We have 55% in Singapore airlines, for example.

But, we will invest in them for as long as there is a clear transition plan for reduction of absolute carbon emissions and carbon intensity.

This is the reason why we are investing with Brookfield Global Transition Fund in Origin Energy’s Energy Markets business in Australia, with the intention of transitioning coal fired power generation to renewable energy sources.

We also focus on ESG.

And for us and our portfolio companies, this is a journey.

We do not condone greenwashing.

And so we pay attention to not just financial and operational goals and objectives but ESG goals and objectives too.

We have an ESG framework that is applied to all our current investments and the potential investments at the evaluation stage.

If we identify key ESG risks and there is no pathway to resolving them, we will not invest.

We also engage our portfolio companies on their ESG journey and seek to assist them where we can.

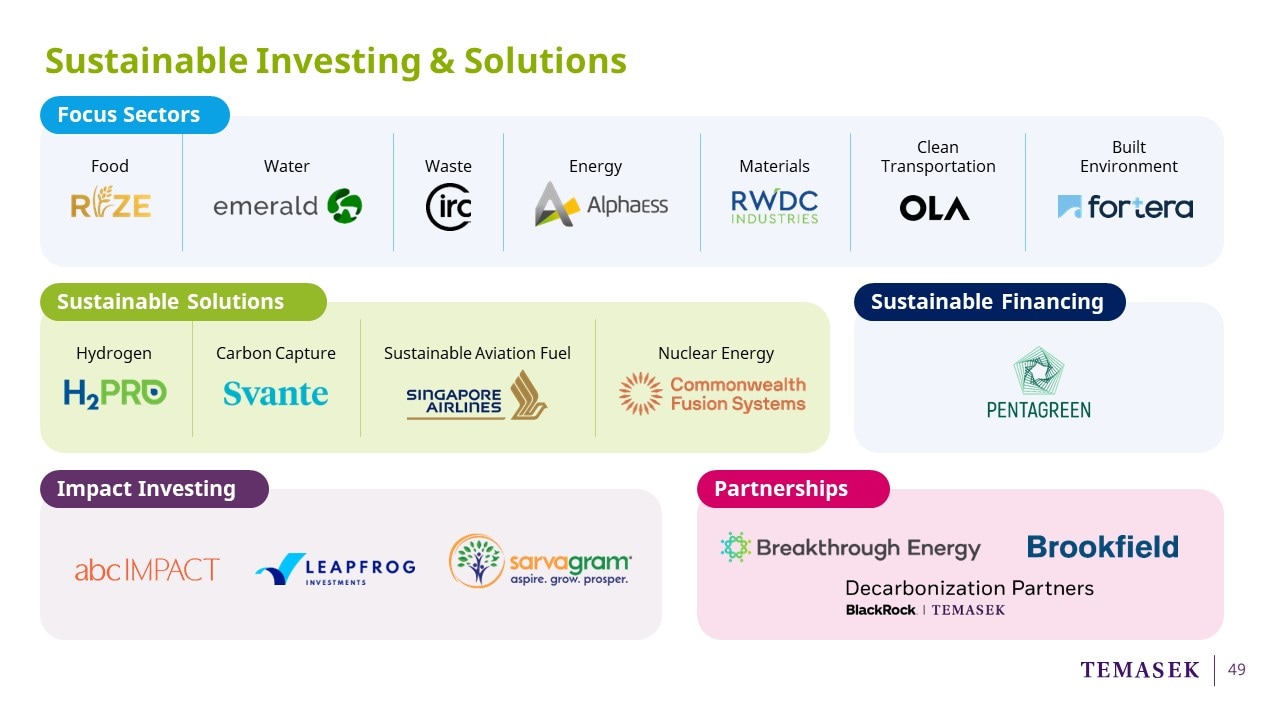

So, what are we doing as an investor in the context of sustainability at the core?

We have many initiatives alongside our ambition.

We invest in climate-aligned opportunities in the focus areas of food, water, waste, energy, materials, clean transportation, and the built environment.

We have a focus on Sustainable Solutions. In particular, Green Hydrogen, Carbon Capture, Sustainable Aviation Fuel, and Nuclear Energy.

We also believe there is a need to get involved in Sustainable Financing. We believe in catalysing financing to accelerate the adoption of green energy and decarbonisation solutions, especially for developing countries.

