Temasek Review Media Conference 2022: FAQs

Selected Questions & Answers from the Temasek Review Media Conference 2022

12 July 2022, Singapore

The following is an edited transcript of questions and answers at the Temasek Review 2022 Media Conference.

Grammatical edits have been made to aid readability. For the same reason, questions are not necessarily listed in the order in which they were asked, but grouped thematically.

Slides and charts have been added from the Temasek Review 2022 where they were included in the presentation, or where they contain material helpful to the reader in providing detail to supplement the answer.

Click here to read the transcript of the preceding presentation and accompanying slides, and here to view all of the key financial metrics and diagrams in Temasek Review 2022.

Question on Net Portfolio Value

QUESTION: You doubled the net portfolio value in the last 10 years. So, is that one of the figures you run the company with or is it just net profit? In other words, could we expect that one of your targets would be to, again, double it over the next 10 years?

LIM MING PEY: I think many of you here will be familiar – the primary measure which we measure our portfolio against is our Total Shareholder Return, and our aim is always to achieve long term sustainable returns above our risk-adjusted cost of capital. I think you've heard from our 2030 strategy there are many things we're working towards in the decade ahead. So no, we would not be looking at portfolio size as just one target but rather it's really about working towards our structural trends, looking at the different opportunities from a bottom-up perspective and finding the best opportunities that can give us that resilient and forward looking portfolio that we want to construct.

ROHIT SIPAHIMALANI: Just to clarify your point, on this metric of risk-adjusted cost of capital, currently it's 7% for us. Over the last decade, as you pointed out, our returns have been just about 7%. So, we have met our risk-adjusted cost of capital. Going forward, while we don't have specific targets for portfolio value, the goal is to exceed our risk-adjusted cost of capital.

Question on Investments and Divestments

QUESTION: You mentioned that you will slow down your investment pace this financial year. How about divestments? I noticed that for the past two years your divestments have picked up. So what's your quick criteria when you come to the decision for divestment?

ROHIT SIPAHIMALANI: We will look at valuations and the intrinsic value of the companies that we hold. If we think if they're undervalued, clearly we will not look to divest them and we then have no compulsion to divest them. We also have a strong balance sheet and strong liquidity so there's no compulsion to divest at points where it doesn't make sense.

Having said that, if in the changing environment we think there are certain companies that have played out the investment thesis and are close to the intrinsic value, we will go ahead and divest. So, my sense is that as you look at this year you will probably see a decline in both investments and divestments for that reason. But we will continue to divest where we think an investment thesis has played out.

Question on Investments and Divestments (2)

QUESTION: You touched upon divestments, and it was a characteristically active year for you with S$37 billion of divestments. But when you sell, what latitude do you have to remain in cash when you can see bad news coming from the stock markets ahead as has been the case throughout this year? To what extents are you expected to redeploy pretty quickly?

ROHIT SIPAHIMALANI: We don't really have any compelling need to invest if we don't see the right opportunities at the right value. Similarly, we've seen in the last two decades – you’ve had SARS, the GFC, the European debt crisis, China in 2016, COVID, and there have been many periods where we felt that the risk reward was not as compelling to be investing. We've been happy to sit on higher amounts of cash during those periods. But when we do see the right opportunities aligned with the long term trends, we will deploy.

LIM MING PEY: Again, that speaks to the value of our long term orientation as an investor looking for long term sustainable returns. We are not under any pressure to buy or sell in a particular year. It's back to the fundamental view of the intrinsic value and the trends of what we're looking at.

Question on Investment – Unlisted Assets

QUESTION: We noted that unlisted assets now make up slightly more than half of Temasek's portfolio and this is partly due to the good returns despite the tough times. So, we are wondering whether this will be Temasek's strategy going forward and what is your outlook on this portion of the portfolio given all the risk factors?

RUSSELL THAM: Let me start by saying we invest in good opportunities regardless of whether it's listed or unlisted. As you can see from the performance, this sector has outperformed the listed sector. We value the [unlisted] portfolio on a book value less impairment perspective. If we were to mark to market, this unlisted portfolio value will rise another 10%. There are other benefits to it – if you look at the mix, there’s broadly three components there. One is mature assets that have been delivering a steady stream of dividends for us which is helpful. Two, we have a high quality diversified portfolio that is diversified geographically, sectorally, and by vintages, and you get a regular set of distributions. Finally, our early stage – that specific portfolio has done very well and it's around just under 10% of our unlisted portfolio and many of these have exited [early stage]. I think this portfolio is high quality, and generates reasonable liquidity for us too.

ROHIT SIPAHIMALANI: I would like to emphasise two things. One is that, you alluded to the point of risk. Actually, we don't see the unlisted portfolio as being higher risk. In some sense, it's lower risk because we can perform due diligence of these companies much better, we have access to much better information, we can have a role in governance of these companies. So, yes, there's illiquidity but we more than get compensated for that illiquidity premium based on the returns we've seen on this portfolio. But again, it's not a number or a target that we have – the percentage also varies depending on how the public markets do. So, last year when the public markets were very high and valuations were high, the share of the unlisted portfolio was lower, and this year, part of the reason it's gone up is also because of a decline in public market valuations.

