The following is the speaker notes that accompanied the presentation deck for Temasek Review 2026. The text should be read in conjunction with the slides shown in this document.

Please note that:

- All data presented are for our financial year ended 31 March 2026

- All currencies quoted are in Singapore dollars unless otherwise stated

Thank you for joining us today.

You have just heard from our CEO, Dilhan, sharing about the complexities of the broader global environment that we are operating in.

What I will do now is to bring that into sharper focus from Temasek’s perspective.

The theme for this year’s Temasek Review is “From Complexity to Clarity”.

Our job as a global investor is not to predict volatility, but to build a resilient portfolio that can navigate and perform through it.

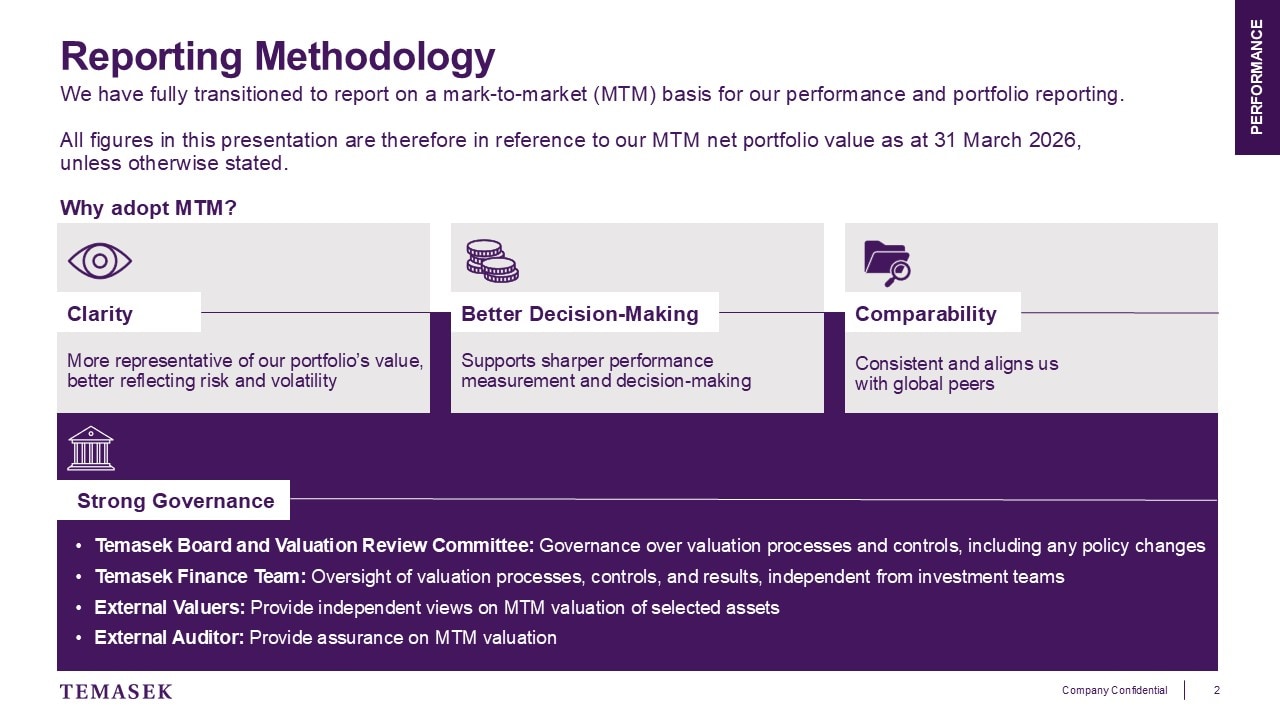

Before that, let me run you through the change in our reporting methodology that is taking effect from this year on.

We have fully transitioned to report on a mark-to-market basis, or MTM for short.

Why does this matter?

It provides a clearer and more consistent view of our portfolio value, performance, and risk across asset types and holding structures. It also aligns our reporting with global best practices, particularly when looking across time periods and against our peers.

Importantly, to ensure that our valuation is robust, we have embedded a strong governance structure to match greater transparency with rigour, discipline, and accountability.

This is not a fundamental change to our reporting approach.

About three-quarters of our portfolio has already been marked-to-market, and since 2022, we have been disclosing the MTM value uplift of our portfolio. From this year on, we are simply extending this approach to the remainder of our portfolio.

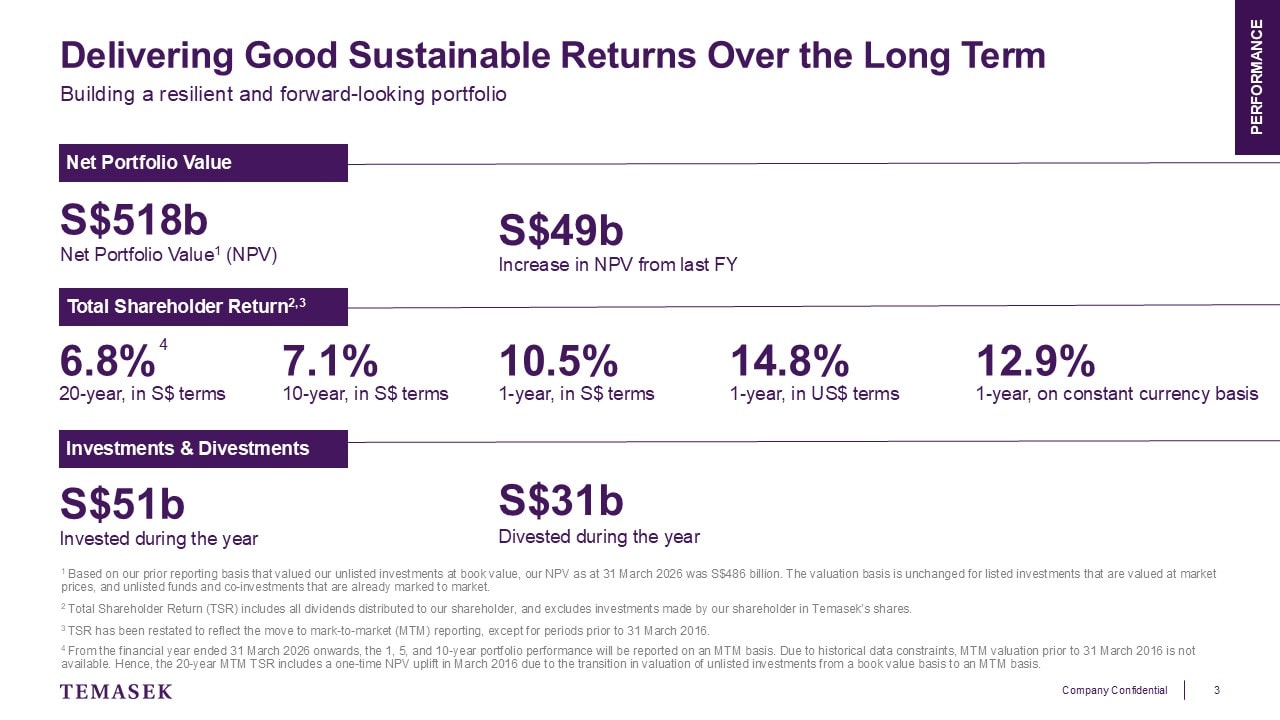

With that, let me turn to our headline numbers for the year.

Despite a complex environment, we continue to deliver resilient returns over the long term.

For the financial year ending 31 March 2026, our Net Portfolio Value stood at 518 billion Singapore dollars, an increase of 49 billion dollars from the previous financial year.

Our 20- and 10-year TSR were 6.8% and 7.1% respectively. This demonstrates the resilience of our portfolio over the long term and its ability to perform through market cycles.

Our 1-year TSR was 10.5% in SGD terms and 14.8% in USD terms, driven largely by the strong performance of our listed Singapore-based Temasek Portfolio Companies and realised gains from key divestments.

As Dilhan mentioned in the video earlier, foreign exchange rates have been volatile over the past year. Hence, reporting on a constant currency basis provides a clearer view of underlying performance. On that basis, our 1-year TSR was 12.9%, or about 2 percentage points higher.

Throughout the last financial year, we remained active and disciplined in our capital deployment. We invested 51 billion dollars and divested 31 billion dollars, recycling our capital to capture new and emerging opportunities.

