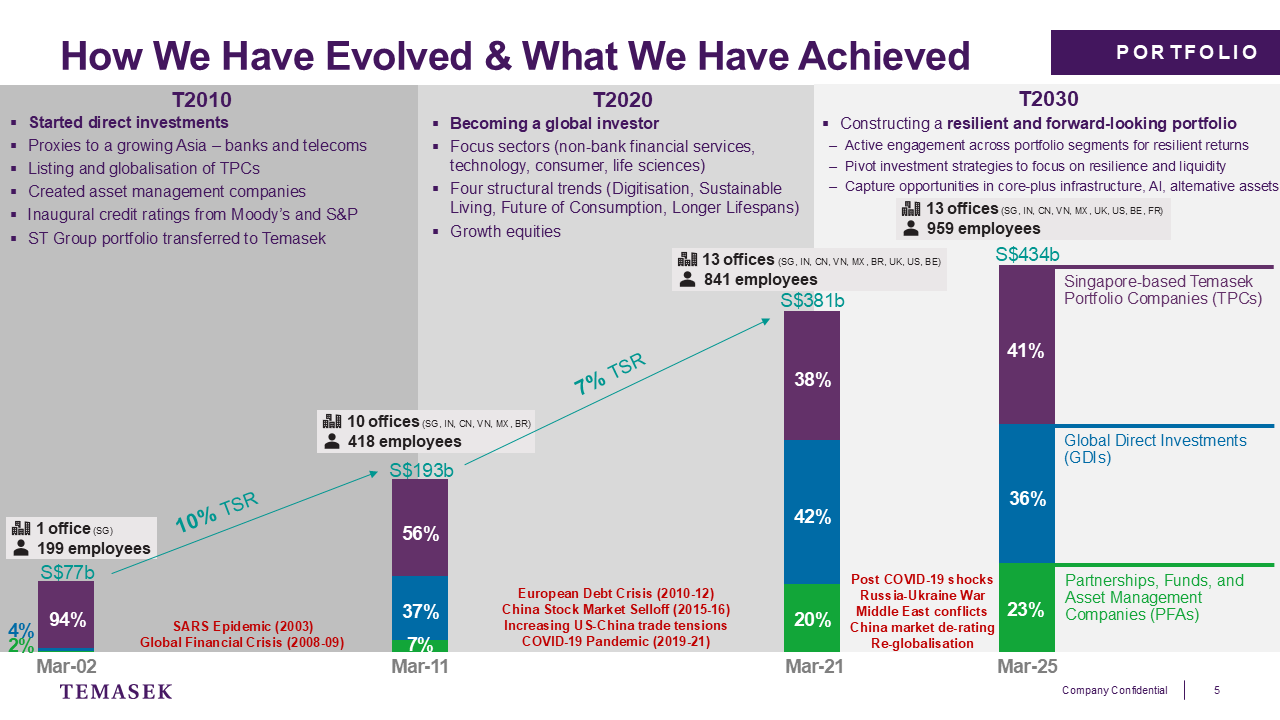

So let me just go through with you the journey that Temasek has been on, at least in the last 22 years.

