Video: Agility, Alignment, Accountability

We had our roots in a young and transforming Singapore.

43 years on, we have grown and branched across the globe.

From established businesses to disruptive start-ups, we see a world of investment opportunities.

We spot trends in the unlikeliest of places and constantly reinvent ourselves to stay ahead in a changing and challenging economy.

We map our ideas, chart our own paths and align them to our long term goals by fostering a collaborative spirit.

Within and beyond Temasek.

As a generational investor, we do things today with tomorrow in mind.

We seek to deliver sustainable value in the long run, to make a difference in what we do for our investment, our institution, and our community.

We look forward to the opportunities of tomorrow, embracing the change and all that it brings.

Anchored by agility, alignment and accountability, we invest for generations to come.

MICHAEL BUCHANAN:

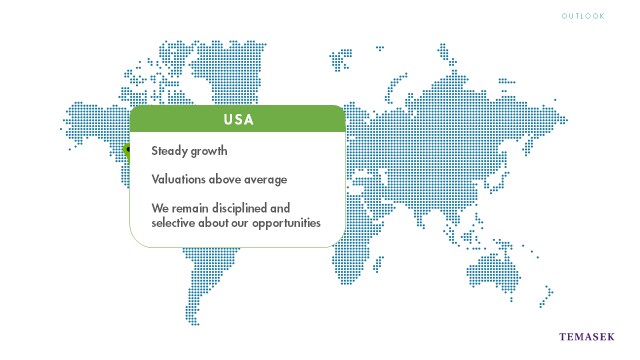

Well, thanks, Sulian and good afternoon, everyone. I'm Mike Buchanan and I will now go over our views on the economic and market outlook going forward. But first, a bit of a recap on last year.