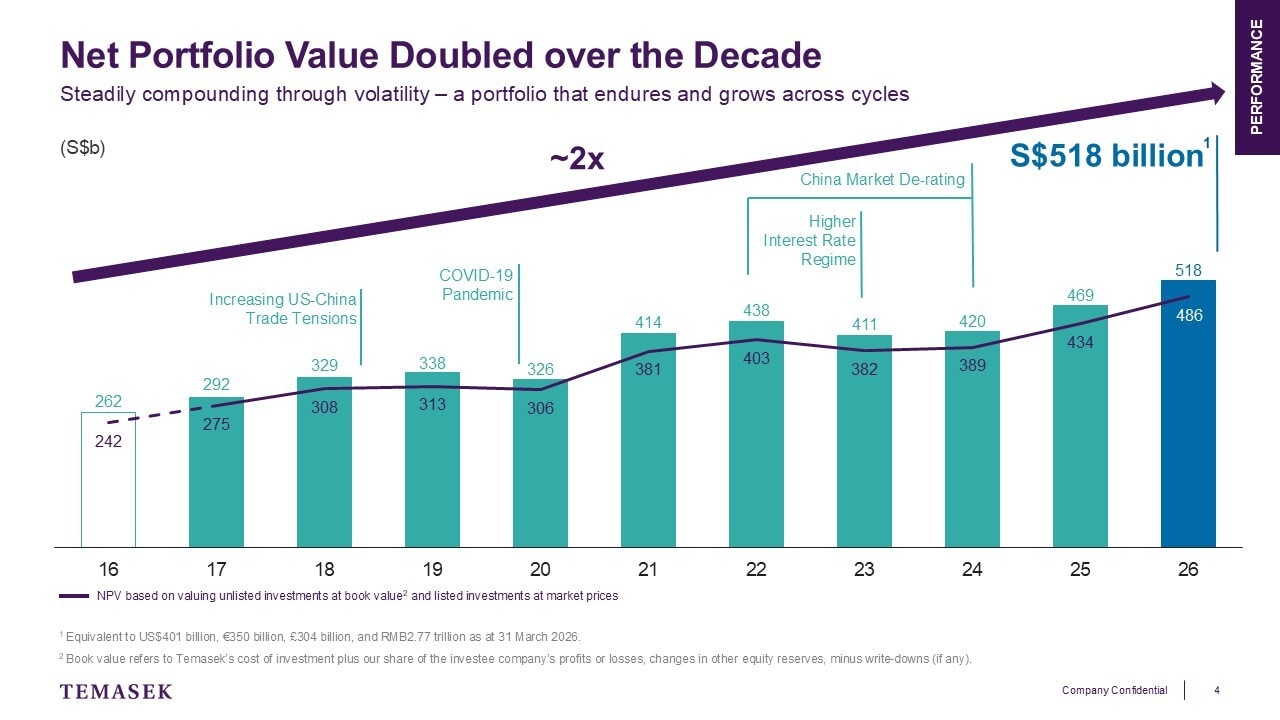

Let me put this year's results into a longer-term perspective.

Over the past decade, our net portfolio value has almost doubled to 518 billion Singapore dollars.

This growth was achieved despite multiple periods of market stress and economic disruption, as well as heightened geopolitical tensions.

The resilience you see in this chart did not happen by chance. It reflects the strength of our underlying assets, how we manage liquidity, and the discipline with which we deploy and recycle capital.

Let me now walk you through the key building blocks of our portfolio.

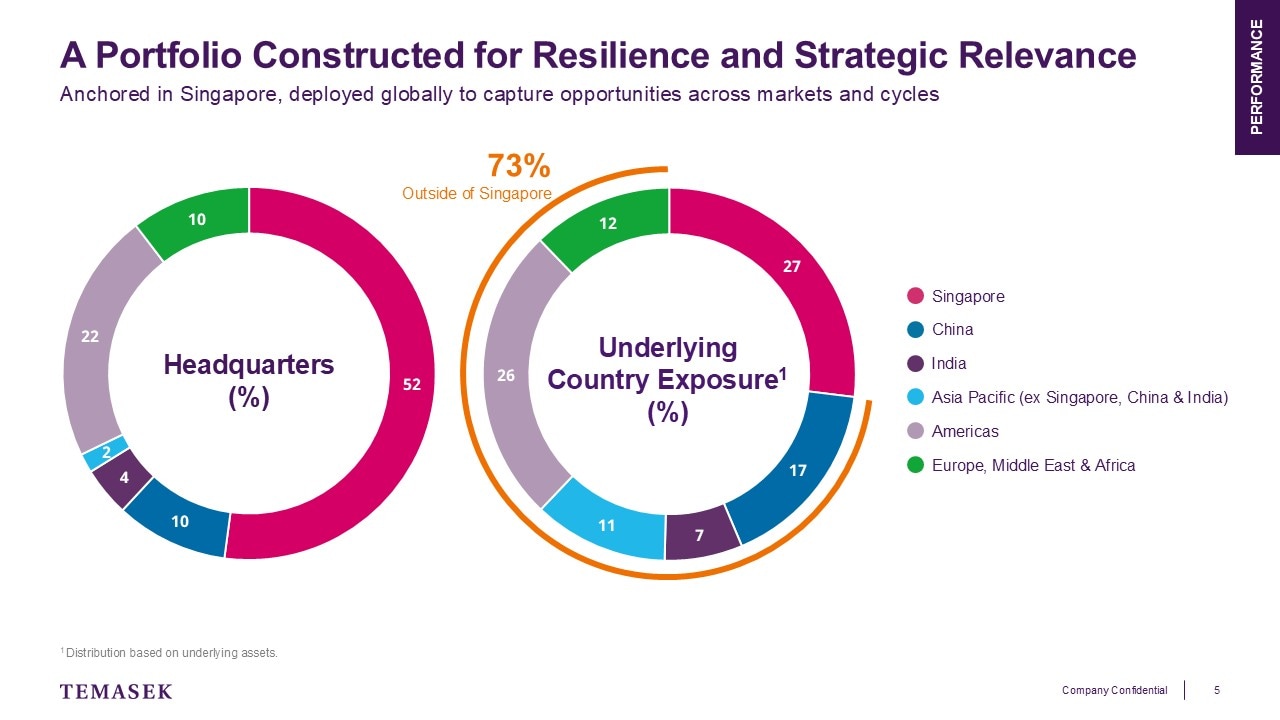

Starting with where we deploy our capital.

Our portfolio today is anchored in Singapore, but globally deployed.

You would have heard from Dilhan that our portfolio is structurally different from global market indices which have minimal exposure to Singapore, or from a local index like STI, as almost three-quarters of our underlying exposure is outside of Singapore.

Our portfolio is constructed around our key priorities of long-term portfolio resilience, strategic relevance, and disciplined deployment to capture opportunities aligned with our focus sectors across geographies.

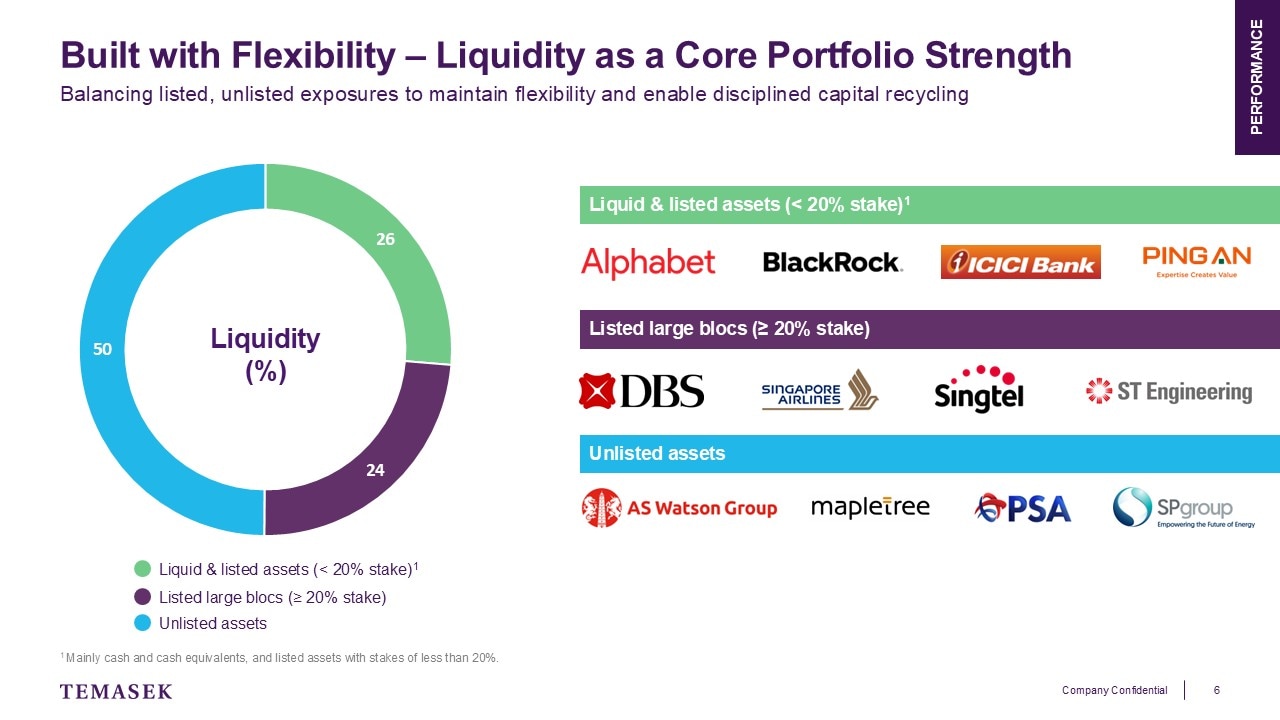

Geography is but one dimension of resilience. Another is maintaining the flexibility to respond when conditions change.