One of the biggest issues is addressing the gap in sustainable infrastructure financing, especially in emerging markets, is the access to green solutions and affordability. Together with HSBC, we formed a partnership called Pentagreen - the focus of which is on marginally bankable projects in Southeast Asia in the areas of renewable energy, water, waste-to-energy and clean transportation.

Impact Investing. While there is much focus on impact for climate, we must not forget impact for communities. It is a role all of us can play in the uplifting of communities, especially in emerging markets. We invested in ABC Impact, Leapfrog and other funds, and made our first direct investment in this space, SarvaGram, which we have previewed in the video you saw before Chin Yee’s presentation.

But to do all this, we realised that we have to form partnerships as well, and focus on investing in tech-based decarbonisation solutions.

We have a close relationship with Breakthrough Energy Ventures and have become an anchor investor in BEV Select, which is investing in growth equity in decarbonisation solutions.

Together with BlackRock, we have formed Decarbonization Partners to invest in late venture and early growth opportunities in the tech-based decarbonisation space.

For energy transition, we partnered Brookfield in their global transition fund, and we were attracted by the way they were allocating their capital on the three investment themes of Business Transformation, Clean Energy, and Sustainable Solutions.

The third pillar, our Temasek Operating System.

Our Temasek Operating System guides us to build specialised, next-generation capabilities, which we believe will produce essential skill sets of the future.

These are horizontal capabilities that can be applied across sectors and geographies and across our portfolio.

It helps differentiate us as an investor and shareholder.

More so, it is an important initiative to bring on board a broader range of skill sets to help future-proof us and our ecosystem.

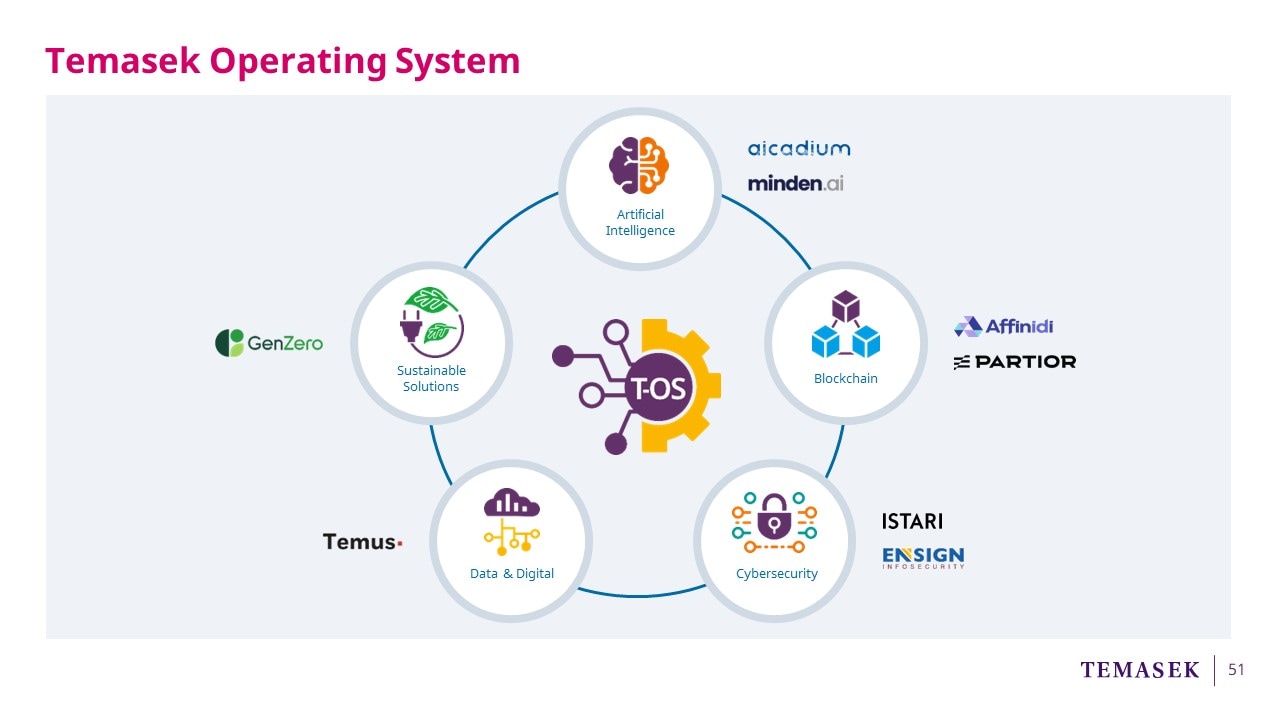

We have set up Centres of Excellence in AI, Blockchain, Cybersecurity, Data & Digital, and Sustainable Solutions, where we are building a suite of specialised, next-generation capabilities, which can differentiate us as a value adding investor and shareholder.