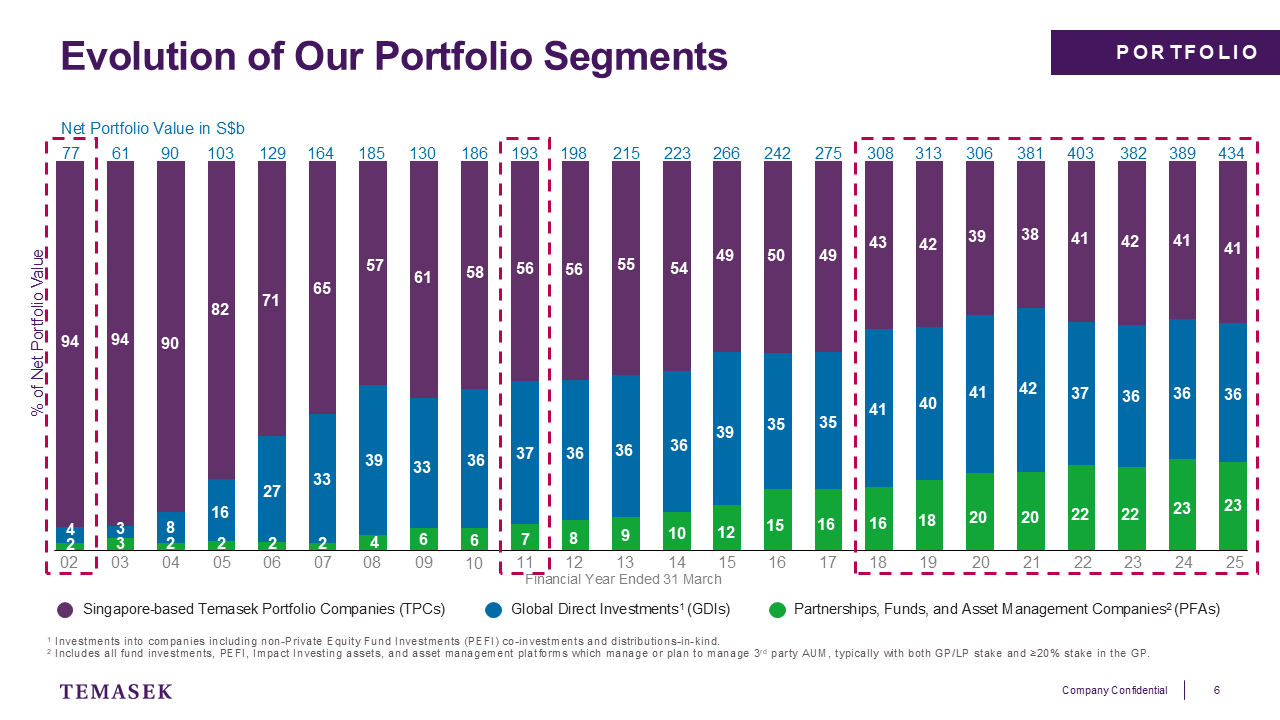

The first starting point would be in April 2002, when Ho Ching joined Temasek as Executive Director. Her mandate was to prepare Temasek to become a global investor. If you look at this bar chart, 94% of our portfolio value was in our Singapore portfolio companies, 94%. Only 4% of our portfolio was in global investments, and 2% was in funds and other instruments that we had.

And so she set about for us to start our direct investments. These were proxies to a growing Asia in the beginning, because we believed that we had to step up in Asia first, especially post WTO, where we saw that emerging Asia would be a winner in the context of globalisation. And so we started to invest in banks and telecom companies. Why? Because they were proxy for urbanisation, middle income populations in these countries.

We also started to look at globalisation of our Temasek portfolio companies, as well as listing some of them.

So I'll give you an example. PSA, at the time in the early 2000s, had only a small number of ports, primarily Singapore and a port in China. In 2004, 2005, we bought into Hutchinson Ports, a 20% stake and subsequently built a global port network. And today, we’re the largest independent port operator in the world.

We created asset management companies because we believed that there was an opportunity for us to bring products out to the broader market, and to help galvanise the asset management sector in Singapore.

We also decided to become more transparent and that entailed us doing two things: one is to publish our Temasek Annual Review. The first one happened in 2004, and in the same year, we decided to get ourselves a credit rating, Triple A, by both S&P as well as Moody's. And why did we do that? Because we believed that quite apart from the fact that our shareholder was a principal stakeholder for us, we should have other stakeholders who would be able to give a marker for how we would be doing, or could be the canary in the coal mine if we were not doing the right things.

There was also an interesting development at the end of 2004, where we merged ST Group into Temasek. So the Temasek today comprises portfolio companies that came from Temasek from its inception in 1974, but included companies that were built by the ST Group which came out of the Ministry of Defence from 1969 onwards. So to give you some examples, it would be Sembcorp, which came from the ST Group. So did Chartered Semiconductors, which we eventually disposed of in 2009.

And so ST Group was seen to be a little bit more entrepreneurial in actually establishing new companies and setting them up, and helping them to contribute to the ecosystem, whereas Temasek was very much a good steward of businesses that had been built by the Ministry of Finance and Economic Development Board.

