This article grossly misrepresents Temasek’s investment stance on Europe by neglecting material facts that were shared during our Temasek Review media briefing, with FT and other international media.

Our Chief Investment Officer, Rohit Sipahimalani explicitly stated during the briefing that we have a strong presence in Europe and it is amongst the key markets that will be the “biggest recipients of our capital.” This is contrary to the assertion that “rising trade tensions from US President Donald Trump’s tariffs have made Temasek fearful that the European companies it has previously targeted for investment will be among the worst affected.”

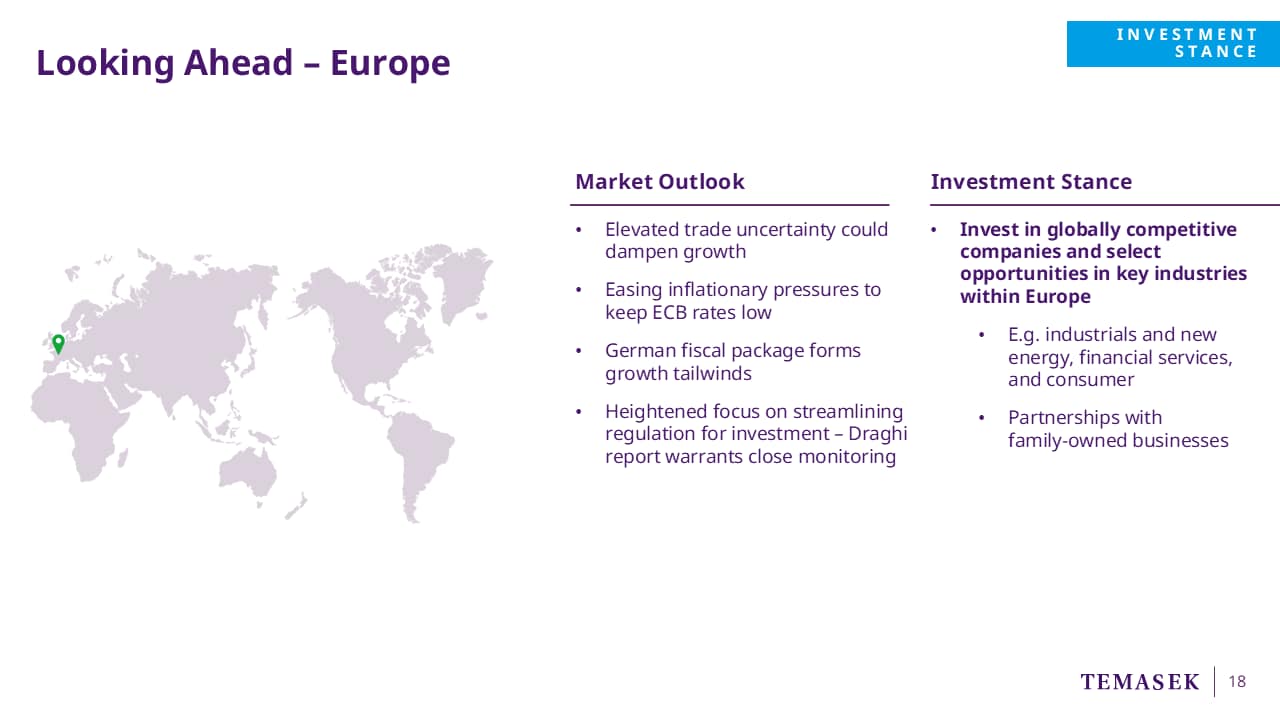

Rohit added that Temasek’s plans to invest S$20 to S$25 billion in Europe over five years remain on track, and we continue to see opportunities in Europe. He noted that “we will invest in high-quality businesses that are going to be more resistant to the geopolitical shocks we are seeing today.” These include family-run businesses with strong franchises and deep engineering or technical leadership in sectors such as industrial and new energy, financial services, and consumer goods.

