Hello and thank you for coming to the media briefing for Temasek Review 2026.

We’re not simply in a VUCA world, we are in a polycrisis world.

This is not new to us. As a long-term investor seeking to deliver sustainable returns, we have had to navigate volatility and uncertainty over the years. But the environment we are in today is the most complex that we have seen in five decades.

This brings us back to the 1970s — the decade in which Temasek was founded, when the world had several wars, fractures in society, runaway inflation, and markets that were volatile.

What is unprecedented is the convergence of geopolitical tensions, technology transformation, energy security concerns exacerbated by recent events in the Middle East. A demanding environment where fiscal space is constrained by rising costs, inflation, and interest rates which are a drag on growth and returns.

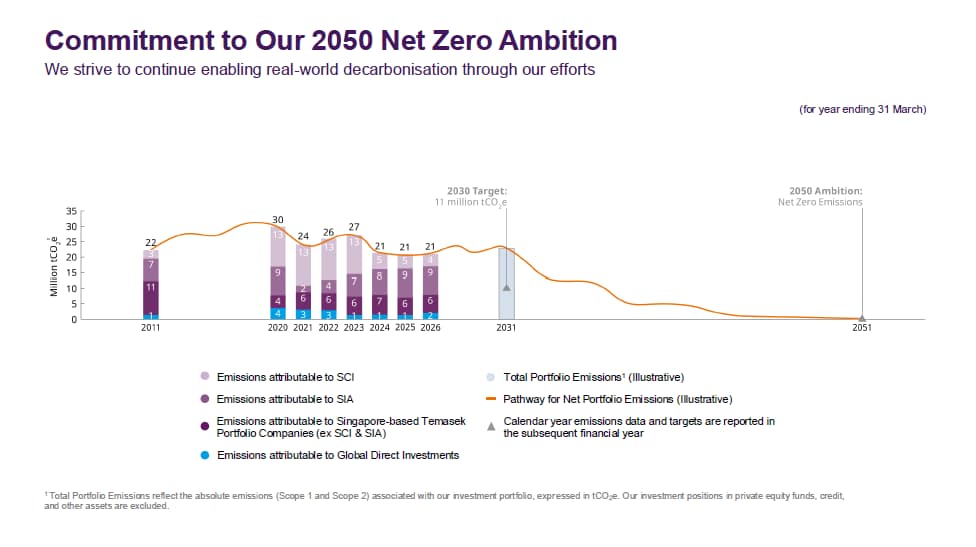

Meanwhile, generative AI is reshaping business models and the nature of work itself, bringing both opportunities and risks. Climate transition is under pressure amidst rising power demand.

Taken together, this is one of the most challenging environments we have had to navigate as an investor seeking good sustainable returns over the long term.

From Complexity to Clarity

We are focused on complexity to clarity. For a long-term investor like us, it is very important to be clear-minded about how we need to operate to achieve the returns that we want.

We have to live with the world as it is, not as we wish it would be, as Mr Lee Kuan Yew once said. And that is why you will hear my colleagues talk about how we are navigating this complexity to deliver clarity.

What does this entail?

We have been consciously making important shifts to our portfolio and investment strategies over the past few years. And it is starting to bear fruit, as you will see from the results of the past two financial years.