LIM MING PEY: I just also want to add, I think what Russell said is right. We always approach investments from a bottom-up perspective. Which are the investments that we want to invest in, whether they are listed or unlisted. So, actually, in a way the percentage of unlisted assets becomes a resultant number. As we move towards the trends, there are many early stage opportunities because of the nature of those trends and so they manifest themselves in certain parts of this segment. So, it's really what comes out of our core focus on our opportunities.

MARTIN FICHTNER: I would just make a small comment that I think it's one of our strengths – the ability to be able to invest in both listed and unlisted assets. It is the best way that we can come up with to invest, against the trends that we see and build that resilient portfolio and from an investment team perspective, I think we get the benefit of taking insights on this side and deploying them over there or vice versa.

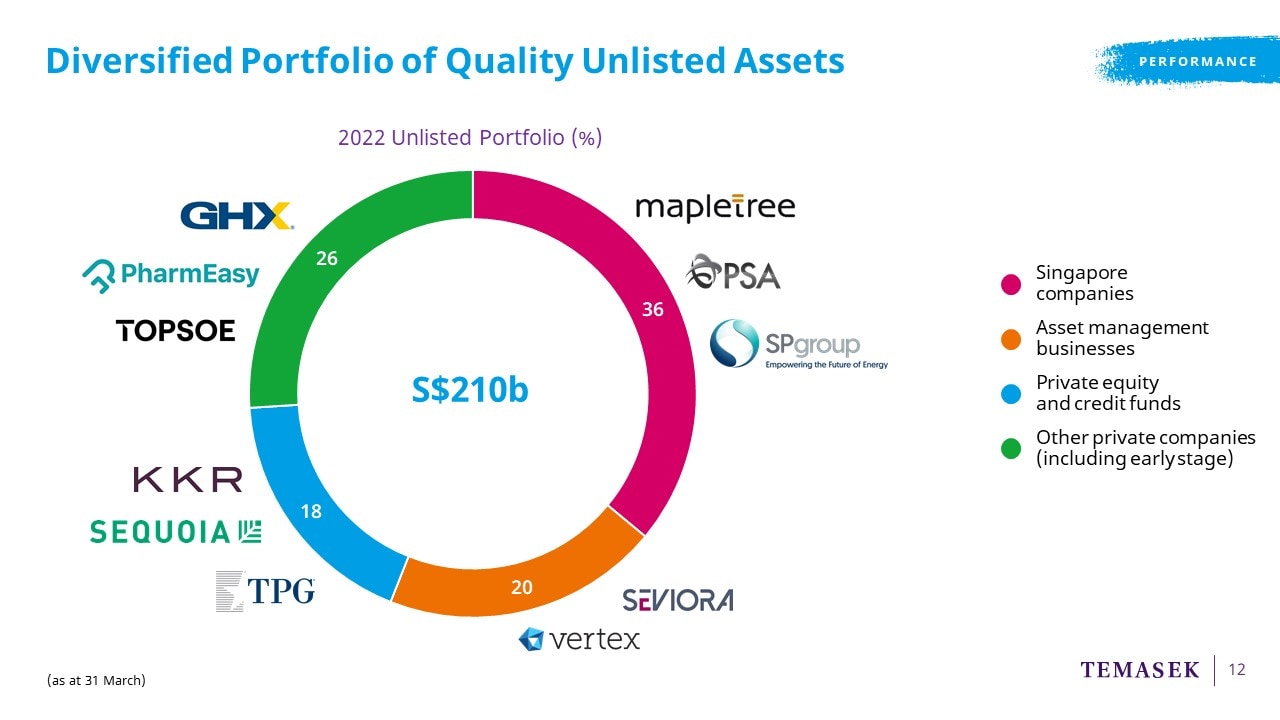

STEPHEN FORSHAW: There's a slide on the screen right now that gives a bit more colour to the unlisted portfolio, to give you an indication of how our unlisted portfolio is broken up.

Question on Investment – Unlisted Assets (2)

QUESTION: With most of your portfolio in unlisted assets now, I just wanted to understand a little bit on what the exit environment is like. The public markets are down now, so is there anything you have to do to adjust for your portfolio companies?

ROHIT SIPAHIMALANI: Maybe we can get that slide back up.

You will see that some part of the portfolio – the largest chunk – is actually some of our Singapore companies that we've held for a long time, which we see as a steady source of dividends for us – so companies like PSA, Mapletree, Singapore, et cetera. There's another section here which is our investment in funds, third party funds. It's a very diversified portfolio and they have their own cycle of distributions and sales, which would be through either M&A or by listing in the public markets. And while in the near term there may be an issue in terms of public market listings – these are investments made over horizons of at least four or five years – we don't see an issue from that perspective.

So, again, it's not something that concerns us. We're not looking at immediate liquidity in the next 12 months or so from some of these companies. I feel fairly confident that if the companies do well, we will have good exit opportunities both in the private and public markets over the next few years.

Question on Investment – Unlisted Assets (3)

QUESTION: Your financial year ends March 31. We've since seen the markets go further down. Does that mean we see an acceleration into even more unlisted assets probably in the coming financial year, and possibly even more Singapore-based companies given the performance of the markets since March?

