Temasek’s portfolio contains listed and unlisted assets that span the entire business life cycle, from start-ups to mature businesses.

There are five main sectors. By size, the largest is transportation and industrials (for example, Singapore Airlines and Sembcorp Industries), followed by financial services (for example, DBS Bank and Adyen); telecommunications, media and technology (for example, Internet brands and shopping platform Meituan); consumer and real estate (for example, luxury fashion brand Moncler and AS Watson); and life sciences and agri-food (for example, Covid-19 vaccine-maker BioNTech and Mastronardi Produce).

Temasek’s aim is to build a resilient portfolio that can weather shocks and deliver sustainable long-term returns.

We put five questions to Temasek deputy chief executive Chia Song Hwee that focus on the company’s investing strategy and performance.

How does Temasek measure its performance?

Overall, an important indicator of our long-term performance is the 20-year total shareholder return. It is calculated over a rolling 20-year period. For the 20 years ending in 2023, this was 9 per cent. (It’s been as high as 16 per cent in 2010 and 6 per cent in 2020, for example).

We evaluate our performance based on the absolute return against our risk-adjusted cost of capital. This is a more conservative approach. Other investors may measure their performance relative to relevant benchmarks such as market indices. In such cases, their investment may be making losses, but less than their benchmarks, and these investors will still be seen as doing well.

For each investment, we also attribute a different cost of capital, depending on the market, sector and the investment itself. The cost of capital will be higher for a private investment to reflect the illiquidity risk versus that of a public company, other things being equal.

About half – 47 per cent – of our portfolio is in liquid and listed investments. Some years ago, we increased our exposure in private markets, privately held companies and private credit, and they have delivered returns above the cost of capital and higher than the liquid and listed portfolio.

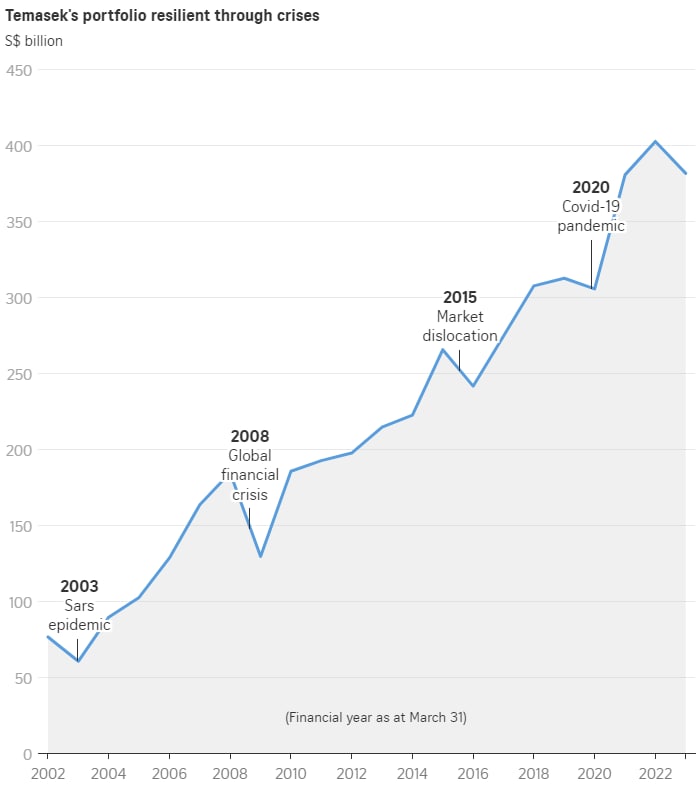

Another indicator is how our portfolio has recovered after each crisis. As you can see, our portfolio has bounced back after each crisis and most recently, from the Covid-19 pandemic (see chart below).

Talk us through Temasek’s investment approach

We are fortunate in that we are not constrained by having to buy or sell within a fixed time duration. This means that if a private equity does well, we can continue to hold it for compounding effect or monetise through listing or trade sale at an opportune time.

We are not a buyout outfit. We seldom do control deals. When we do, we will co-invest with other partners like KKR or Thoma Bravo.

Temasek has 13 offices around the world which allow us to develop relationships with businesses over the long term. It’s important to have people on the ground who understand the local environment.

We have multiple channels, including general partners of funds and bankers, sharing opportunities with us, but we also originate our own investing opportunities.

Our teams perform due diligence for all investment proposals before presenting them to our investment committee. The value of having a committee is that we debate and question the merit of the investment or divestment. This way, we harness the different perspectives and views of individuals as well as their experience, exposure and networks.

We won’t have consensus all the time. But having minds applied on issues allows us to get clarity on the decision that will likely give us the right outcome. Without sufficiently diverse views, you may not get the optimal considered decision.

(Temasek gathers the views of business leaders with deep experience, insights and perspectives on significant industry, economic, social and political trends. In August 2023, it launched the South-east Asia Advisory Panel, adding to the existing ones for Europe and the Americas.)

In investing, there is a simple saying, which is to buy low and sell high, but it is much more complex. What is considered high or low? Today’s high may not be the highest, and today’s low may not be the lowest. To add another layer of complexity, we are making multiple investments. As a long-term investor, we focus on fundamentals and look beyond the immediate horizon.

Every single investment is a learning opportunity. Learning from one sector in one market can be very useful when investing in another market. We hold people accountable when things don’t go well. But the more important thing is how to prevent a recurrence. When we do things well, we try to institutionalise as much of the learning as we can so that we have a higher probability of achieving good outcomes.

Our portfolio comprises two categories of investments. A resilient component that is held for the long term and can provide stable and sustainable returns, and a dynamic component that has higher growth opportunities.

Our early-stage investments fall under the dynamic component. They help sharpen our understanding of future trends, the impact to our existing portfolio, and allow us to gain insights on constructing our future portfolio. But we define the risk parameters and cap our overall portfolio exposure for early-stage investments to 6 per cent.

What have been some of the successful investments?

From our experience, we get the best returns when we invest early, at more favourable valuations. We increase our investment as the company grows, from start-up, to pre-IPO (initial public offering), to IPO and beyond.

Global integrated payments platform Adyen is an example. When we invested, it was a small company based in Amsterdam. Now it is an almost €40 billion (S$58 billion) market cap company. When we invest early, we build relationships and conviction, and invest more and more as we go along.