Do Well: Performance and Investment Stance

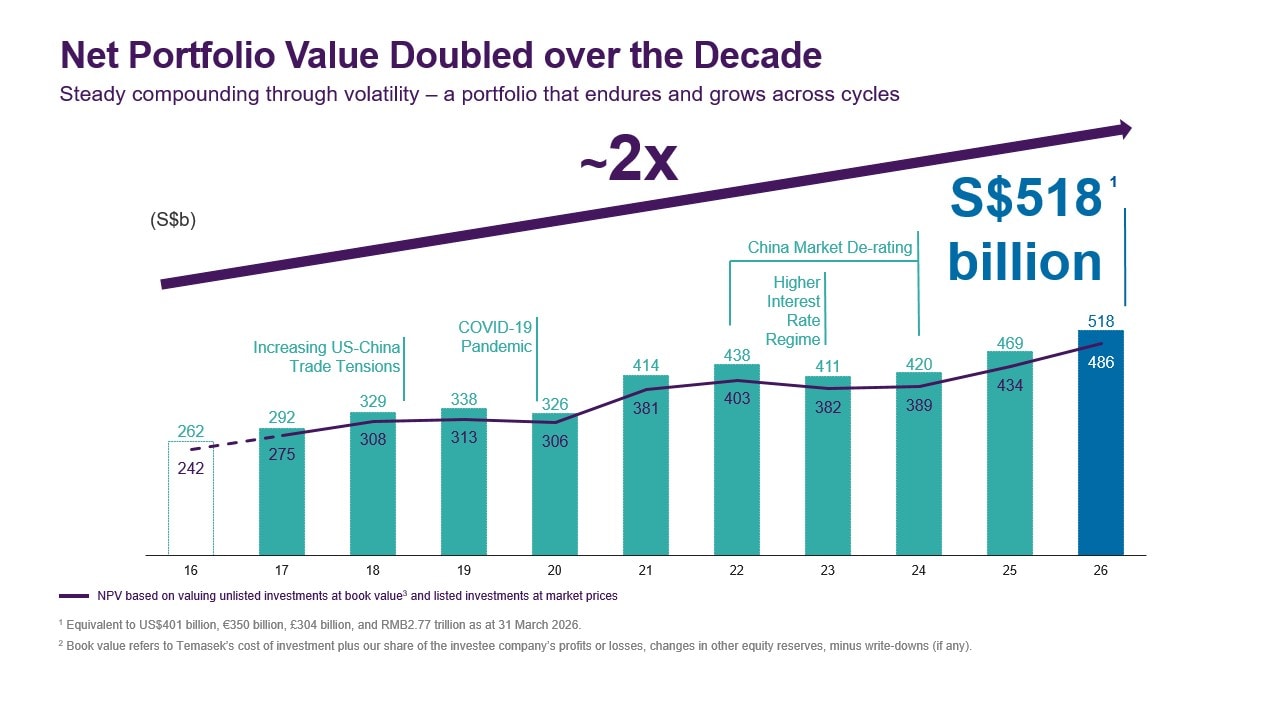

Since we started making these shifts, we have added about S$100 billion in portfolio value. That is a good outcome for us and hopefully represents a positive trajectory forward.

What have these shifts looked like?

Sharpening discipline across investments and divestments, driving value creation across our portfolio companies, strengthening our public markets capabilities.