ROHIT SIPAHIMALANI: Our listed-unlisted proportion is really based on value and opportunity. In fact, arguably, I would say that today, the public markets have corrected much more and the private markets have yet to correct to the same extent. So, in some cases we may do more public market opportunities before we do private. But if we do see private market valuations correct, and we're beginning to see that, and we see the right opportunities, we'll invest in private markets. But we don't really have a goal of listed and unlisted.

LIM MING PEY: I think this is worth emphasising: we don't have a private asset allocation goal. From what you see from our private assets – at the risk of repeating, let's call the chart up again.

Each segment of the unlisted asset portfolio serves different purposes and gives us different value. They're not in and of itself because they're private. So it's really looking at the dividends that they may give us, the co-investment opportunities, the insights that they give us, the early insights from the early stage companies that they give us. That's quite important, so we wanted to clarify as well.

ROHIT SIPAHIMALANI: And I would say the other part we're very happy about is the balance and resilience we have in our portfolio. You mentioned the fact that markets have come down since 31 March. But actually the only market that's had a positive return since 31 March is China, which is the one which had negative returns for us last year. So, this balance, you know, last year, the years before that, there was a period where the Singapore market didn't do very well because growth was getting more compensated for than value, and Singapore is more of a value market. But in the last fiscal year, Singapore was one of the better performing markets because it was more value-oriented. For us, when we look at resilience and long term portfolio construction, we want to make sure that firstly, we look at all scenarios and how the portfolio would perform, so we're not unnecessarily biased towards one scenario; but secondly, we look to have the balance to make sure the portfolio is resilient across environments.

Question on Investment – Portfolio by Geography

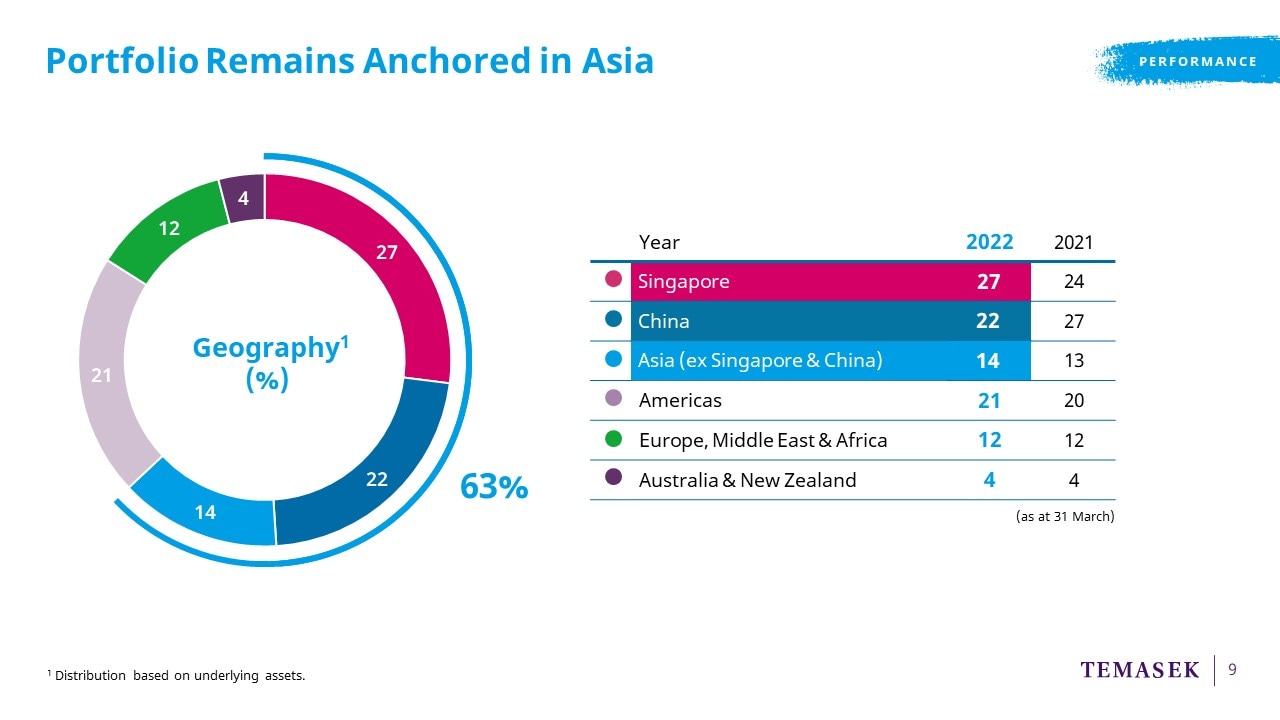

QUESTION: A technical point on geographical asset allocation and definition: when I look at a result saying 27% of the portfolio is in Singapore, I believe that means the legal domicile or the listing of the enterprise itself. If you were to look instead at the underlying geographical exposures of portfolio companies, would you end up with a different geographical mix than the one that you have?

ROHIT SIPAHIMALANI: Actually, just to clarify, what we've shown out here is the underlying geographical exposure. This is not by country of listing or incorporation. So, the reason we show it that way is so you get a sense of the actual exposure of our portfolio.

Question on Investment – Portfolio by Sector (Telecommunications, Media & Technology)

QUESTION: I want to ask about Temasek's TMT sector. It's the largest drop in the sector for FY22. Did Temasek rebalance its investments in this sector or was it a mark to market loss? And also within your Development Engine, there are many investments in the technology sector. Will we see a tech-heavy portfolio from Temasek in the future?

