I can also give you another version of how our portfolio has evolved,

this time from a geographical perspective.

Using the same T2010, 2020, 2030 periods…

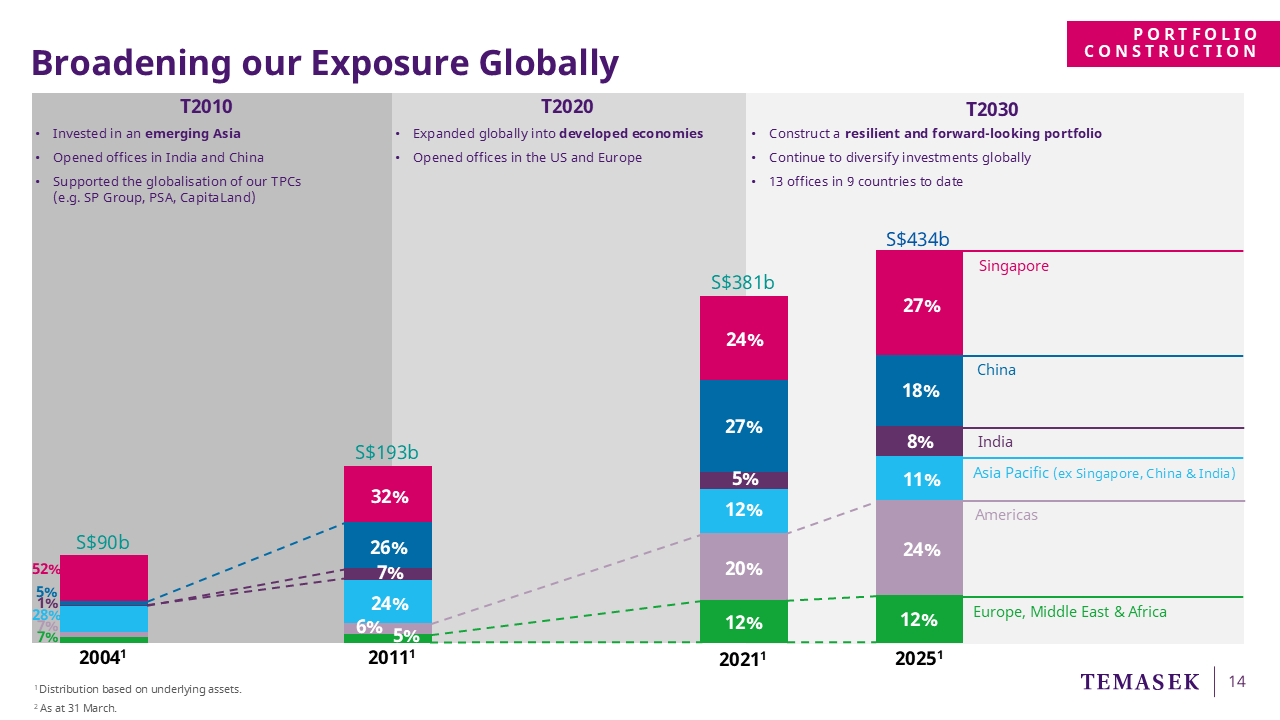

T2010

In the first decade, we invested in an emerging Asia

as it recovered from the Asian Financial Crisis.

We set up offices in emerging markets such as India and China,

to capture opportunities from the growth of the middle-income population and

local industrial champions.

So you can see our exposure to China and India (in dark blue and purple)

growing to 26% and 7% respectively,

and we were beneficiaries from the spike in China’s growth.

During that period, we also supported our TPCs in their globalisation plans,

which also added to the geographical diversification of our portfolio by underlying assets.

An example is PSA. Since corporatising in 1997, it has expanded to become a global cargo partner across more than 180 locations in 45 countries today.

We have shared a factsheet with you separately with more examples.

T2020

Under T2020, we extended beyond Asia, with the aim to become a global investment house by 2020.

After the Global Financial Crisis,

we saw an opportunity to invest in developed markets such as the US and Europe,

as they restructured to recover from the GFC.

So we began to deploy more capital to these regions.

We opened our first offices there in 2014.

Today, we have six offices across both continents.

You can see that our combined exposure to both continents (at the bottom in light purple and green)

has tripled from 11% in 2011, to 36% today.

In dollar terms, the exposure to these regions were approximately 21 billion dollars in 2011.

It has grown by about seven times to approximately 156 billion dollars today.

So, you can see that the geographical exposure of our portfolio today

is the result of our portfolio strategies and regional focus over the years.

T2030

Today, we have 13 offices in 9 countries.

And for T2030 and beyond, we will continue to sense the market,

and adjust our portfolio allocation towards regions with attractive investment opportunities.

I hope these two slides have given you a useful perspective

on our investment strategies over the years,

and how they have shaped our portfolio composition which you see today

– both by segment and by geography.

Now let me move on to share with you our outlook on each of the markets.