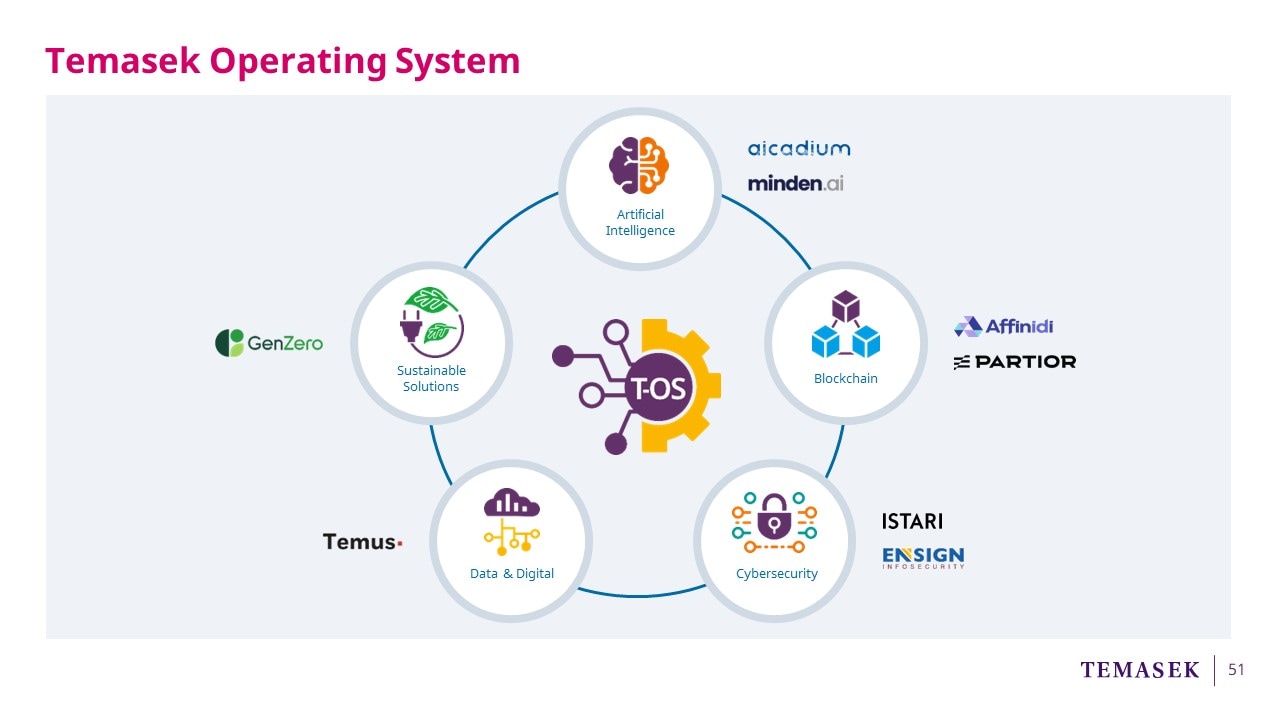

We have set up Centres of Excellence in AI, Blockchain, Cybersecurity, Data & Digital, and Sustainable Solutions, where we are building a suite of specialised, next-generation capabilities, which can differentiate us as a value adding investor and shareholder.

It is effected through venture building with the creation of use cases to attract talent in specialised verticals. It is about catalysing solutions for our portfolio as well as the marketplace.

It allows us to bring on board, grow and develop specialised talents using economies of scale, and offer them career pathways within our ecosystem.

We innovate new applications, business models and ventures, which is part of the entrepreneurial DNA of Temasek.

We focus on Value Creation and seek to Value Capture through the companies we establish as well as the companies that benefit from their solutions.

For example, Aicadium builds a team of AI talents, partnering our TPCs to co-innovate and scale AI products.

In blockchain, Partior is a distributed ledger technology provider enabling the next generation of cross-border payments and value exchange. It was founded in 2021 by J.P. Morgan, DBS and Temasek.

Istari is our global cyber platform based in London that acts as a trusted adviser to clients, deploying a portfolio of curated solutions. Its network has access to more than 3000 cyber professionals.