MARTIN FICHTNER: I'm going to start with the second part because it highlights one of the reasons that we focus on trends.

Digitisation is something that is not just a technology element, it's something that touches the economy in general. And, therefore, investment around technology and technology-enabled business models shows up in many different parts of the portfolio. To pick an example out of fintech, it really depends where the company's core business and core focus is and our thesis for that company. So, we may have a company like Adyen, for example, which sits in the financial services portfolio – at its core it's a financial services business. But we also have an investment in a company called Duck Creek which provides back office enterprise software for insurance companies. That does sit in the TMT portfolio.

In terms of the sector allocation percentage, it has to do primarily with a valuation correction in the technology sector. It doesn't have to do with a rebalancing of the portfolio in any way, shape or form. It is a core sector for us.

LIM MING PEY: If I can also add on, moving forward, we're seeing a lot of convergence. So, we ourselves are looking at our four trends, how they are converging. So, something like digitisation that pervades all our trends, is it really just technology or not technology? So, we are encouraging our own teams to think cross-functionally and work towards those converging opportunities which we see a lot of value in.

RUSSELL THAM: Part of this also requires us to go very upstream early in technology investments. I think one of the key benefits of going that far upstream in the cycle, is that it allows us to gain a lot more insights than what it means to our portfolio down the road. Coming back to this, this certainly helps us construct a much more forward looking, much more resilient portfolio on an ongoing basis.

Question on Investment – Portfolio by Sector (Life Sciences & Agri-Food)

QUESTION: Can I ask about the agri-food sector? The pandemic and the war have proven the importance of food security. Have you changed your strategy towards investing into agri? Have you narrowed down the sector? And if you have changed the target, can you share with us?

RUSSELL THAM: Temasek has been a very active global investor in the agri-food tech space. We've invested in a lot of companies where technology is a key differentiator. Just to cite a couple of examples, we have invested in Rivulis, a micro-irrigation technology company, we've invested in an array of alternative proteins, we've invested in even seed genetics for vertical farming because we think urban farming will be more critical. We've invested in a broad array, as I mentioned earlier.

Coming back to a Singapore angle, recently we announced the Asia Sustainable Foods Platform, this is where the platform is designed to help food tech companies in three ways: in the R&D context, in the manufacturing area, and also in go to market. If we take all this in totality, Temasek is continuing to lean in because it is a key structural trend for us. At the same time, we believe many of these companies will enhance food resilience and food sustainability. So, our stance hasn't changed. We continue to invest in this sector.

LIM MING PEY: Actually not only has our stance not changed, we've been active in agri-food for some time because of the relevance in the sustainable living trend. Even in the investments that we've been making on alternative proteins, all these are with the stance of, how do we have better ways of producing food to feed the planet?

So while it was not maybe motivated by COVID per se, we start to see a lot of complementarity in food resilience, food security and how that's playing out in our original investment stance in agri-food as well.

Question on Investment – Crypto

QUESTION: I noticed you've made quite a few investments in the crypto industry over the past year, including in the popular exchange FTX. I was hoping you could explain what opportunities you see in this industry and how your outlook for the sector has been impacted by the recent crash in crypto markets?

MARTIN FICHTNER: Blockchain as a technology is an important innovation and it's going to have a long gestation period. We believe it's going to touch a lot of different parts of business and the economy. That is the reason that we focus on it and that's the reason we set up a pod four years ago to begin understanding the technology and the opportunities around it.

Our focus is broadly on blockchain-enabled solutions, platforms, infrastructure and some of the applications, and exchange is an example of that. So FTX is an example of that. But by no means are we only limited to making investments in something like FTX. We are also, as part of our Development Engine, building some companies ourselves. We've set many of them up.

In terms of the current market environment, this is part of a cycle of innovation that goes on. Again, we take a long term view and a long term investment horizon. Cryptocurrencies in particular, which is what I think you're referring to, our exposure to crypto currencies is minimal and it's primarily through venture funds that invest in crypto-related projects and companies. As I said, we are focused on more broadly, the application of the technology and the companies and the opportunities that are going to emerge from that.

LIM MING PEY: Actually, if I may add, I think despite the recent attention on cryptocurrencies, it is important to understand that blockchain, decentralised technologies and Web3 actually entail a lot more different components and opportunities in the value chain. So, we are looking for those transformation opportunities that will really disrupt many different industries.

MARTIN FICHTNER: This continues to be a great example of how we think about building that resilient and forward looking portfolio. It's important to understand how a technology like this, how an innovation like this, is going to touch, yes, financial services and help innovate financial services over a long period of time, but other parts of the economy as well. We're seeing it touch consumer companies, we're seeing it touch media companies now, and it's going to go broader than that.

RUSSELL THAM: If I may add, I think as part of our investment engine strategy, this particular engine is called the Development Engine. This engine is designed to identify and build future-centric capabilities. So, blockchain is one of the four verticals we have selected to build up capabilities in it. The others are AI, Cybersecurity, Digital solutions, and Sustainability Solutions. You’ve got to look at this in totality. This will put us in a much better position to build a forward looking, resilient portfolio.

Question on Investment – Crypto (2)

QUESTION: A follow-up question on a crypto question: how have you seen valuations of firms that you've invested in such as FTX or Amber being impacted during this current downturn?