In today’s environment, capital flexibility is key.

About a quarter of our portfolio is in liquid and listed assets. This gives us the flexibility to pivot, rebalance, and respond quickly as opportunities and risks evolve.

At the same time, our unlisted investments continue to be a meaningful source of long-term value creation and cash generation for us.

On the right side of this slide, you will see some examples of our investments in these spaces.

Beyond geography and liquidity, resilience is also shaped by how we structure the portfolio itself.

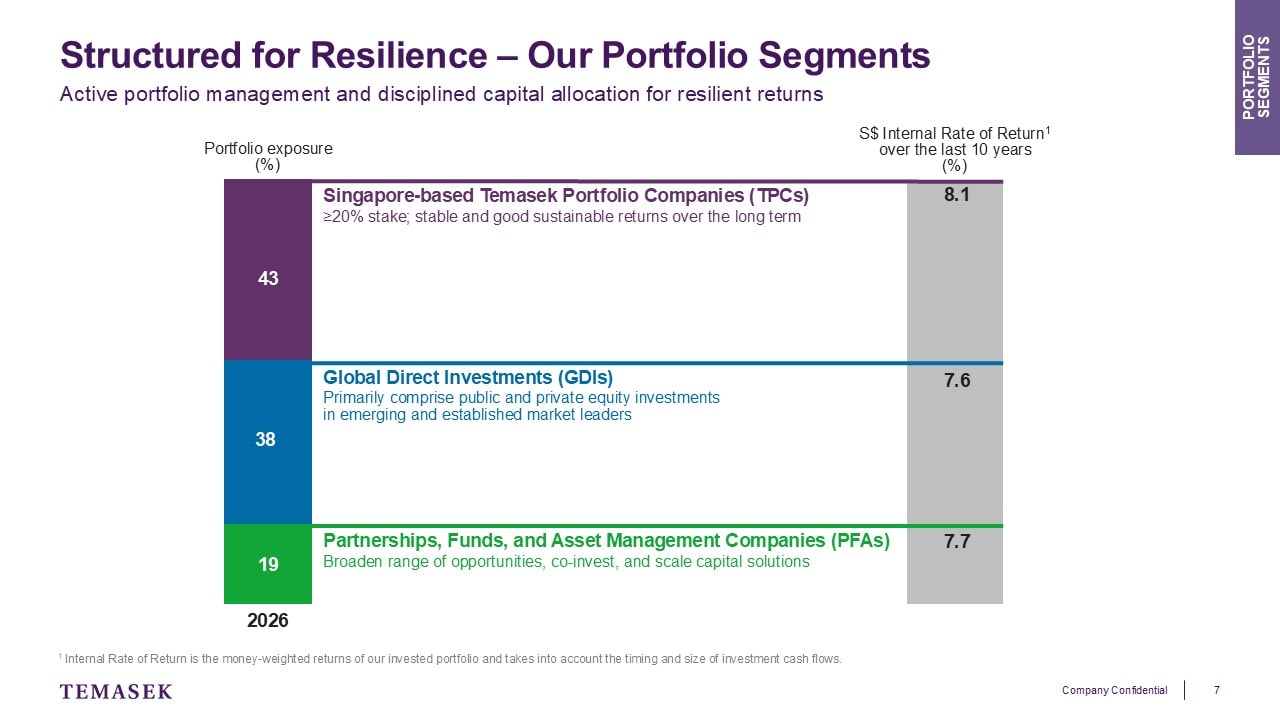

Over time, our portfolio has evolved into three segments, each serving a distinct role.

Our TPCs make up 43%. They are the stalwarts of our portfolio, and provide stable and good sustainable returns over the long term.

Our GDIs stand at 38%. They primarily comprise investments in emerging and established market leaders across focus sectors and markets.

Our PFAs make up the remaining 19%. They help broaden our access to opportunities, scale our capital in both public and private markets, and add differentiated return streams.

Together, these segments form three complementary engines of long-term returns.

Each has delivered resilient performance over the past decade, with 10-year IRRs ranging between 7.6% and 8.1%.

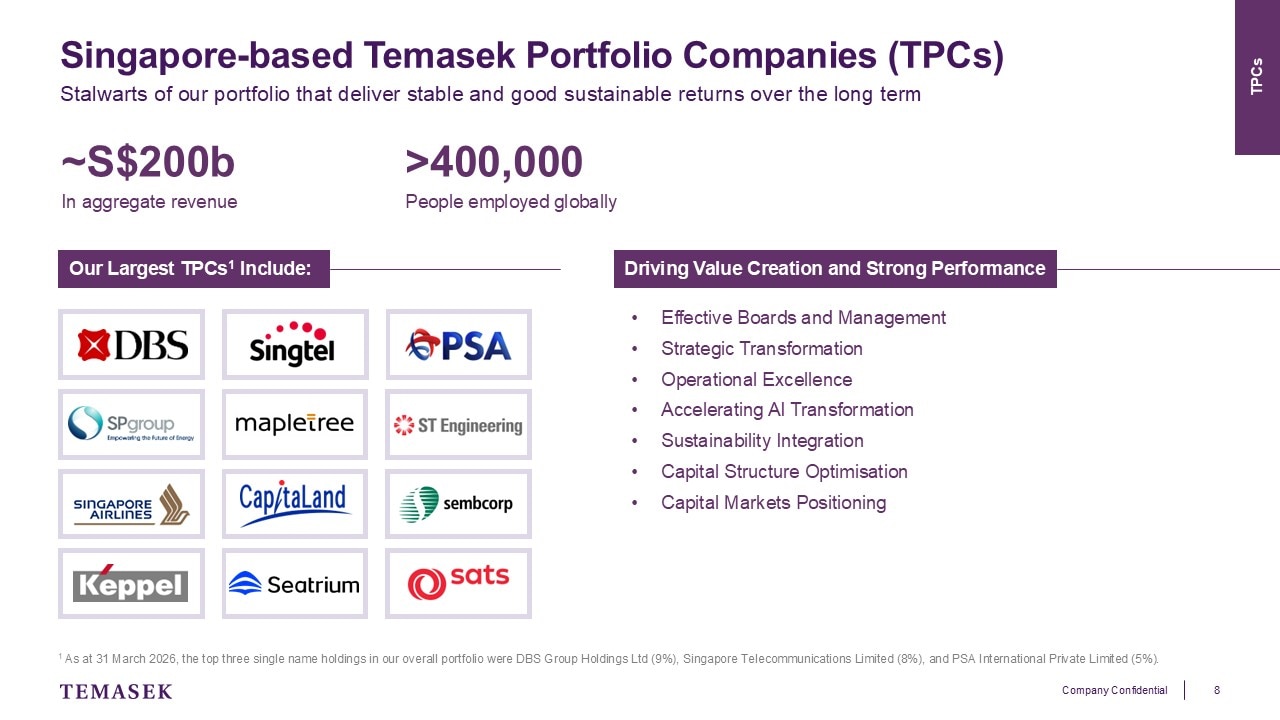

Let me now walk you through each of these segments, starting with our TPCs.

These remain the core foundation of our portfolio and are key to our portfolio resilience. Many of them are household names that you are familiar with.

Collectively, our TPCs generate about 200 billion dollars in aggregate revenue and employ over 400 thousand employees globally.

Beyond the numbers, we actively engage our TPCs to drive value creation and position them for future growth.