Where did we end? Well what happened at the same time? So even though we were on a good trajectory, there will always be crises in any decade that you operate in. And the two biggest crises that actually impacted portfolio accretion in value was SARS in March 2003; as well as the Global Financial Crisis which started towards the end of 2007, had gotten into full swing by the third quarter of 2008, and was in full bloom by the time of the end of our financial year in March 2009.

Yet we did manage to achieve for the decade, a 10% TSR, and we went from S$77 billion of portfolio value to S$193 billion by 31st March 2011. But the big shift was that from 94% of TPCs to 56%, still the majority, and from 4% of global direct investments, that went up to 37%, a nine-time increase. So that was the first phase of the globalisation of Temasek’s portfolio, which was in line with stepping up in Asia first, and subsequently to other emerging markets before we decided to invest in developed markets.

Then came the plan for T2020. So Temasek does its strategies based on 10-year roadmaps. So first was T2010, second was T2020. (T2020) was implemented from 1st April 2011 to end of 31st March 2021. What were our objectives? The first was to become truly a global investor, and that meant not just investing in Asia, not just investing in emerging markets, but that we should have a more balanced portfolio, between developed markets and emerging markets. That meant stepping out to the United States and to Europe.

I'll just give you one statistic. At the beginning of T2020, US accounted for only 6% of our exposure, Europe accounted for 5%, so collectively 11%. By the end of the decade, US was 20% and Europe was 12%, so that’s 32%. So that was a massive shift when we decided that we will invest more into the developed markets, because we saw innovation and growth happening there, especially in the United States. And they were also deep markets for us to invest in across the capital structure, as well as through both private and public investments.

But again, there were shocks that came about that impacted our portfolio returns. The first was the Europe debt crisis, pretty much after the GFC from 2010 to 2012. Remember, it only came to a proper landing when Mario Draghi, as president of the ECB, said, “whatever it takes."

The second was of course the China stock market sell-off in 2015, 2016. There was also an exchange rate issue that came about in the same time. The third was emerging US-China trade tensions, which started in 2017 and accelerated towards the end of the decade.

But the most important of all was the COVID-19 pandemic. And although it started in China in 2019, it was again, in full bloom in March of 2020. So, you know, I think it's interesting for all our crises to have happened in March, because it happens to be our year end. So, you know, when everything's going well, come 31st March, the number that we are measured by gets impacted by something. SARS was March 2003, the GFC in full bloom was March 2009, and COVID in March 2020. I remember that, because that's my first year as CEO of Temasek International. I thought in January, we were going through a pretty good portfolio return and by the end of the year, we were minus 2.3%. It's never good to spend your first year in negative. But we achieved still a 7% (10-year) TSR, which means a doubling of our portfolio, despite these four crises that happened.

And again, you can see that the TPCs went from being a majority of our portfolio, 56%, to 38%. And the global direct investors went from 37% to 42%. But what really grew was the funds, the partnerships we have with others, and the asset management enterprises that we had set up, most of them with the objective of getting third-party money.