It is effected through venture building with the creation of use cases to attract talent in specialised verticals. It is about catalysing solutions for our portfolio as well as the marketplace.

It allows us to bring on board, grow and develop specialised talents using economies of scale, and offer them career pathways within our ecosystem.

We innovate new applications, business models and ventures, which is part of the entrepreneurial DNA of Temasek.

We focus on Value Creation and seek to Value Capture through the companies we establish as well as the companies that benefit from their solutions.

For example, Aicadium builds a team of AI talents, partnering our TPCs to co-innovate and scale AI products.

In blockchain, Partior is a distributed ledger technology provider enabling the next generation of cross-border payments and value exchange. It was founded in 2021 by J.P. Morgan, DBS and Temasek.

Istari is our global cyber platform based in London that acts as a trusted adviser to clients, deploying a portfolio of curated solutions. Its network has access to more than 3000 cyber professionals.

It has worked with Temasek’s cyber COE to protect Temasek and our ecosystem, and to make sure that we are cyber resilient. Our TPCs who use the services of Ensign and portfolio companies of Istari have improved the mean time to resolution of cyber incidents by 55%, which is close to the Cybersecurity and Infrastructure Security Agency’s benchmark, thereby enhancing the resiliency of our ecosystem.

Temus builds distinctive tech capabilities to accelerate the adoption of digitisation in our TPCs and others.

It has a headcount of 320 in total, including 230 digital talents since its founding two years ago. More importantly, it is contributing to workforce transformation through its "Step IT Up" programme, where it converts non-IT talent to digital talent in Singapore.

GenZero is our sustainable solutions platform focused on tech-based decarbonisation solutions, nature based solutions, as well as products and services. It has an initial capital commitment from us of $5 billion.

All these platforms have revenue and breakeven targets, and our intention is for them to have returns in excess of their risk-adjusted cost of capital.