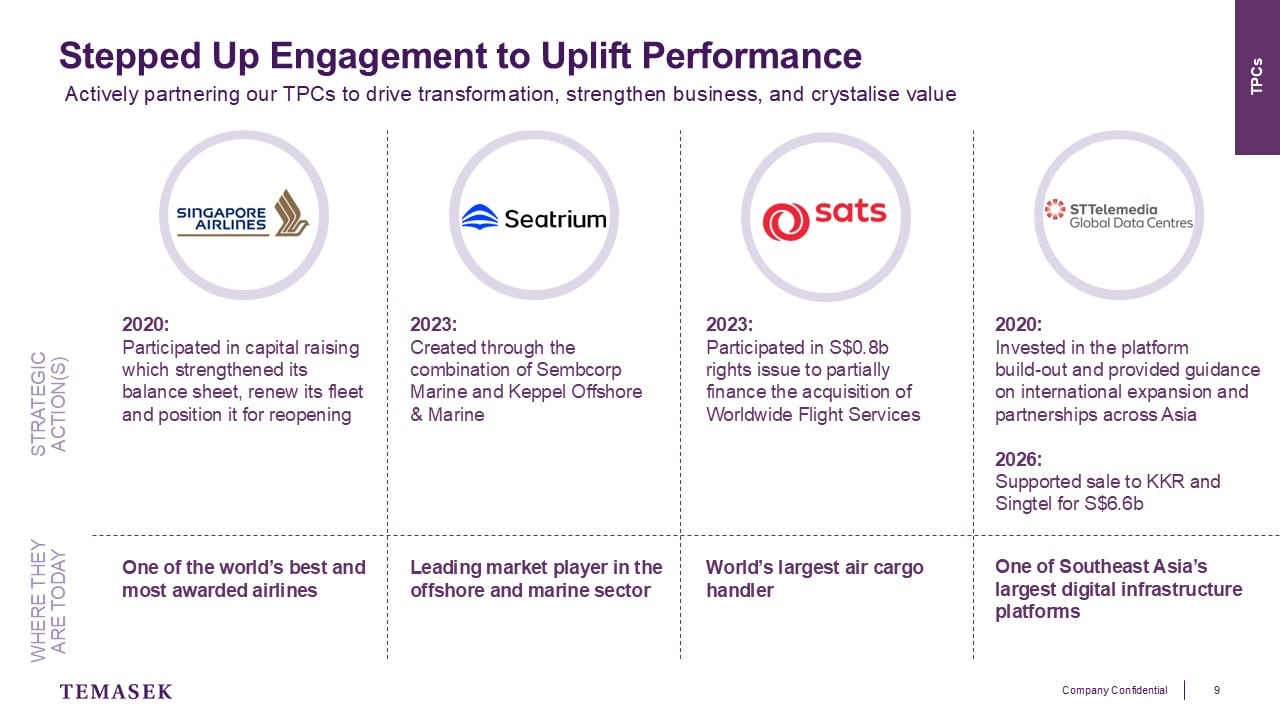

We are an active owner of our TPCs, and this comes through clearly in how we have been steadily partnering with them over the years to unlock value.

You can see various examples in the slide here, but one more recent one is ST Telemedia. In 2020, we invested in the build-out of STT GDC’s data centre platform, provided guidance on expansion, and facilitated introductions that enabled their development of partnerships across Asia.

Fast forward to earlier this year, the business was sold to KKR and Singtel for 6.6 billion dollars.

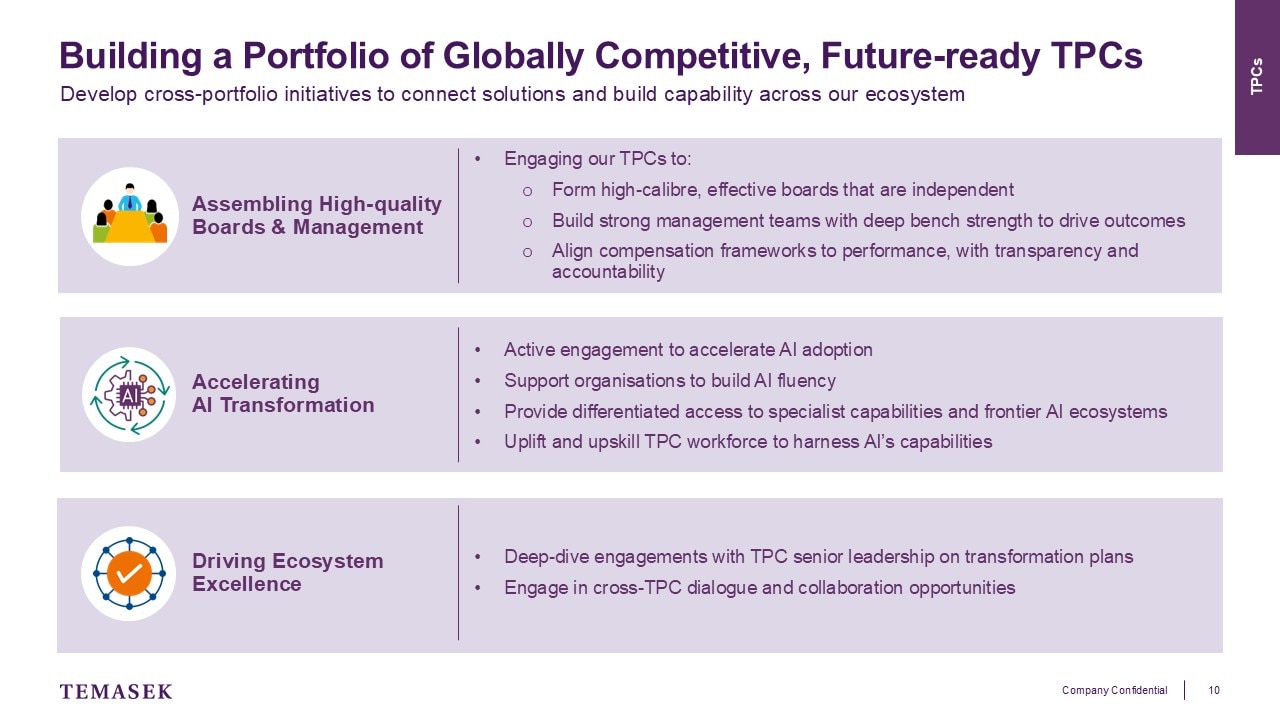

Looking ahead, our focus is on ensuring that our TPCs remain globally competitive and future ready.

We see three priorities.

First, continuing to strengthen leadership, governance, and organisational capability. Strong boards and management teams remain the foundation for long-term performance and resilience.

Second, accelerating AI transformation across our portfolio. We actively partner our TPCs to harness the use of AI, providing them with differentiated access to specialist capabilities and frontier AI ecosystems. We also work with them to uplift and upskill their workforce in leveraging the multifaceted capabilities of AI.

Third, deepening collaboration across our ecosystem. By connecting our portfolio companies with our broader ecosystem, we can accelerate learning, capability-building, and innovation at scale.

Ultimately, our objective is not simply to preserve today's champions, but to help build the next generation of globally competitive Singapore-rooted companies.

Let me now turn to the next segment of our portfolio – our GDIs.

This is where we deploy capital globally across sectors, markets, and stages of growth.

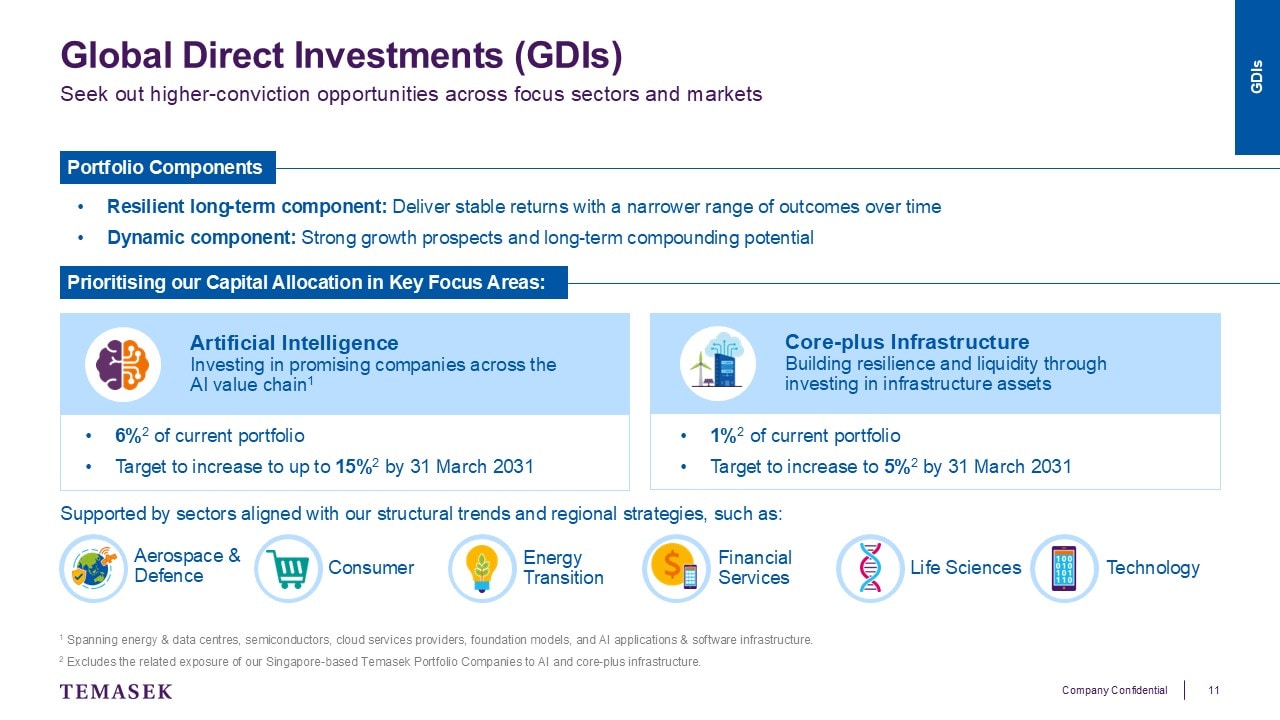

Within GDIs, we maintain a balance between two components:

- First, a resilient long-term component comprising high-quality businesses that can deliver stable returns across market cycles.