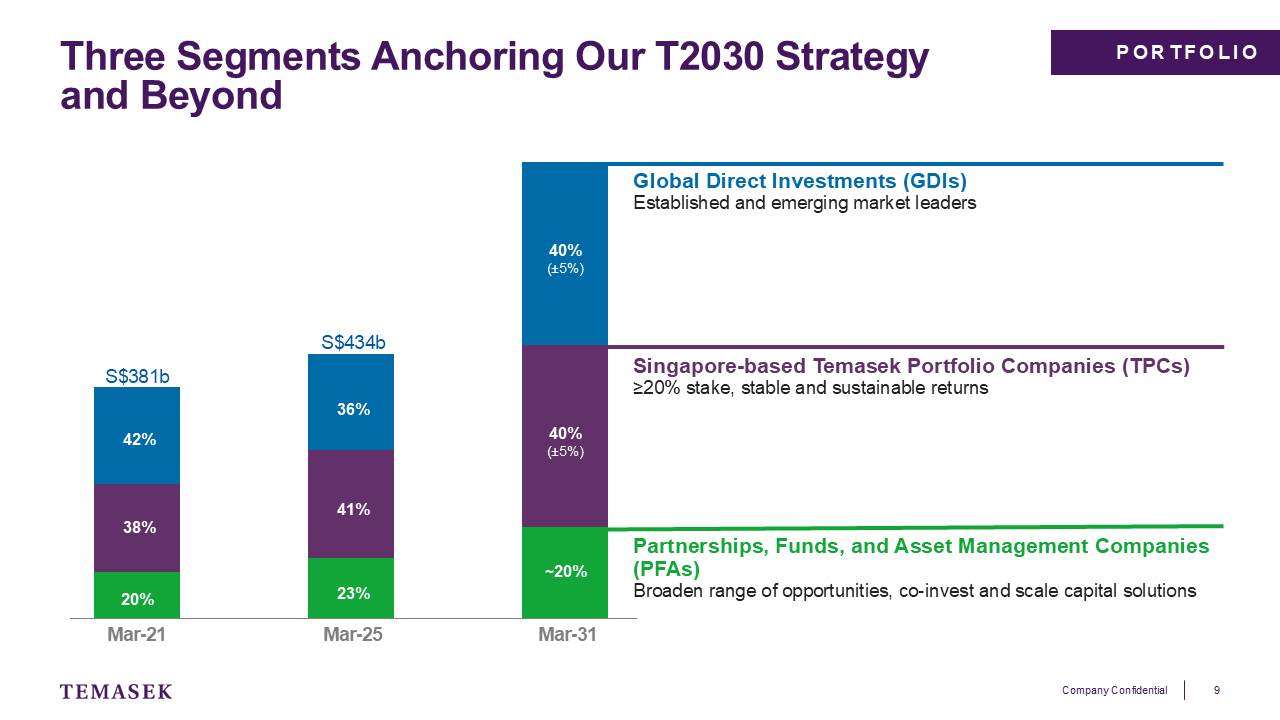

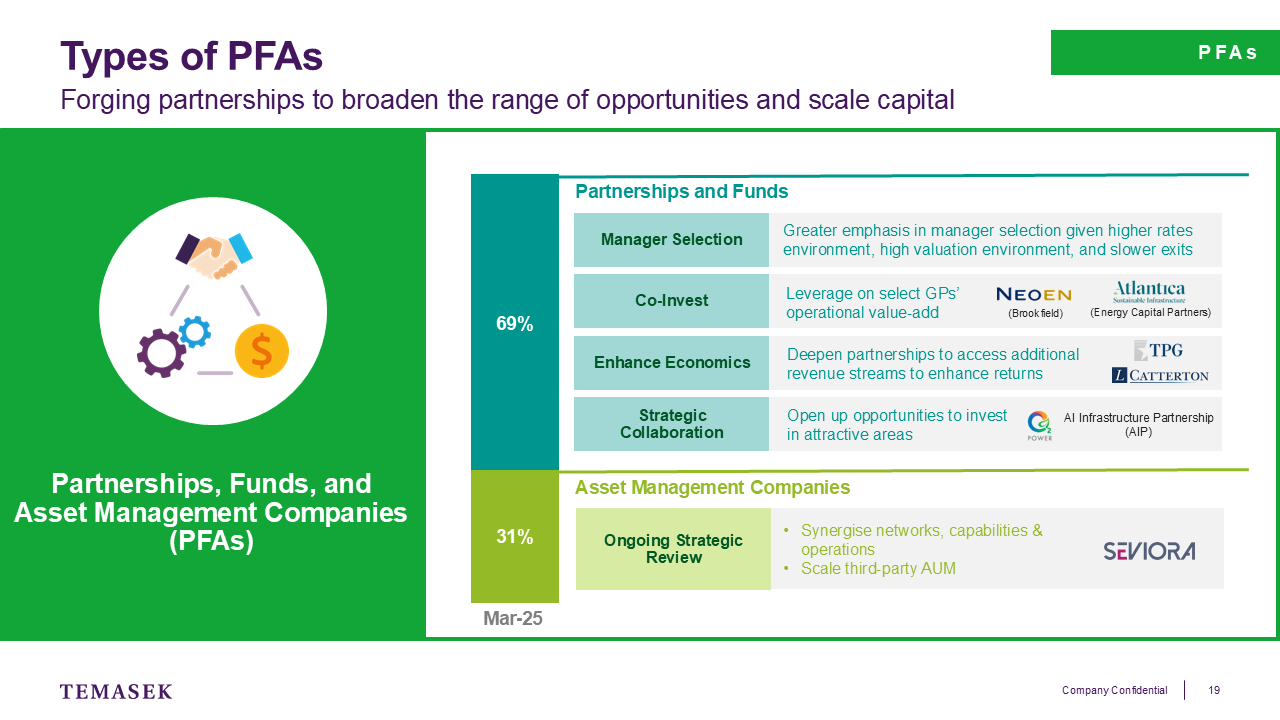

So where we are today, as at end of FY2025, is that our portfolio value is at S$434 billion, but the shift, the portfolio weight between Global Investments, Singapore and the Partnership Funds and Asset Management Companies, has remained fairly constant. It’s 41% for the TPCs, 36% for the GDIs and 23% (for the PFAs). So this 40-40-20 that we are thinking about for the future, which I will elaborate in a short while, has been fairly constant for us for some time.