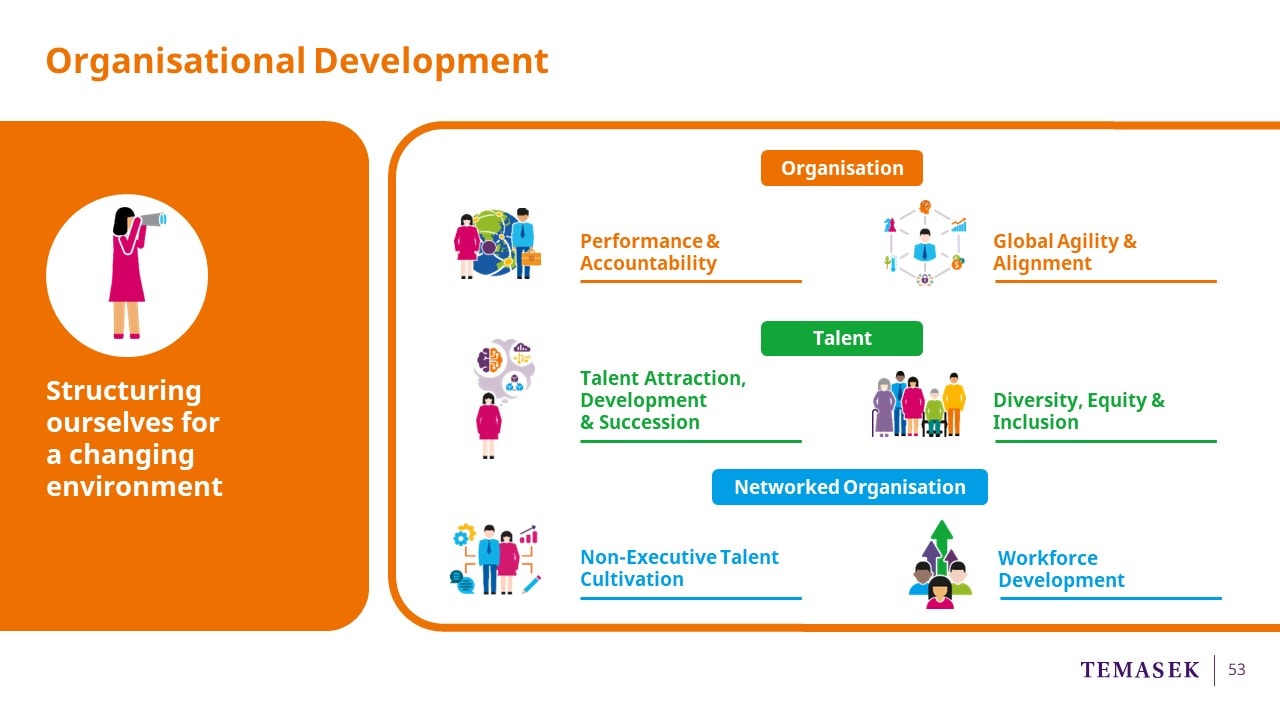

Finally, our fourth pillar, and our most important one.

Many may see Temasek as being in the investment business, but we see ourselves as being first and foremost, in the people business.

We need to be an organisation that people want to join so that we can attract the right people with the right capabilities to join and, more importantly, stay with us.

We have to develop our talent, so we can grow, individually, and collectively as a firm.

At the organisation level, we have to be agile, adaptable and hold ourselves accountable for our performance.

Our people are our most important resource.

Whatever your strategy, whatever the amount of capital you have to deploy, without good talent, you cannot get to where you want to go, or achieve what you want to achieve.

This is why we have a laser-like focus on developing our organisation and its human potential.

It was a central feature of T2020 and it remains a central feature of T2030.

So to achieve this, we need to make sure that we structure ourselves for a changing environment and focus on talent attraction, talent retention, talent development and talent management.

This focus is embedded across our organisation structure, our talent management initiatives, and how we engage and partner across our networked organisation.

Let me share some of our initiatives across three areas:

1) The first is Organisation:

We are focused on Performance & Accountability. The way we organise ourselves is to enable us to optimise team performance, capital and resource allocation, as well as to align with compensation.

We also want to achieve Global Agility & Alignment.

We support the mobility of our workforce globally to enable a one Temasek culture and to give individuals the opportunity to broaden their experience.

2) The second area is Talent:

We focus heavily on talent development to ensure our employees stay relevant and equip themselves with future-centric skillsets, to build a strong pipeline of global leaders for our succession planning purposes.

In Diversity, Equity, and Inclusivity, we want to seek a broader, and more inclusive meritocracy.

For example, we have Temasek Women’s Network, which was previewed in the video. Our focus is to address the aspirations of our female colleagues, now 46% of our workforce, to ensure that they have opportunities to progress in their careers with us while balancing other considerations.

We support programmes that are geared towards bringing career opportunities to neurodiverse talents. Through Ensign, our cybersecurity group, as well as a programme that we will preview later in a video called GATES, Growing Autistic Talent for Engineering Sector.

3) Third, being a Networked organisation:

We recognise that we need to bring in non-executive talent, advisers, who can help us and whom we can leverage on to partner and support us as we grow our portfolio globally.

We are also focused on Workforce 4.0 to support the transformation of our TPCs. Getting our TPCs to be future ready is key to the economy of Singapore, the success of our portfolio companies, and for our long term returns.

We strive to work with our companies, their unions and employees, to understand and anticipate shifts in the relevant sector, so that as our TPCs transform themselves and their business models.

We can also focus on org design and redesign, job design and redesign, skilling, reskilling and upskilling of the workforce to achieve higher productivity and better opportunities.

Our Temasek Tripartite Conversations bring together relevant government agencies, trade unions and companies, not just our TPCs for this purpose.