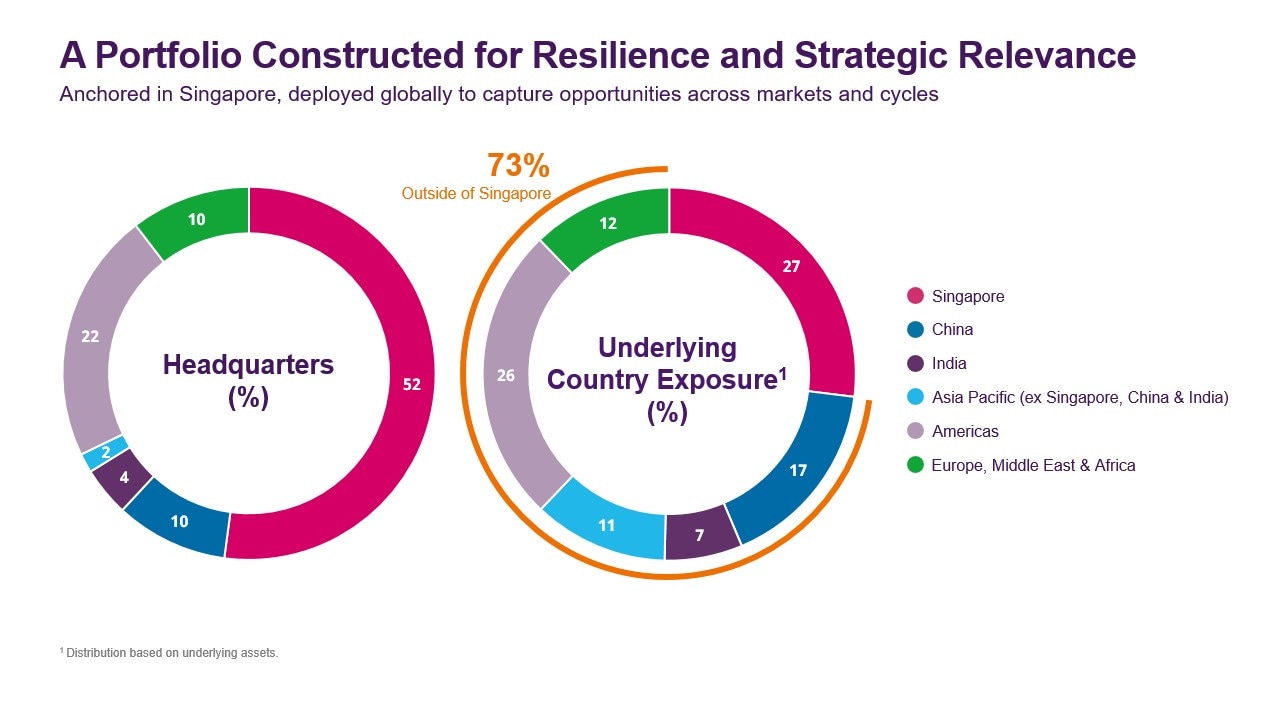

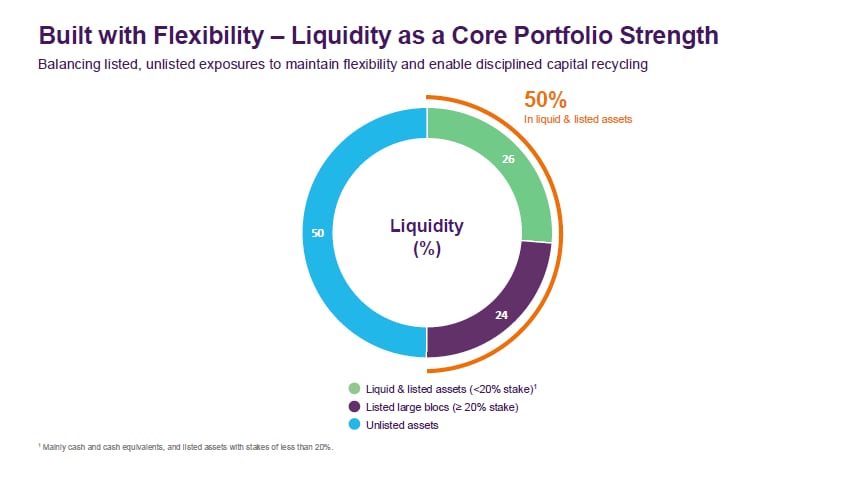

But for performance to remain resilient going forward, the most important factor is to build a quality portfolio, one that can bounce back from shocks. And we should expect these shocks to continue. A good investment environment matters too, but that is something we cannot control.

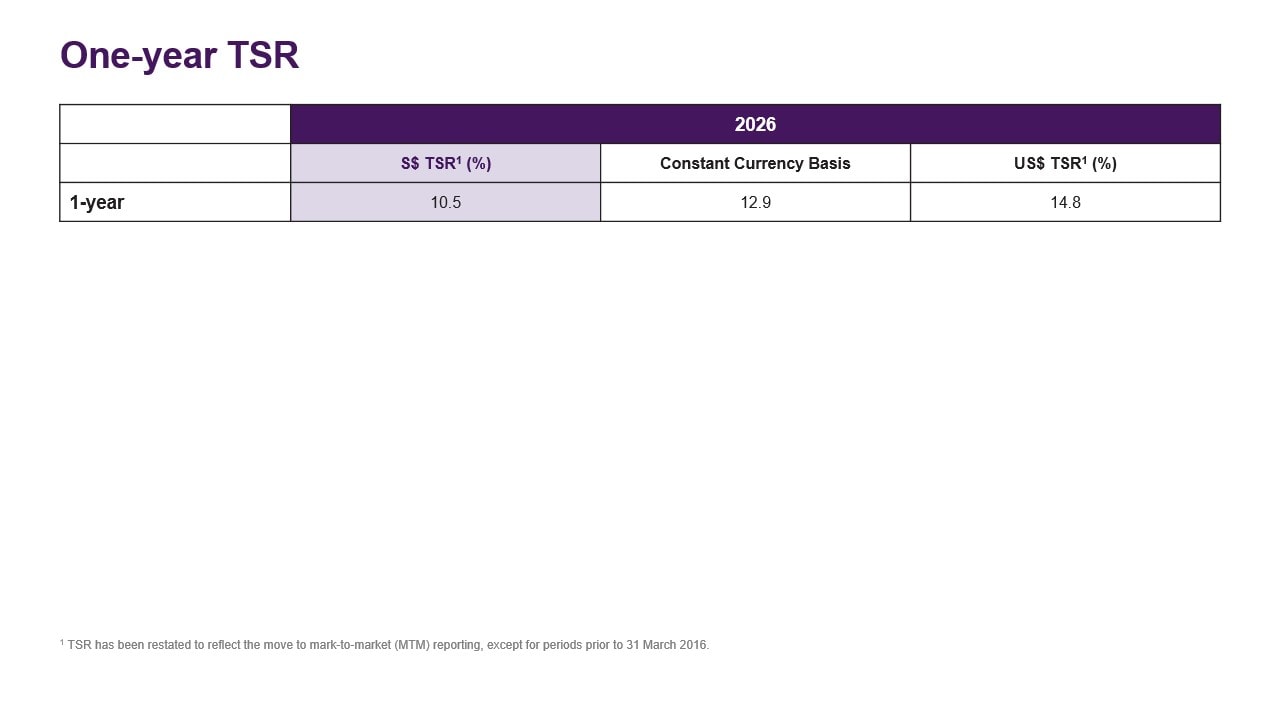

Year-to-year performance may not be the most natural measurement for an institution like ours, which is geared towards good sustainable returns over the long term. The real measurement of success is the longer-term returns of 10 and especially, 20 years. It is aligned with our mandate.

This year, we have fully transitioned our financial reporting to mark-to-market.

We started this four years ago.

Only about 25% of our portfolio needed to be aligned; the rest was already marked-to-market. In the longer 10-year TSR for example, you will see that there is no significant difference between mark-to-market or prior basis TSR.