MARTIN FICHTNER: In terms of valuations of some of the crypto companies that we might have invested in, I won't comment on any of the companies specifically. It would not be appropriate for me to do so. What I can say, though, is that in general, we're seeing a cycle from a valuation perspective happening right now and valuations for higher growth companies that have profitability further out, have come down. Some of that is starting to trickle into private company valuations as well. What we focus on is this: are the businesses healthy and are they growing, and do we think the prospects are strong? There is no mark to market on a daily, quarterly, et cetera basis, and we feel strongly about the companies in our portfolio performing well over time and we'll see cycles in terms of multiples go up and down as the cycles occur.

Question on Investment – Singapore-based Portfolio Companies

QUESTION: We've seen a fair bit of consolidation in the Singapore portfolio. Does Temasek see more scope for further M&A opportunities given the market downturn?

LIM MING PEY: It's important to remind ourselves of the governance principles that we operate under. So, we look to the boards and the managements of those companies to consider their own M&A plans or strategies. As a supportive shareholder, we will always listen out to those opportunities and then we make our own evaluation as a shareholder.

ROHIT SIPAHIMALANI: We do want these companies to scale up, be globally competitive, and therefore you've seen we've been investing in the Singapore companies in a post-COVID world to help them be more competitive and to manage the green transition. So we will continue to do that but the opportunities and the decisions of what actions to take really is up to the companies themselves.

Question on Investment – Element Materials Technology

QUESTION: This year we saw a rare instance of Temasek buying 100% of a company – Element Materials Technology. Can you explain the rationale behind that, and are we likely to see more of this happening?

ROHIT SIPAHIMALANI: So, you're right, it's not something we do very often. It's not, however, the only time we've done it. About three or four years ago, we bought GHX in the US. We have made occasional controlled transactions of that nature. This one was a company we knew very well, because we were already a minority investor in the company and had been for the last few years. So, when the majority shareholder was looking for an exit, it was in a space where we see long term secular trends around testing, inspection and certification. They also were leaders of sustainability within that area. It was an asset we felt we could own for the long run and add a lot of value to, and it was synergistic to our ecosystem.

So we will do this. I don't think they will be very frequent but when we know a company well, feel convicted about it and it's aligned with our long term trends and focus areas, I think we will look at such opportunities selectively.

Question on Investment – Sembcorp Marine Ltd

QUESTION: It was mentioned that Temasek continues to invest in some of the Singapore companies, one of them is Sembcorp Marine. Can you explain a little bit of the thinking behind the investment in Sembmarine, and what will Temasek do if the plan to merge Sembcorp Marine with Keppel Offshore & Marine doesn't go through?

RUSSELL THAM: We made a commercial decision to invest in Sembcorp's 2021 rights issue. The purpose then was to strengthen its balance sheet and its liquidity position. Within that, there was also the plan to enable Sembcorp Marine to proceed with its transformation journey and it was stated then that this includes a proposed merger with Keppel Offshore & Marine. That was designed to help them pivot into better opportunities within the clean renewable space.

So, on the second question, if it doesn't go through, we don't speculate on hypothetical scenarios. But we have noted that the Sembcorp Marine management has indicated their liquidity position, and it should be good to at least end of 2023 as a standalone entity. So, I think that's where it is right now.

ROHIT SIPAHIMALANI: I think the important thing is that I think both management teams – the boards of both companies – have clearly articulated benefits they see in the merger and we do believe that a combined entity in this competitive environment would be much more able to compete globally and more importantly, effectively manage a transition to the green economy in terms of the types of things they can do.

RUSSELL THAM: Temasek is supportive of the combination and we think it's a compelling proposition, especially since it enables them to make a transformative next step which I think will create shareholder value all round.

Question on Investment – Zilingo

QUESTION: Just a quick Zilingo question. The board-backed investigation by Kroll was concluded, but at the very least, Temasek was on the board for two years when the company had a lot of failings and failed to file its basic financial audits. I realise this is a problem that you've inherited rather than developed, so I apologise for asking you the question. But what are some of the lessons that Temasek has learned from this and what will you change in your approach to governance because of it?

ROHIT SIPAHIMALANI: I would say firstly, we believe in the highest principles of governance and expect that of all our companies, and we also rely on the boards to drive that governance. As a shareholder, we engage with the boards but we see the primary responsibility of managing that governance is with the boards of these companies. Clearly, the company went through a tough time during COVID and there were a lot of changes that happened. There were clearly some things that the board was not aware of and when there were complaints made, they investigated and actions have been taken subsequently.

Question on Macro Outlook

QUESTION: You mentioned a slowdown in investment pace this financial year amid the global economic outlook. Could you expand a little bit on that, please?

ROHIT SIPAHIMALANI: We're in a bear market right now in the US, Europe and we have been in China for a while. The decline in values in markets like the US has almost been entirely a function of rising rates, and we still haven't seen an earnings decline being priced in. We think that is inevitable as we go through this year. So, we see further downside in the markets from that context.

If you look at Europe, I would say the situation is even more acute because not only do you have high inflation, slowing growth and tightening policy, you have the initial problem of the Russia-Ukraine crisis which is creating an energy crisis in Europe, which could clearly aggravate the situation much more.