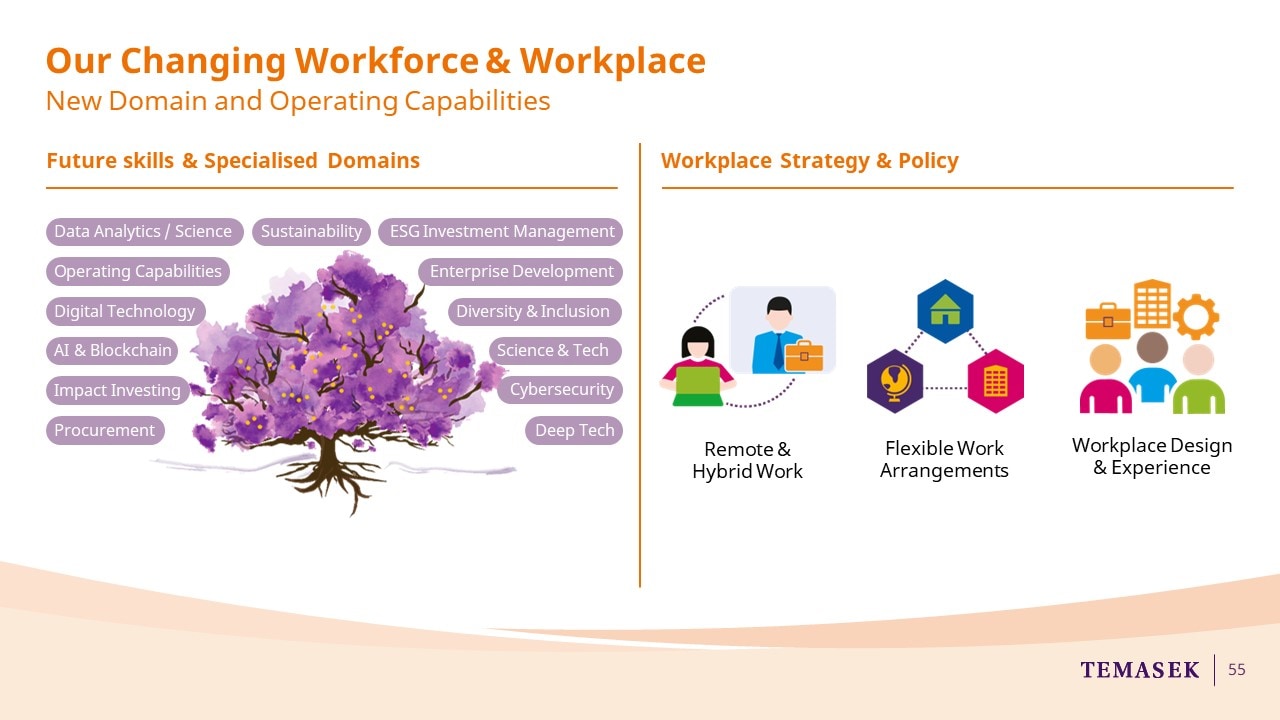

Over the last 10 years, we have grown our global workforce.

In line with our enlarged portfolio, increasing coverage and growing complexity of our operating environment, we have built our offices around the world. Now, we have 13 offices in different continents to which we operate.

We are a multinational and multicultural organisation, represented by a workforce of 34 nationalities, in 13 different offices as part of our OneTemasek team.

We have just added Paris to our network of International Offices.

As a global investment house, we have now evolved a multinational leadership that can be seen from the composition of our senior leadership team, as well as through the ranks.

We have doubled our investment professionals in the past decade.

But more importantly, we have invested in bringing on board specialised capabilities in new domains, some of which are highlighted on the left side of this slide.

We also track the broader trends to ensure that our workplace strategy,

design and policies can keep up with our next-generation workforce and colleagues.

Our four pillars are underpinned by our three foundational enablers.