- Second, a dynamic component made up of companies and opportunities with strong growth and long-term compounding potential.

Looking ahead, we seek to increase our exposure into compelling opportunities where we see enduring structural tailwinds.

This includes AI, where we target to increase exposure from 6% today, to up to 15% by 2031, as well as Core-plus Infrastructure, where electrification, data centre growth, and energy transition investments are creating attractive long-term opportunities.

We will also focus on opportunities in selective sectors aligned with our structural trends and regional strategies.

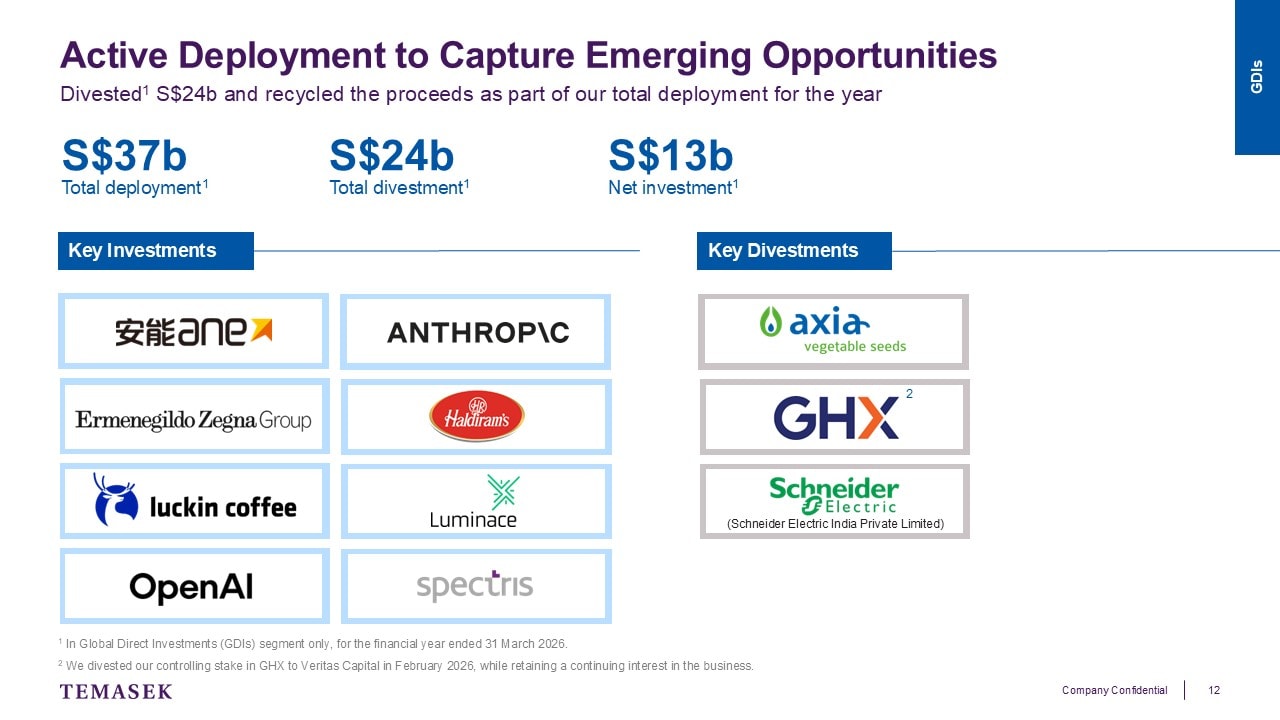

Let me show you how this translated into investment activity over the past year.

Within the GDI segment, we invested 37 billion dollars and divested 24 billion dollars, resulting in a net investment of 13 billion dollars.

Some of our key investments are names that you may be familiar with, such as Anthropic, OpenAI, and Luckin Coffee.

We also completed a number of divestments during the year as investments matured and delivered in line with our investment theses.

What this illustrates is our continued discipline in capital allocation – realising value where appropriate, and redeploying proceeds into opportunities where we see stronger future potential.

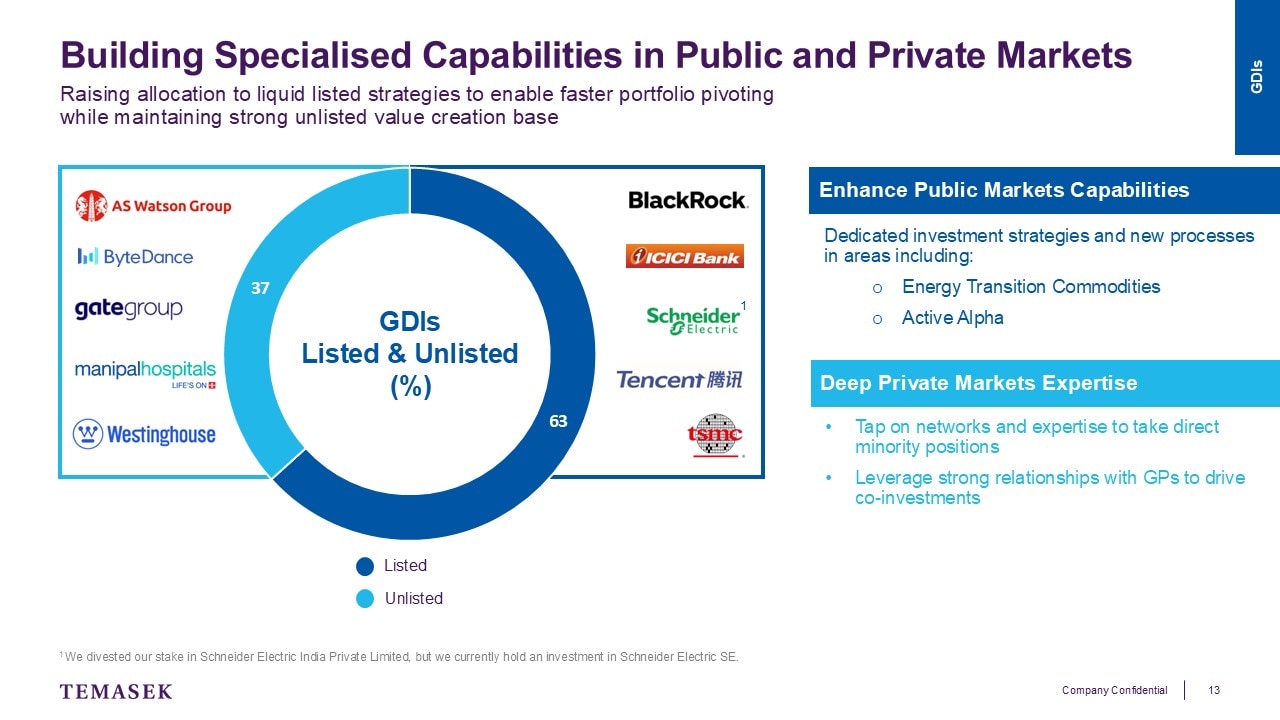

As a global investor, we invest across the capital structure.

Today, about two-thirds of our GDI portfolio is listed. One-third is unlisted.

In a more uncertain and rapidly changing environment, we have been increasing our allocation to listed investments.

We have also strengthened our public market capabilities in areas, including Energy Transition Commodities to focus on materials essential to enable the global energy transition; and Active Alpha, to focus on scaled positions in developed markets.

Importantly, this is not a shift away from private markets.

We continue to leverage our long-established strengths in private investing – tapping on our deep expertise to take direct minority positions through well-established networks; and seeking co-investments opportunities with trusted GPs.