China's actually at the other end of the cycle, where it's early cycle and I would say the risk-reward ratio is more balanced right now given the starting point of valuations, and also the flexibility they have on the fiscal monetary front. But overall, I would say the profile, even in China, if you have a recession in the US, and Europe, China will get impacted by that too.

So, the economic outlook is not looking very good. We see further downside in the markets and I would say, historically when you’ve had a bear market like this, you only trough after the Fed has shown that it's stopped tightening and is moving towards the policy of easing. Given the Fed's current stance we don't see that happening quickly, so for that reason we think this could be a prolonged downturn extending through the end of the year, potentially into some time in 2023.

All these cause our cautious outlook. At the same time, we look for opportunities aligned with our long term trends. We want to continue building a sustainable and resilient portfolio for when we get out of this downturn, and we will continue to invest. But for the reasons I mentioned, we are more cautious than we would have been, say, a year ago.

Question on China Outlook

QUESTION: My question regards China. The period under review included an era of some debate about the investability of China, chiefly as a question of the unpredictable nature of regulation which must have affected some of your holdings in the tech sector, and I do notice China as a proportion of the portfolio has dropped from 29% to 22% over the last couple of years. Is that reflecting weaker market performance in China or have you consciously chosen to step away a little from your previous allocation towards China?

ROHIT SIPAHIMALANI: We continue to see China as an important market for us. We've been there for almost 20 years, and we’ve seen many cycles. Over the last decade, I would say it’s been the best performing market for us, even including the last year. So, it continues to be an important market for us.

The movement you saw in the portfolio last year was, in fact, entirely due to market price movements. In fact, we were a net investor in China last year. We were also a net divestor the year before that because we saw that valuations were very, very high. But we have seen attractive opportunities even in this volatile environment and continue to invest in China right now.

RUSSELL THAM: So maybe I will just add onto that. Given that we been there for almost 20 years, we have seen through policy cycles, we have seen through economic cycles, we've seen through various phases of economic development and we remain invested there. We constantly reshape the portfolio accordingly.

MARTIN FICHTNER: Even if you look at specifics around the trends that we invest in, there are very compelling opportunities in China – the rise of software, the rise of automation, the rise of deep tech in China do provide us with attractive investment opportunities now and in years to come. This is very much aligned with the key trends and the key themes that we have, in this case, I picked examples around digitisation but it's true across everything that we do.

Question on China Outlook (2)

QUESTION: What has been the biggest change in your China investment strategy over the past year? A lot has changed in the country for investments. How do you see this shaping forward? As a global investor, where do you see opportunities for investments now?

ROHIT SIPAHIMALANI: In China, a lot of opportunities align with our trends around digitisation, longer lifespans, sustainable living and future of consumption, so that could hold true. The two areas where we have been more focused on in the last year or two – one is basically looking at policy and making sure that whatever we're doing is aligned with policy. And in that context, the platforms are a good example there. We think that most the regulatory headwinds are behind us there. But it's nothing new in China — around the world people are concerned about monopoly power of the big tech companies. They're concerned about data issues. It's just the pace of change that we saw in China was faster than what anyone expected. So, we obviously have to keep policy in mind in whatever we look at out there and make sure we're aligned with policy.

I think the second thing that has been exacerbated is the polarisation of tension between US and China aggravated by the Russia-Ukraine war. It's something that we've always looked at, but we have to focus on it even more to make sure the businesses we focused on are self-contained within the China economic sphere, both from a market perspective and access to technology perspective. There continue to be many opportunities of that kind. Sustainable living is an example where China is the largest EV market in the world, it's building the whole value chain within it, it has access to minerals that go into it, so that's a perfect example of something which is aligned with our trends, aligned with government policy and actually is not negatively impacted by things that I just talked about.

Similarly in the area of consumption, and the government wants to encourage consumption, there are areas out in the domestic brands coming up – we invest in a company like Genki Forest, et cetera. There will continue to be opportunities of that nature. There's lots of opportunities we see out there in China.

MARTIN FICHTNER: We can go to the other question in terms of where we're seeing opportunities globally. Again, in many ways, the simple answer would be, we would go back to the four trends because underpinning those four trends are specific areas with specific strategies that we have to pursue. The gestation period for investments don't change immediately and on a dime. In longer lifespans, there are elements around infectious diseases that have become more relevant now as we've lived through a pandemic. But things around ageing or things around digital health and population health are themes that are of a longer term nature and will continue playing out.

If you go through each of the key trends within each sector and how we're playing on those, we're sticking to what we're focused on – financial services, the continued digitisation and innovation of the financial services sector, market infrastructure, payments – continues to be an important trend and I can go through each one of those. We do recognise that the environment shifts and maybe some opportunities become more attractive right now than others, but the core focus stays the same.

ROHIT SIPAHIMALANI: The only additional thing I would say is that compared to the last two years the one area where we're seeing many more opportunities, because you're seeing maturing of these opportunities is around the sustainable living trend. While there are early technologies, there's much more activity happening, there's lots more capital development in those companies so that's one area where I would say at the margin, compared to two years ago, we're seeing many more opportunities today.