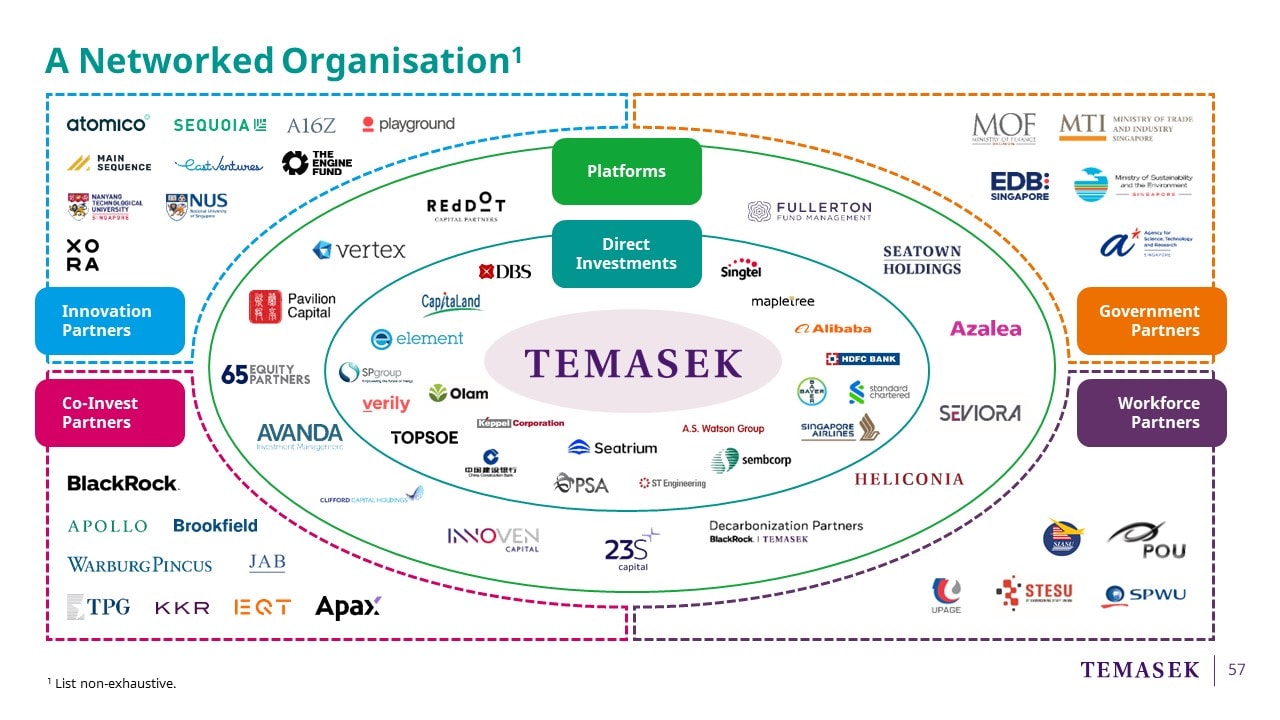

The first is that we have to operate as a networked organisation, internally and externally.

Within the firm, this means collaboration across teams and locations, harnessing diverse skill sets to achieve our institutional goals.

Beyond the firm, we augment our capabilities with those of external partners and collaborators, to collectively address issues and create solutions.

Second, our capital must catalyse solutions that generate value across the four dimensions of financial, human, natural, and social capital.

Third, we instil a sense of purpose, build a culture of teamwork, and cultivate a strong set of values to navigate the decade ahead.

It is difficult for us to do everything on our own.

We recognise we do not have all the skillsets necessary for our objectives.

Therefore, we need to be a globally networked organisation.

We augment our capabilities with the skillsets of our ecosystem partners,

who are knowledgeable experts, ahead of the game, and able to bring value-added perspective to what we do.

We partner with them on opportunities and solutions that addresses challenges in a complex global environment.

Someone told me once,

Knowledge is good,

Know-how is better,

Know-who is best.

We deploy catalytic capital to deliver sustainable value over the long term in these four dimensions:

Financial Capital, which we use to stimulate innovation and growth.

Natural Capital, to foster sustainable solutions for a more liveable world.

Human Capital, to uplift people’s capabilities by harnessing human potential and seeking to ensure that the future is human centered and human led;

And Social Capital, for social progress which enables resilience and inclusivity in societies.