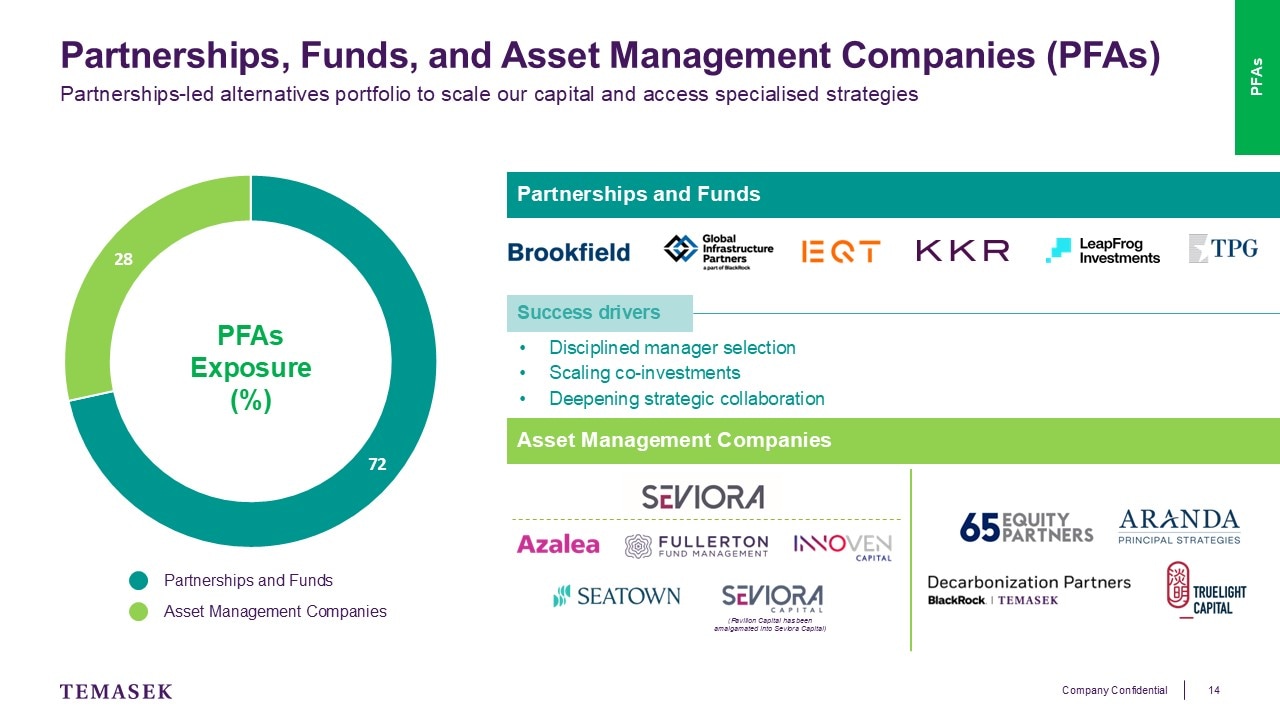

The third segment of our portfolio is our PFAs.

They broaden our access to opportunities, expertise, and capital solutions that would be challenging to replicate through direct investments alone.

Today, almost three-quarters of this segment is invested through Partnerships and Funds. This is where we back differentiated managers with strong deployment and operational capabilities, scale co-investment opportunities with our GP partners, and deepen strategic collaborations with our key fund managers.

The remaining is deployed to Asset Management Companies, or AMCs for short. They include those managed by our main Asset Management Platform, Seviora Holdings, as well as others such as Aranda and Decarbonization Partners.

Beyond providing access, we are also actively building scale and capability within the PFA segment.

Over the past year, we continued strengthening our alternatives platform and broadening our capital solutions capabilities. For example, the amalgamation of Pavilion Capital into Seviora Capital strengthened our private equity capabilities and expanded the scale of the broader Seviora platform.

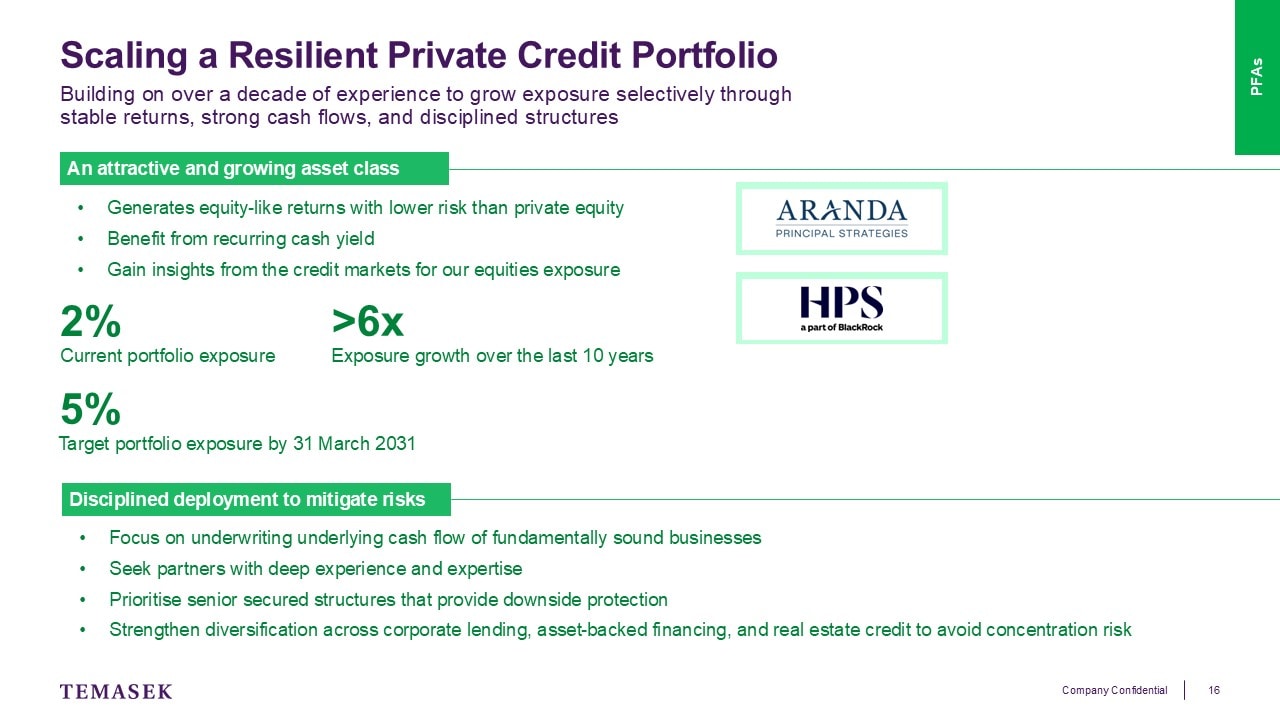

Aranda, our private credit platform, has also expanded from its initial 10 billion dollars portfolio to 13 billion today, generating over 1 billion in annual recurring income.

On this, let me briefly touch on private credit.

Private credit is an area where we have been building capabilities for more than a decade.

It remains an attractive asset class to us, because it can offer equity-like returns at lower risk compared to private equity, while providing stable, recurring cash yield that contribute to portfolio resilience.

Our exposure to the space has grown more than sixfold over the last decade. It currently stands at about 2% of our total portfolio, with a target of around 5% over the next 5 years.

Our approach to this asset class remains selective and disciplined. We focus on senior secured structures, strong underwriting through experienced partners with proven origination, and a well-diversified lending book to avoid concentration risk.

Now you have heard about the three segments of our portfolio, let me move on to sustainability.

