QUESTION: Unlisted assets position is now 48%, a very big increase from 42%. Intuitively, one would imagine that's a function of the fact that at March 31, listed markets were still heavily down and perhaps that is a distortion but I did want to ask you is that the case and has that turned back towards the previous equilibrium or has there been a conscious effort to put more into unlisted assets?

PNG CHIN YEE: I don't think there's been a significant change in the portfolio mix since the end of the year. Clearly markets have rebounded since March 31 which pretty much marked evaluations as a result of COVID. So that's, I guess, an indication to the positive.

From the liquidity perspective, we're still very liquid. As you know, when we were here last year, we talked about the fact that we wanted to de-risk in light of slowing economic conditions. Clearly, we didn't foresee COVID coming through, but we had actually de-risked significantly coming into this year.

In terms of our private assets, they have delivered stronger returns than our listed portfolio and they've outperformed and given as a liquidity premium that we expect to derive from being invested in the private space. So, you're right to say that this is all a function of the relative evaluations of our listed versus our private portfolios and I think with the recovery in the market you may say see some retracement of that 48% at this point in time.

Having said that, we do have at least half of our portfolio in the private space, mark to market because of the underlying exposures that they're in. The other half, which is not mark to market, we recognise at book value and recognise impairments on a year‑to‑year basis where we ‑ if and when we see deterioration in the portfolio. So, the marks on that book is actually quite fresh.

Out of the half which is not mark to market, two thirds of those are companies which you will be very familiar with, Mapletree, SingPower, PSA and Watson, some very high‑quality names. Only a small portion of that is in what we call earlier stage companies. They will comprise about sort of 5% of our overall portfolio. And within those, we've a pretty good track record of our private investments. So, some of the names that you're familiar with today, for example, Alibaba, Adyen or Celltrion, Meituan, these started out as private investments in our portfolio and we've seen very good realisation from these investments over time. So, I hope that addresses most of your questions.

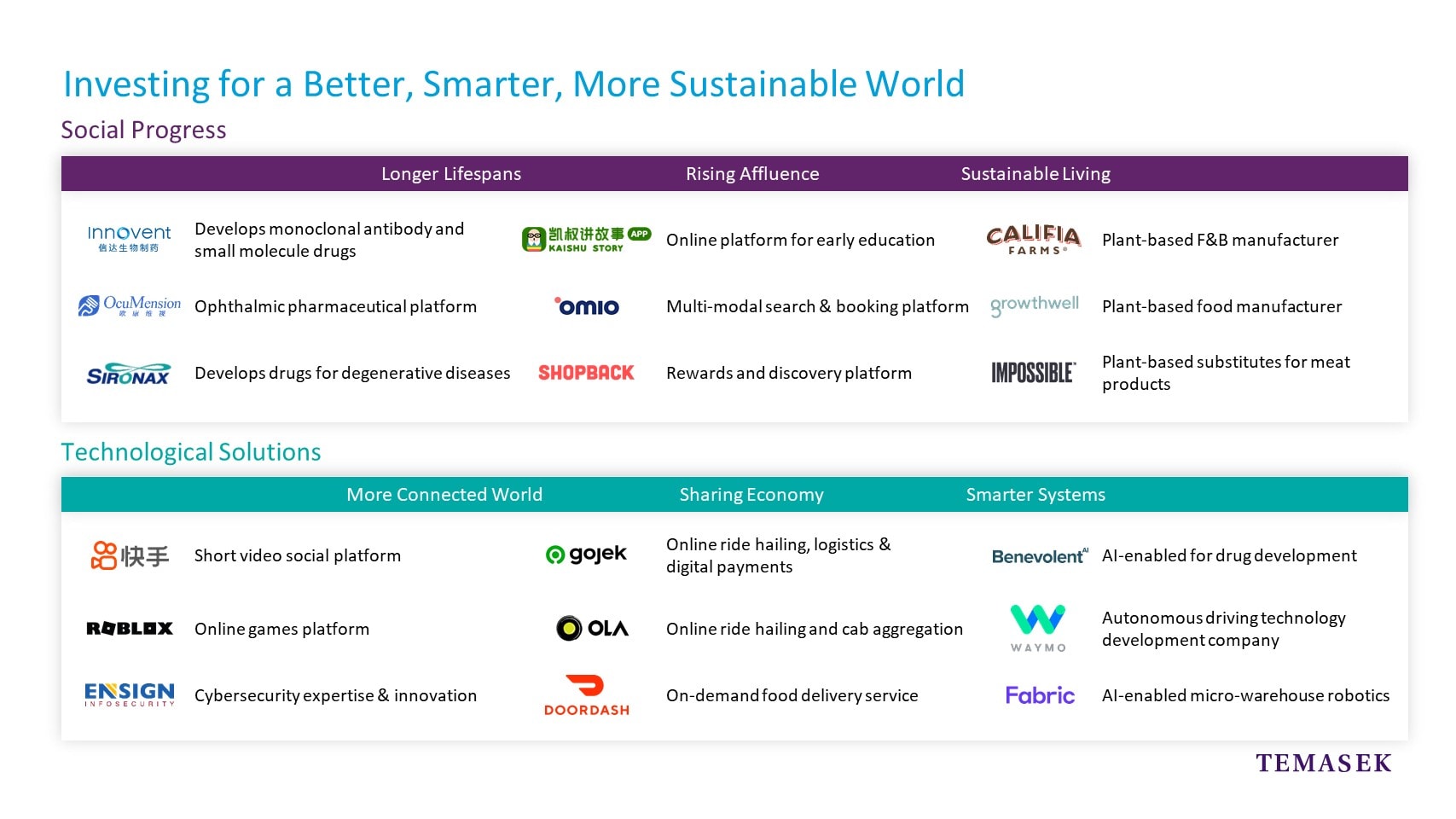

YEOH KEAT CHUAN: I just wanted to add, Chin Yee, that if you look at 2010, 23% of our portfolio was unlisted assets, so that has grown very steadily over the years and the other reason is also it's very much in line with the structural trends we're seeing. Spaces like longer lifespans, more connected worlds, smarter systems – that's where the opportunities lie.

PNG CHIN YEE: Our ability to invest in both the private and public space gives us a competitive advantage, relative to those whose mandates are actually more constrained because, for example, one of the things we've liked is around payments and we've invested in the public space with Visa, Mastercard, PayPal, etc, but we've also invested in the private space with Adyen and being able to do that across the capital structure actually gives us a lot of flexibility in terms of how we pursue a theme.