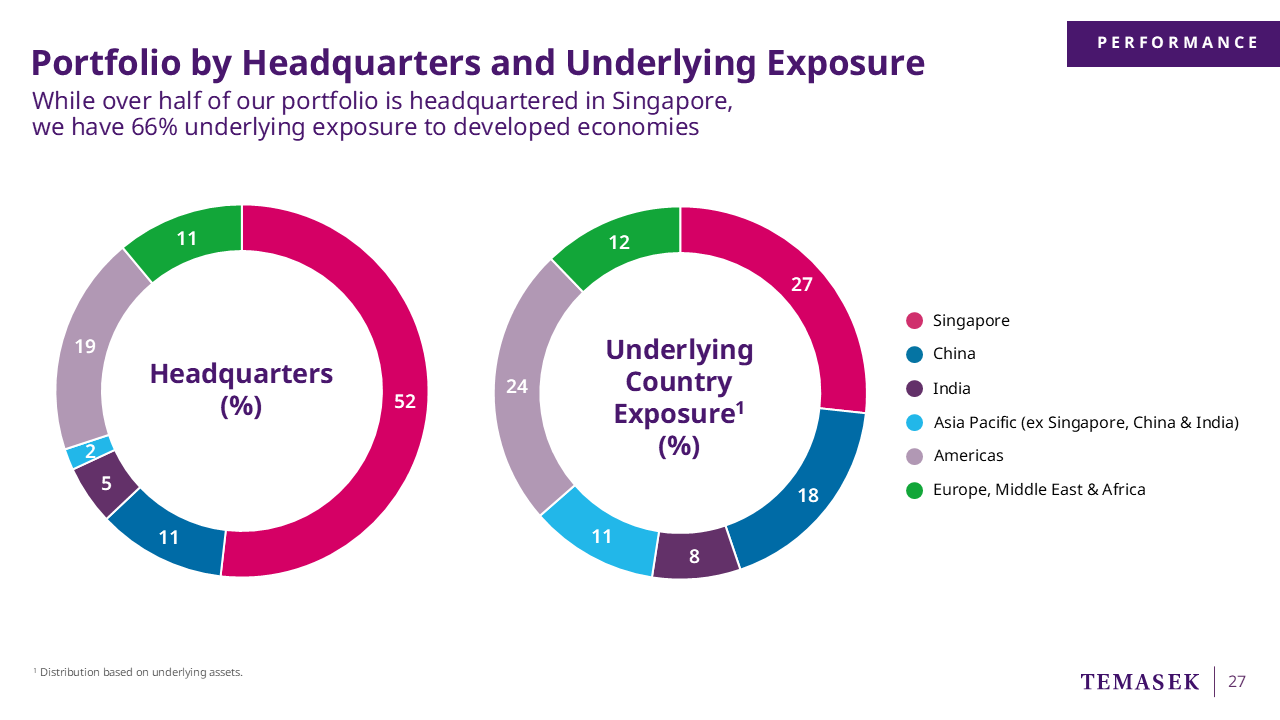

Over the past year, the absolute value of our underlying exposure to EMEA has increased and our portfolio exposure in EMEA by headquarters was up by 1% (over S$4 billion). However, the article ignored these facts and only highlighted in isolation our underlying exposure is down a percentage point from a year ago.

Europe has been the second-largest recipient of our capital since 2022 and will remain so based on our capital allocation for our portfolio construction. We continue to actively source opportunities and approve sizable transactions notwithstanding the uncertainties arising from tariffs.

Our recent investments include Neoen (renewable energy), Keyword Studios (video game technology services), VFS Global (visa processing), Atlantica Sustainable Infrastructure, and SRG (financial services).

The article conflates our views on the macroeconomic outlook with our investment activities in the region.

During the media briefing, our Joint Head of Corporate Strategy, Lim Ming Pey’s presentation noted that while there is a sense of elevated trade uncertainty that could impact the growth trajectory of the region, our portfolio in Europe remains resilient.

The media presentation is available here and the exchange with FT and other international media on Europe at the media briefing is reproduced below.

Chia Song Hwee

Deputy CEO, Temasek