QUESTION: Dilhan, you made the point that you've obviously witnessed a significant upswing in US public markets and that's not really where you have significant exposure and that, longer term you're more focused on Asia, for example, where the growth will be. So I mean, would it be fair to say that irrespective of, in a way, where public markets will go and how they will perform, the longer term vision and promise of Asia sort of trumps those trends and market movements and therefore that vision also trumps where the total shareholder return may move potentially into more negative territory?

DILHAN PILLAY: I won't want to downplay the value of the portfolio we have in private investments in the US. So, if you look at the shift of our portfolio over the last, say, ten years. We started to invest in the US more significantly from 2014 when we opened up an office in New York. In 2016 we opened up in San Francisco as well and that actually underpinned our investments in core areas like technology, life sciences and so on.

That will continue to be the case, by the way. There will be significant allocation of capital every year to the US and to these areas that we see are focus areas for the future and in line with the six trends that we have identified. And so, if you look at a portfolio construction that gives you a return profile over the next 20 years, that will be a significant component.

Some of those companies will find their way into the US public markets, and we can possibly see an increase in US public market exposure as a result of that. Our private investments will not stay private for long. They might stay private for longer, as we have seen in the technology world, but you might find it's about there.

Now if you look at allocation of capital to the US versus the rest of the world, where do we invest in the rest of the world? So, a big part of our capital goes to China, to India and now we have a focus for South‑East Asia. So, in just relative terms, you will see more allocation towards Asia compared to, say, US and maybe even Europe.

So when you think about that we would only invest capital where we see risk‑adjusted return hurdles are met and so when we invest in emerging markets in a rising Asia, we have to bear in mind our cost of capital is higher and therefore the risks are higher, to some extent and so we have to be very focussed on investing in the right things, the right trends, the right opportunities and the right return framework.

So, I wouldn't do a broad brush because, like we said, we do it bottom up. There may be a year when we find the opportunities in US and Europe are so great that we want to allocate more capital there, and then over a five‑year, seven‑year period you will see that come out in portfolio value, whether private or public markets. It's based on where our companies are also exposed.

CHIA SONG HWEE: Let me add a few comments. We could also point to you that at certain periods, the emerging market or Asia outperformed the US or European markets. It's just when you start and when you end. One thing that you would want to consider also is the equity market, capital market in Asia is still very under-represented relative to the developed market. So, there's a lot of head room and the number of institution investors that are actually investing consistently in a market is still very minimum. So, to me, that represents opportunity, not a threat, actually.

JOHN VASKE: I was going to say, the way we operate is not ‑ it's a little bit agnostic to private versus public, it's where we can have a differentiated point of view and an ability to express our capital. But I would just echo what Dilhan said. We've deployed a fair amount of capital in establishing the US base, we've participated in some early stage stuff and some later stages and it's one of the benefits of getting in early is that you can continue to be a capital provider to that company along with the journey and one element of that journey may be to become public. When that becomes a public company, and we're a public securities owner, our point of view, given the history of being alongside management when they've chased that opportunity, just gives us sort of different insight, if you will.

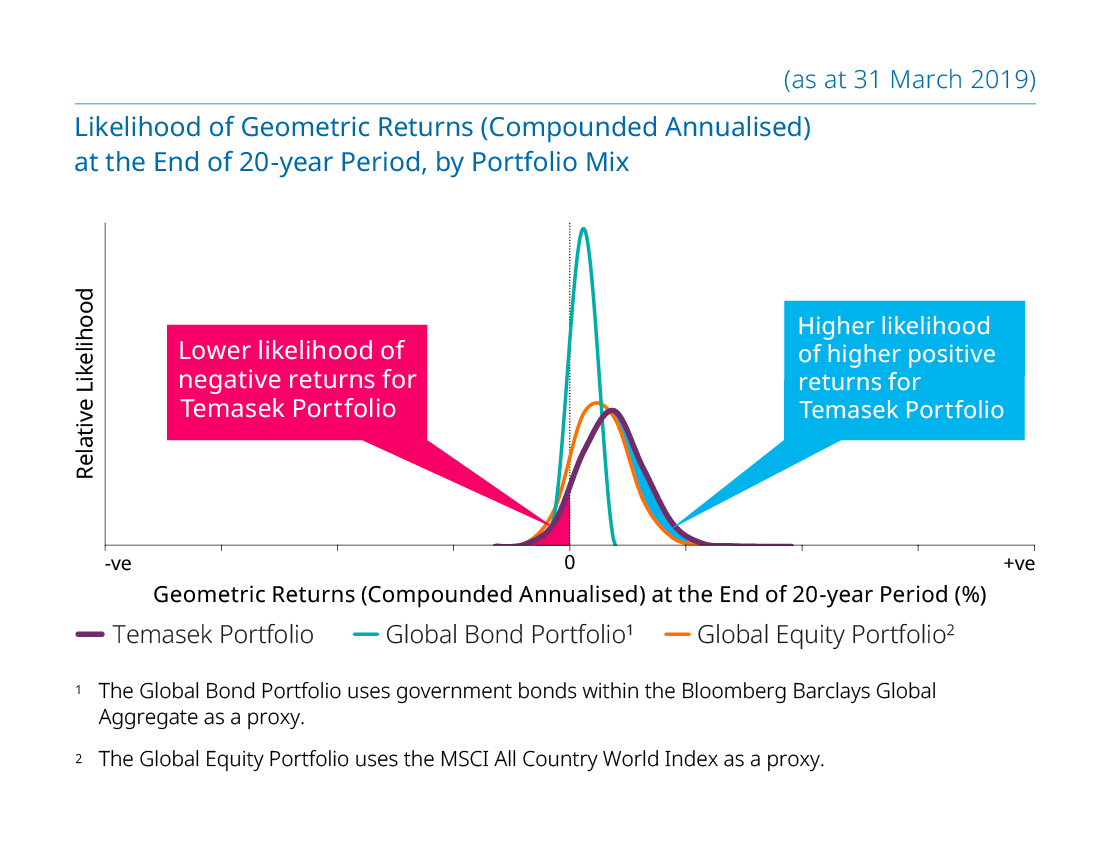

DILHAN PILLAY: I would like to add to what Song Hwee said, actually our returns in Asia have been actually, you know, very, very good over the years. And it gives us confidence that continuing investments in Asia is the right thing to do. If I look at the way our portfolio is being meaningfully constructed systematically going forward, you know, there's every confidence, in the absence of geopolitical events that nobody can foresee, the unknown unknowns of a very large magnitude, that the portfolio will perform in accordance with what we hope for it to be performing in 20 years, over a 20‑year period.