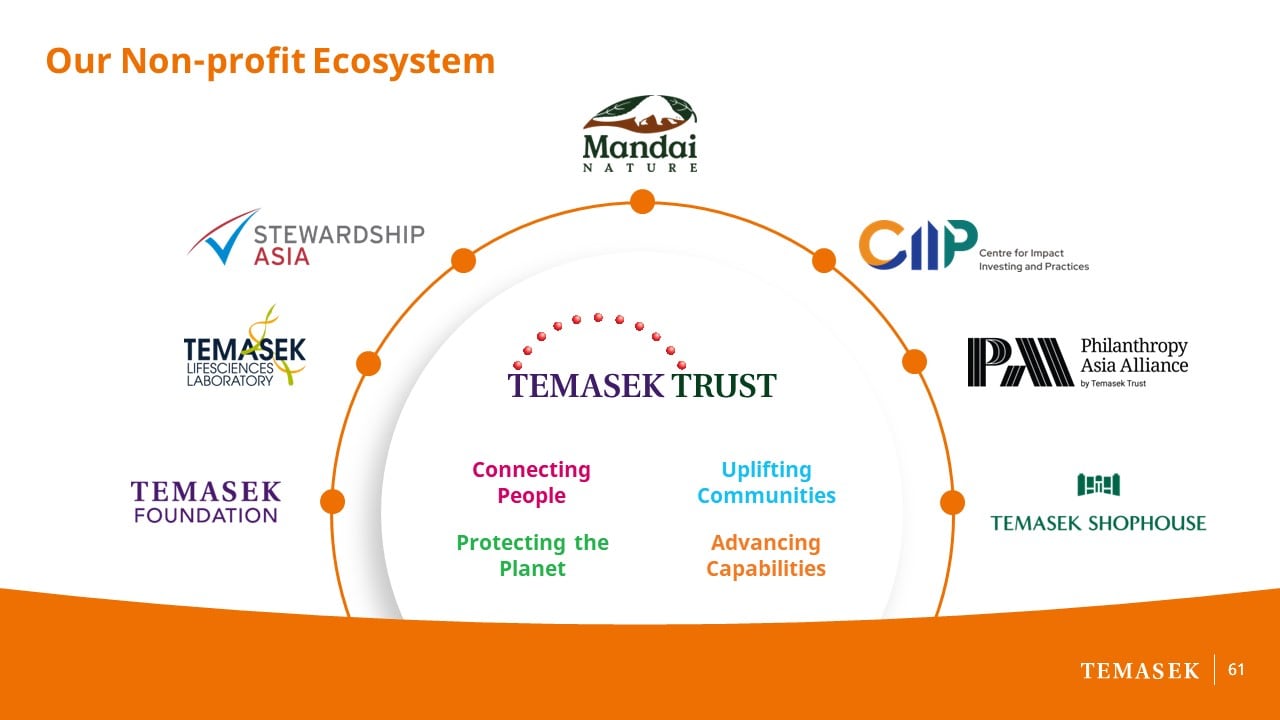

Seeding social capital.

Since 2003, we have been setting aside a portion of our net positive returns above our risk-adjusted cost of capital for community gifts.

Our not-for-profit gifts are approved by the Temasek Board

before being gifted to Temasek Trust,

to support community initiatives based on the principles of

sustainability and good governance.

Not-for-profit gifts to Temasek Trust enable non-profit entities to fulfill our four community objectives of:

Connecting people,

Uplifting communities,

Protecting our planet, and

Advancing capabilities,

in Singapore, Asia, and beyond.

Temasek Trust manages the funds and disburses the gifts via grants and endowments to the non-profit ecosystem in Singapore and beyond,

delivering on our community objectives.

To date, Temasek’s gifts to Temasek Trust have enabled programmes that have impacted about 2.5 million lives across Singapore and beyond.

Now we have a video on a programme that they have supported called Growing Autistic Talent for the Engineering Sector, or GATES.

It trains and places neurodiverse tertiary-level graduates in full-time jobs in the engineering sector.

We have to move beyond the legacy of autism

to the future of neurodiversity,

hence the GATES programmes and other things we are looking into.

Having a strong and clear purpose

enables companies to stay true to their course

amidst the challenges of this complex world.

In 2020, we embarked on a year-long organisation-wide exercise

to come up with our Purpose Statement.

It involved almost 600 of our global staff of 800 people,

and we came up with our Purpose Statement,

“So Every Generation Prospers”.

It is our North Star.

It helps to remind us of who we are, and why we do the things we do.

Who We Are – We have three roles in our Charter – that of an active Investor, a forward-looking Institution, and a trusted Steward.

And in all these three roles,

we seek to

Do Well,

Do Right,

and Do Good.

Our MERITT values – Meritocracy, Excellence, Respect, Integrity, Teamwork, and Trust underpin all that we do.

Why We Do The Things We Do – In our 3 roles, we aim to

Invest in Human Potential,

Build with Courage,

Catalyse Solutions,

And Grow for Generations.

We do so with the courage of our convictions,

With tenacity of purpose,

With a knowledge that change is a constant,

And because of that we must be comfortable with ambiguity.

To do things today with tomorrow clearly on our minds,

So Every Generation Prospers

Thank you.