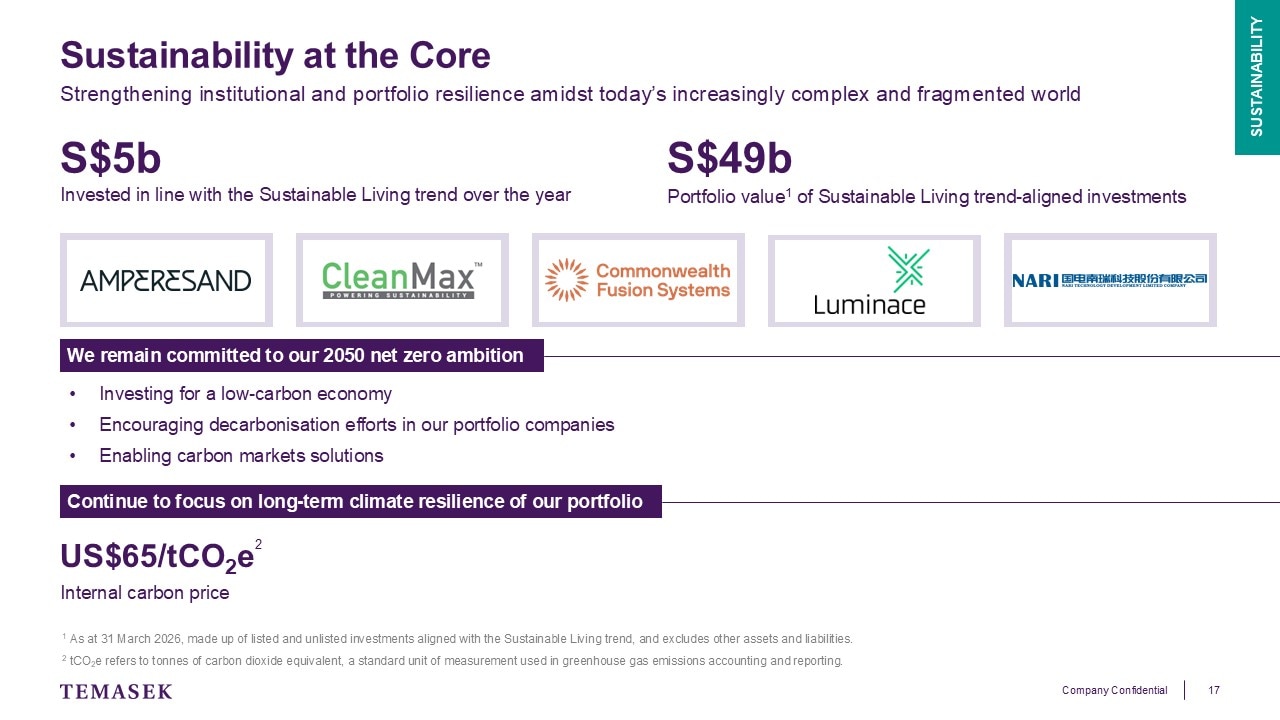

As a long-term investor, we see sustainability as a key driver of institutional and portfolio resilience.

Over the year, we invested 5 billion dollars into opportunities aligned with the Sustainable Living trend, bringing the value of these investments to 49 billion dollars today.

At the same time, we recognise that progress on the global transition has been uneven across markets and sectors, and our portfolio decarbonisation trajectory has been affected by the shifts in the operating environment.

However, our long-term direction remains unchanged. We remain committed to our ambition of achieving net zero by 2050.

We will continue to deploy capital for a low-carbon economy, encourage decarbonisation efforts in our portfolio companies, and through partnerships across our ecosystem, enable carbon markets and other systems-level levers to bring about real-world impact.

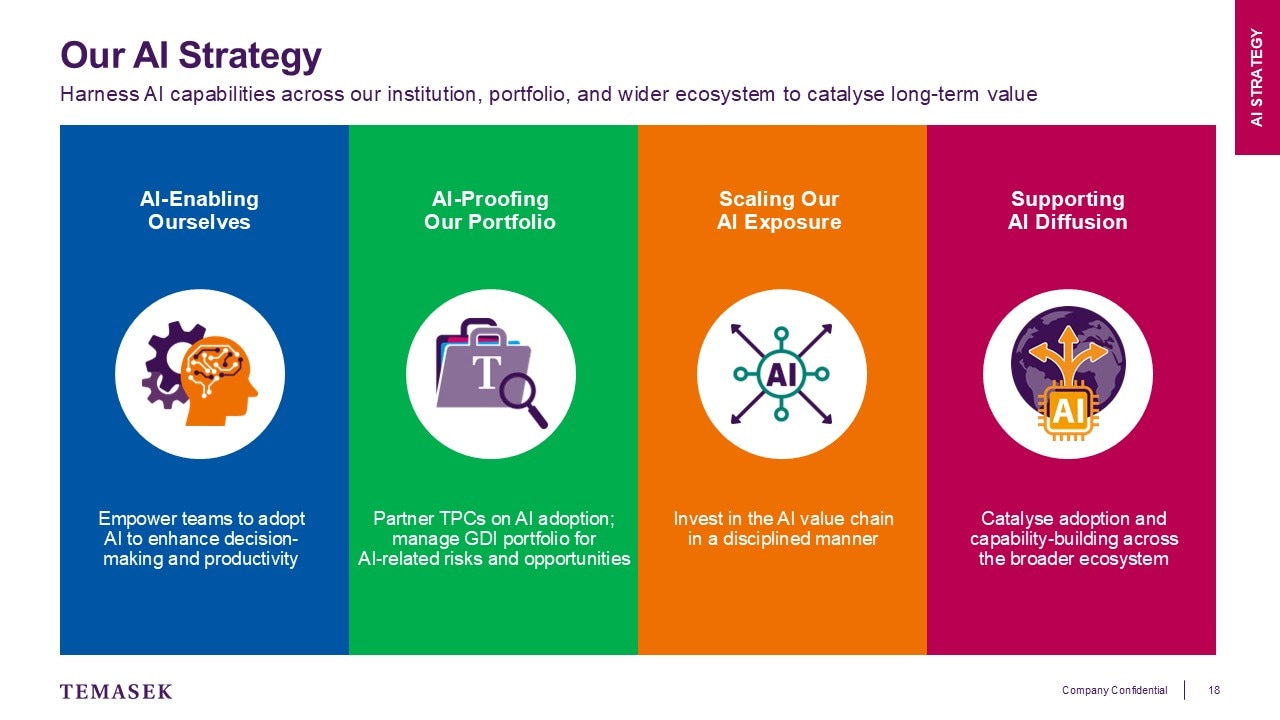

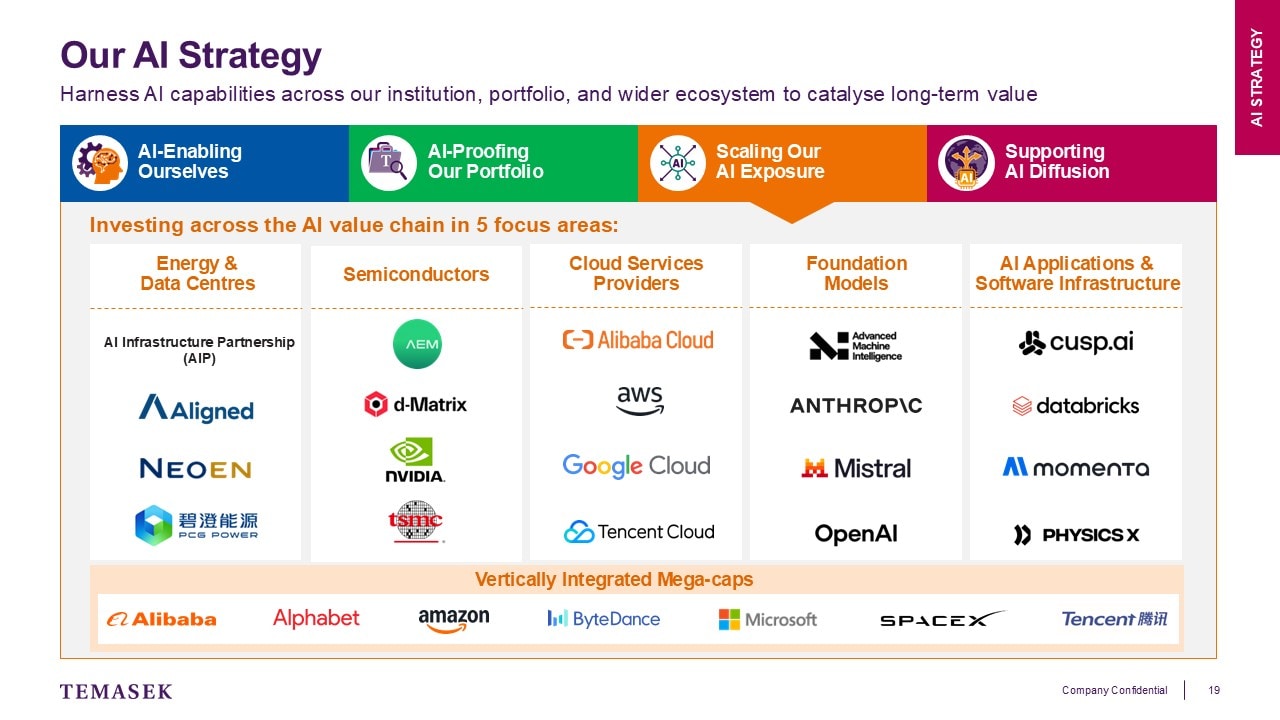

Another structural force that is reshaping economies is Artificial Intelligence.

As Dilhan said, our approach to AI is a holistic one that puts people at the forefront and centre of its adoption.