It has worked with Temasek’s cyber COE to protect Temasek and our ecosystem, and to make sure that we are cyber resilient. Our TPCs who use the services of Ensign and portfolio companies of Istari have improved the mean time to resolution of cyber incidents by 55%, which is close to the Cybersecurity and Infrastructure Security Agency’s benchmark, thereby enhancing the resiliency of our ecosystem.

Temus builds distinctive tech capabilities to accelerate the adoption of digitisation in our TPCs and others.

It has a headcount of 320 in total, including 230 digital talents since its founding two years ago. More importantly, it is contributing to workforce transformation through its "Step IT Up" programme, where it converts non-IT talent to digital talent in Singapore.

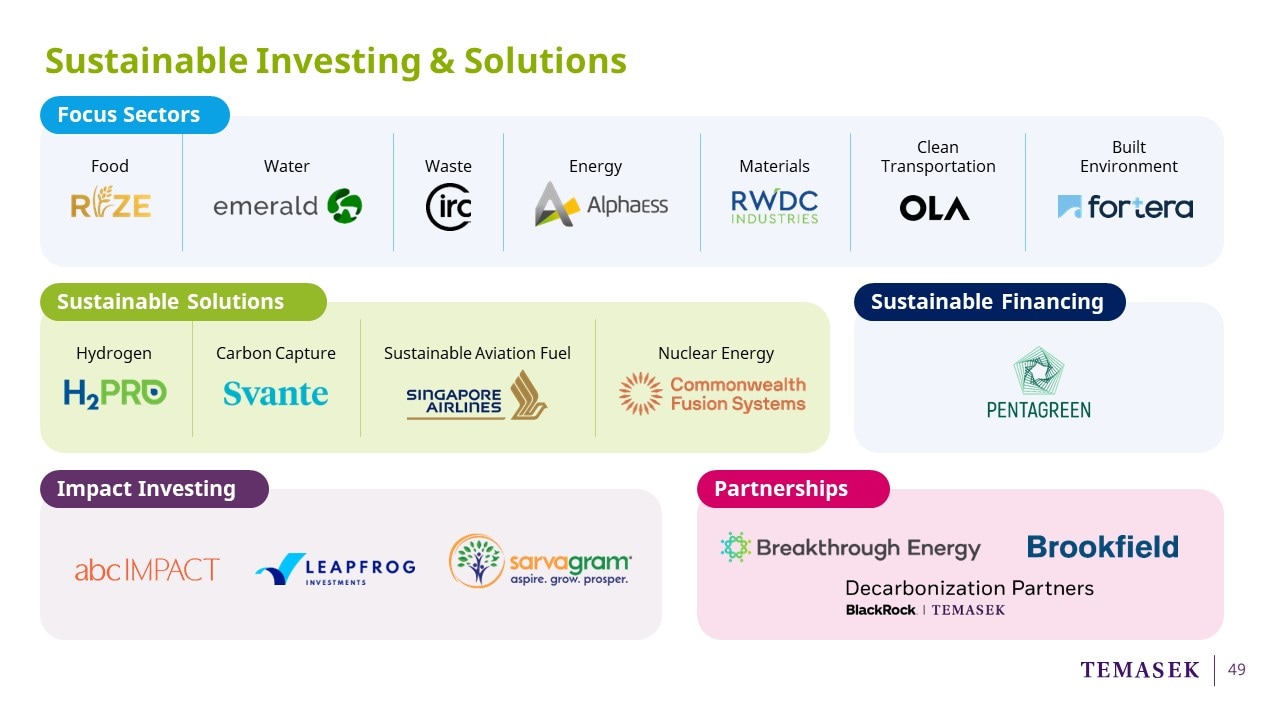

GenZero is our sustainable solutions platform focused on tech-based decarbonisation solutions, nature based solutions, as well as products and services. It has an initial capital commitment from us of $5 billion.

All these platforms have revenue and breakeven targets, and our intention is for them to have returns in excess of their risk-adjusted cost of capital.