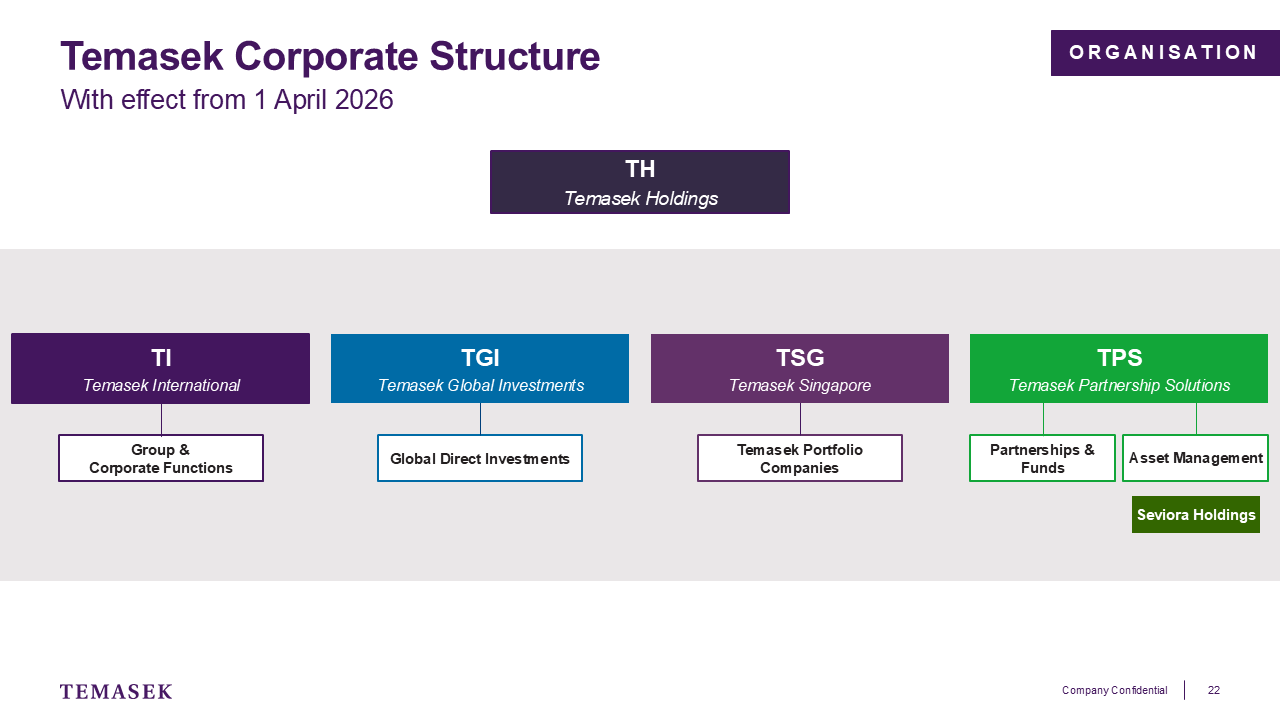

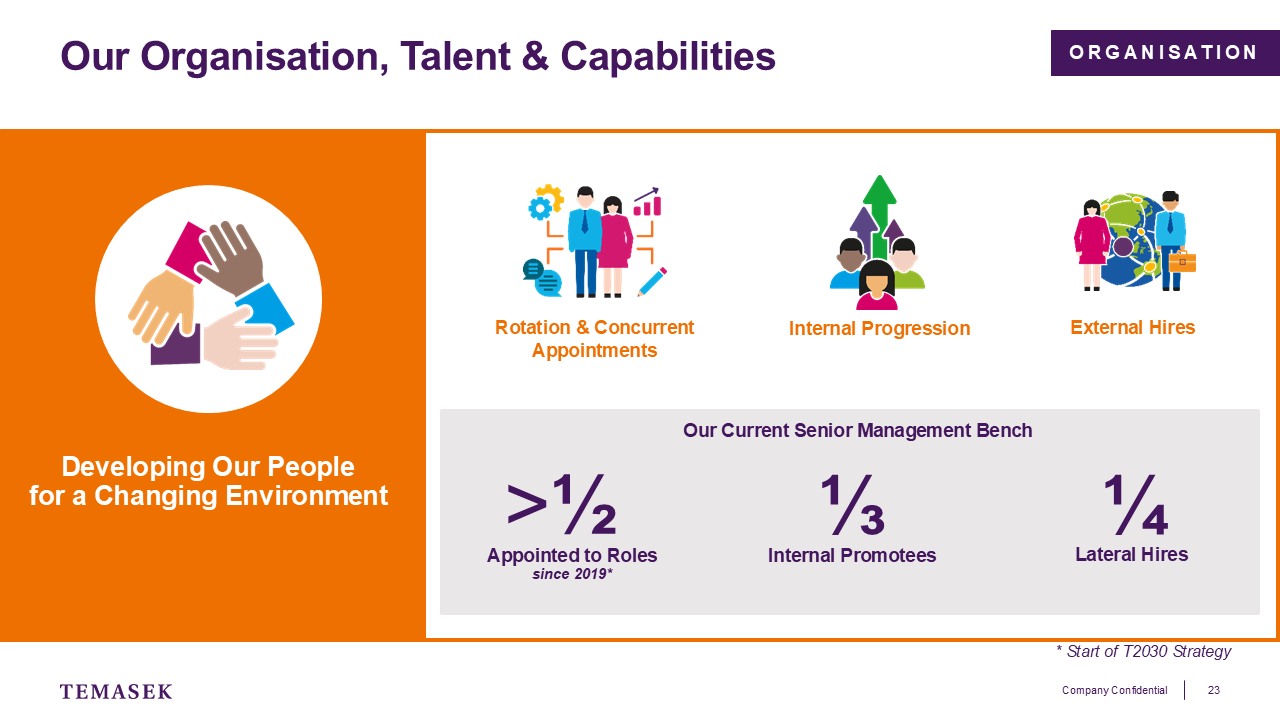

But at the same time, we have also evolved as an organisation. From one office at the beginning of 2004 with 199 employees, we then ended the decade with 10 offices. We first opened up in Mumbai, in Beijing, Shanghai, and Ho Chi Minh City in 2004 and 2005. We then opened up in Hanoi. We also had an office in Brazil and in Mexico City, and so we ended up with 10 offices across these geographies and we doubled to more than 418 employees. That was around time that I joined Temasek, I joined Temasek in September of 2010.

By the end of T2020, we had evolved into an organisation of 13 offices. We opened offices in New York City, in Washington D.C, and in San Francisco; and in Europe, London and Brussels. We did consolidate our offices in Vietnam into one: Hanoi. And so that was a big change that happened at that time. Today, we remain having 13 offices, we have actually evolved our Brazilian office into a joint venture, so that's one office less, but we opened up in Paris in 2024. And we have almost a thousand employees, we are at 959. So the organisation has grown very significantly in the last 20 years, from almost 200 employees to almost a thousand employees, so five times the number, as our portfolio has also grown.