RUSSELL THAM: Specific to China, there's a lot more emphasis on foundational technologies, enterprise-level technologies, and I think that's also in the area where, from a policy standpoint within China, there has been a big focus in addition to putting a lot of policy focus on enabling China's economy to transition to a low carbon economy. Those will play out over the next 5, 10, 15 years.

Question on Japan Outlook

QUESTION: Have you invested anything new into Japan in the past year, and what's your outlook now that the yen is at its lowest in the past decade? What's your evaluation for the country’s economy?

LIM MING PEY: In terms of our outlook, we do see near term support for growth, especially with the gradual reopening domestically, but as we shared just now, there are headwinds building up in the external environment, so growth could slow down in the second half of the year.

You also mentioned the yen weakness. I think we do see weakness because of a divergence in the US and Japan policy positions, but the divergence and the weakness should slow down from this point onwards.

ROHIT SIPAHIMALANI: I would just like to add that I'm very pleased to say that we've actually committed a billion dollars to our subsidiary, Pavilion Capital, to seed the fund that's going to be specifically focused on Japan. That will be the main vehicle through which we expect to be investing in Japan over the next few years. We will be looking forward to that.

Question on Sustainability

QUESTION: Can you share more details about the decarbonisation plans that Temasek has for its portfolio companies? And also with regard to the wider environment on ESG investing, which has also not been so hot in the last few months – how do you think this would impact the decarbonisation plans for your portfolio companies?

RUSSELL THAM: To start off, from Temasek's perspective, sustainability is at the core of all that we do. It is a journey, so I think that's important to remember. First off, Temasek has been a very active advocate for better disclosure standards globally. We are encouraged to see that various global committees and task forces are being set up, so we will continue to push on that front.

At the firm level, there are a couple of initiatives, as my colleague has mentioned. We have priced carbon internally, we have raised the price as we head towards US$100. We have sustainability-linked incentives for the staff soon. We have put in place ESG frameworks that is part of our investment strategy.

Secondly, on the investment front, we have been fairly active in investing across an array of climate-aligned opportunities, ranging from hard-to-abate sectors, to built environment, to hydrogen-related green technologies. So, that is ongoing.

We have also been actively establishing platforms. Recently, if you followed the news, we set up GenZero. We’ve put S$5 billion aside there to help accelerate decarbonisation globally to the point of working actively with our portfolio companies, so yes, we are active in that regard. You’ve seen a couple of examples in the video earlier, in Tampines Central [related to SP’s district cooling].. We have also recently partnered with SIA to launch sustainable aviation fuel. Coming back to that, it is a journey, we're fully committed, we have a multifaceted strategy, it’s multiyear, multipronged and we're executing to it.

LIM MING PEY: I think the second part of the question when you talk about ESG investing, there are two different aspects to ESG investing. Like Russell said, when we invest, we already have an integrated ESG framework that is incorporated into the due diligence of all our investments. That's how we are doing ESG investing. In other areas like impact investing, we've set up a dedicated team internally that's looking at impact investing because we believe in the value of investing for impact and for sustainability. So, it's a journey. I think we continue to work on this and we hope to see more of this becoming mainstream in the years ahead.

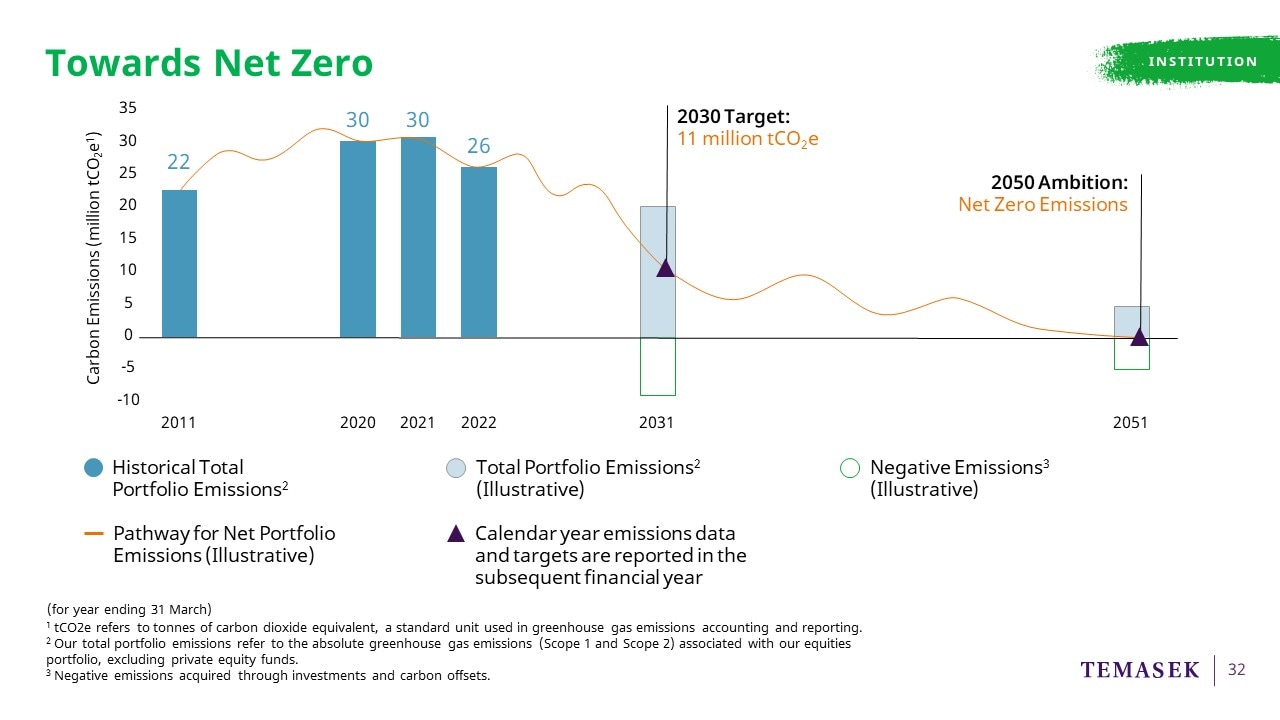

ROHIT SIPAHIMALANI: You can see we're doing a lot and I think part of it is because we're so committed to this. We've stated our goals of producing the carbon footprint of our portfolio by 50% from 2010 levels by 2030, which is about a two thirds reduction from 2020. That's a very, very high bar and we know it's not going to be easy, but we think it's important, and therefore we are all very committed to it.

Question on Sustainability (2)

QUESTION: You have stepped up investments in sustainability. How will your investments in sustainable technologies and companies contribute to improving Temasek’s investment return? Additionally, since Russia’s invasion of Ukraine, there has been a global trend against decarbonisation. Does Temasek see these setbacks as temporary, or has the paradigm shifted since the war in Ukraine?

ROHIT SIPAHIMALANI: One of the things that the Russia-Ukraine crisis highlighted on the energy front is that energy transition can't happen overnight. It is an expensive thing. It will take time, and it will have to be a journey. People have realised the need to have transition fuels but it’s also, if anything, from a medium term perspective, even accelerated the need to move away from fossil fuels and move into more sustainable fuels.

You can see that at the forefront in Europe. Even though they have brought some coal plants back on stream and so on and so forth, they're talking about much more aggressive goals towards decarbonisation over the next decade or so. As you pointed out yourself, it's probably temporarily just to meet the requirements of energy for the world. You may have some going back to fossil fuels, et cetera, but I would only think it's accelerated the long term trend towards the transition.

RUSSELL THAM: I fully agree with Rohit. This energy transition is a long term journey and Temasek is a long term investor. We have been relatively active in investing in future green technologies. To cite a few examples from a primary energy sector perspective, we have invested in geothermal energy generation, and in things even further out like fusion energy. We have started investing in green hydrogen production technologies and the respective carrier technologies that will move hydrogen around. Temasek is actively deploying capital there knowing it is long term, but we are a long term investor. The structural trends align, and we remain committed. This is also part of our sustainability journey.

Question on Sustainability (3)

QUESTION: Temasek has mentioned that it is not going to set hard targets on decarbonisation for your portfolio companies. Today, it laid out three strategies of how it intends to do sustainable investing. For its upcoming investments which include certain carbon-intensive sectors – is there a harder stance coming up?

RUSSELL THAM: We do not have a “harder” stance. I think we, as a long term investor thinking about how we construct a resilient, forward looking portfolio in the context of sustainability. We assess specific value chains, for example, we think the hard-to-abate sector is something we should participate in. We think alternative clean energy sources is an area of interest we would certainly pursue. If we think hydrogen is something we need to preposition our portfolio, we would do it. That's how we look at it. We don't have a “harder” stance. As I said earlier, sustainability is at the core of all we do. It is a journey. We have developed, a multifaceted, multipronged and multi-year strategy and we are executing to it in a fairly agile manner, so we take it as it comes. But commitment is resolute.

ROHIT SIPAHIMALANI: To your point, clearly if you want to achieve those goals, in new investments, we do need to be of lower carbon intensity so we can lower the carbon intensity of our portfolio. You will see by and large the four trends we have, most of our investments out there are low carbon intensity.

Having said that, we also want to invest in some sectors or companies which may be carbon emitters today, but are working on a transition to be low-carbon emitters, which is why when you look at this chart, we've got this wavy line that says that our portfolio decarbonisation may not be linear. We may invest in a carbon emitter today which could see the emissions go up with the idea of reducing it further because we see it not only just being good for the world, but that's also where a lot of value can be created. If a company has been valued as a high-carbon emitter and we can work to transition that, it could be a lead to a significant re-rating of those companies.

LIM MING PEY: Russell has spoken about the new climate-aligned opportunities that we are looking for – in many instances, specific carbon negative related platforms or companies, and innovations that we invest in. And Rohit touched on the last point of how we're working with some of our existing portfolio companies like SIA on their ongoing decarbonisation journey.

RUSSELL THAM: We also became a founding LP (limited partnership) partner in the Brookfield Global Transition Fund. This is very targeted towards brown infrastructure and brown energy assets that we believe could transition well into a green orientation. This all ties together because having a good sense of which emerging technologies could help portfolio companies decarbonise is also a critical element of the overall strategy. These are not thought through in isolation. It's all linked together.

Another example of this being part of a broader ecosystem thinking is GenZero. We have also a particular track that we call carbon ecosystem enablers. This is where we invest in measurement, reporting, and verification technologies. We invest in consultancy companies that can sell carbon credits such as South Pole. We made quite a bit of investments which all come together in a broader strategy framework.