This means using AI to augment how we work and invest, helping our portfolio companies accelerate their AI transformation, scaling our exposure across the AI value chain, and supporting broader AI capability-building.

Ultimately, our objective is simple: to ensure that Temasek and our wider ecosystem is positioned to benefit from the opportunities AI creates, while navigating the risks responsibly.

Let me zoom into where we are investing.

Across the AI value chain, we invest in the underlying infrastructure that powers AI, through to the applications that ultimately create value for businesses and consumers.

In energy and data centres, we look at infrastructure-centered companies that support growing AI compute demand.

In semiconductors, we have exposure to leading enablers of AI processing and advanced computing.

In cloud services providers, we invest in businesses that provide the computing infrastructure needed to train and deploy AI models at scale.

As AI capabilities evolve, we continue to see long-term potential in foundation models.

And in AI applications & software infrastructure, we are interested in companies that are applying AI to transform industries, improve productivity, and create new business models.

We are also invested in vertically integrated mega-caps, which are large companies that have expertise in more than one of the focus areas.

Throughout today's presentation, I have spoken about our performance, portfolio resilience, and the evolving opportunities we see around the world.

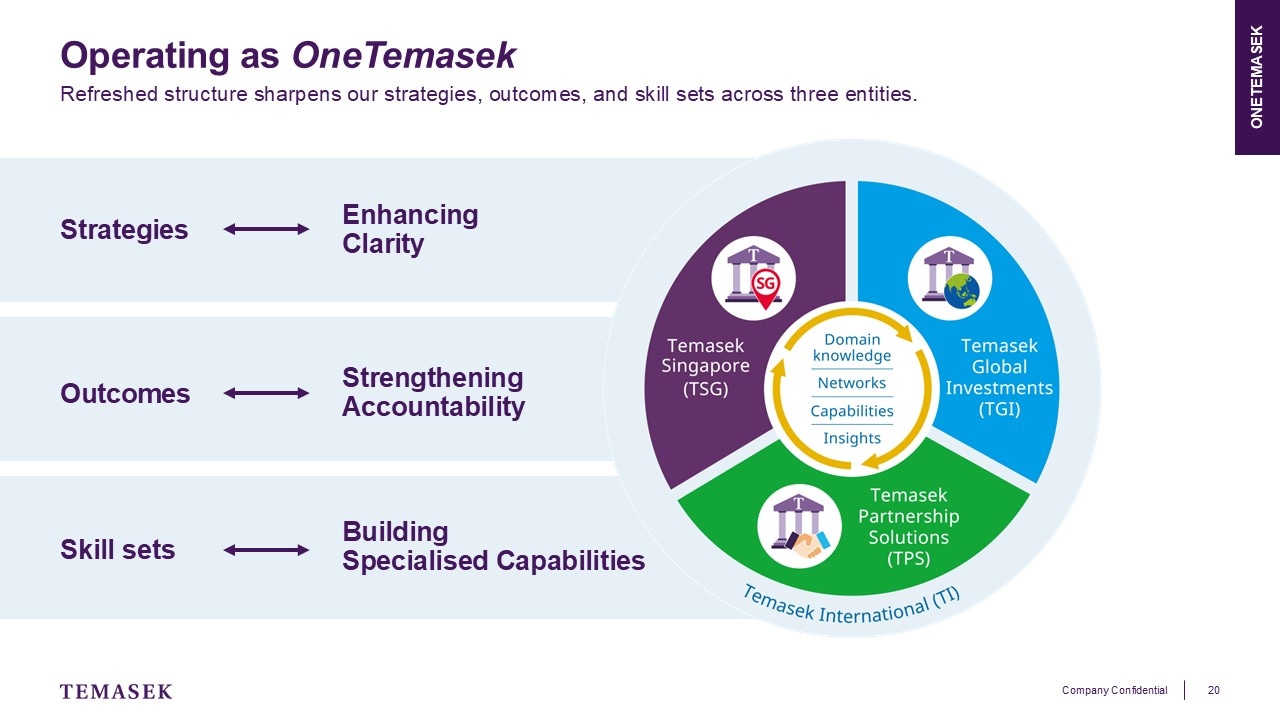

Executing effectively against these priorities requires deeper expertise, sharper accountability, and greater organisational focus.

That was the thinking behind our organisational refresh earlier this year.

We have reorganised Temasek’s investment activities into three wholly-owned entities – Temasek Singapore, Temasek Global Investments, and Temasek Partnership Solutions.

Temasek International will continue to house our group and corporate functions.

The refreshed structure will help sharpen our strategic focus and translate differentiated strategy to clarity, keep each entity accountable in delivering against distinct outcomes, and deepen specialised skill sets and build capabilities that will value add to our organisation.

However, one thing remains key: Temasek will continue to operate collectively as OneTemasek.

We will draw on shared capabilities, networks, and insights across the organisation to pursue opportunities and manage risks holistically.

Before I conclude, let me briefly share how we are thinking about our key markets.

Starting first with Singapore.

We remain confident in the market’s resilience. While global uncertainty and energy-related disruptions continue to pose risks, Singapore remains well-positioned with strong fundamentals and policy flexibility.

For Temasek, our focus remains on actively stewarding our TPCs, strengthening their competitiveness and resilience for value creation over the long term.

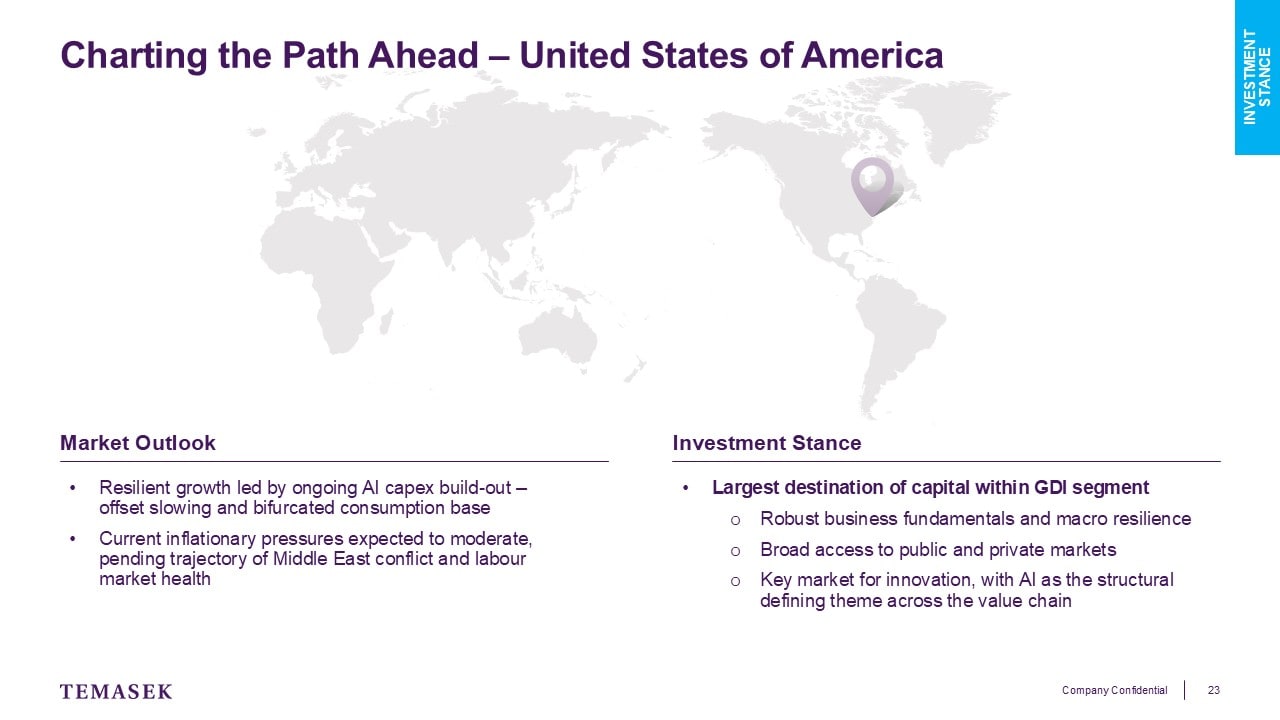

Moving on to the United States.

We see resilient growth in the market and it remains the largest destination of capital within our GDI portfolio.

We see attractive opportunities given its leadership in innovation, particularly across the AI value chain, supported by deep public and private capital markets.

At the same time, we remain disciplined on valuations and risk.

In China, we remain committed as a long-term investor.

While exports have been strong, particularly in technology and AI-related sectors, recovery in domestic consumption remains uneven and not yet broad-based.

We continue to see compelling opportunities in areas where innovation is accelerating, including biotech, robotics, AI-related technologies, and advanced manufacturing.

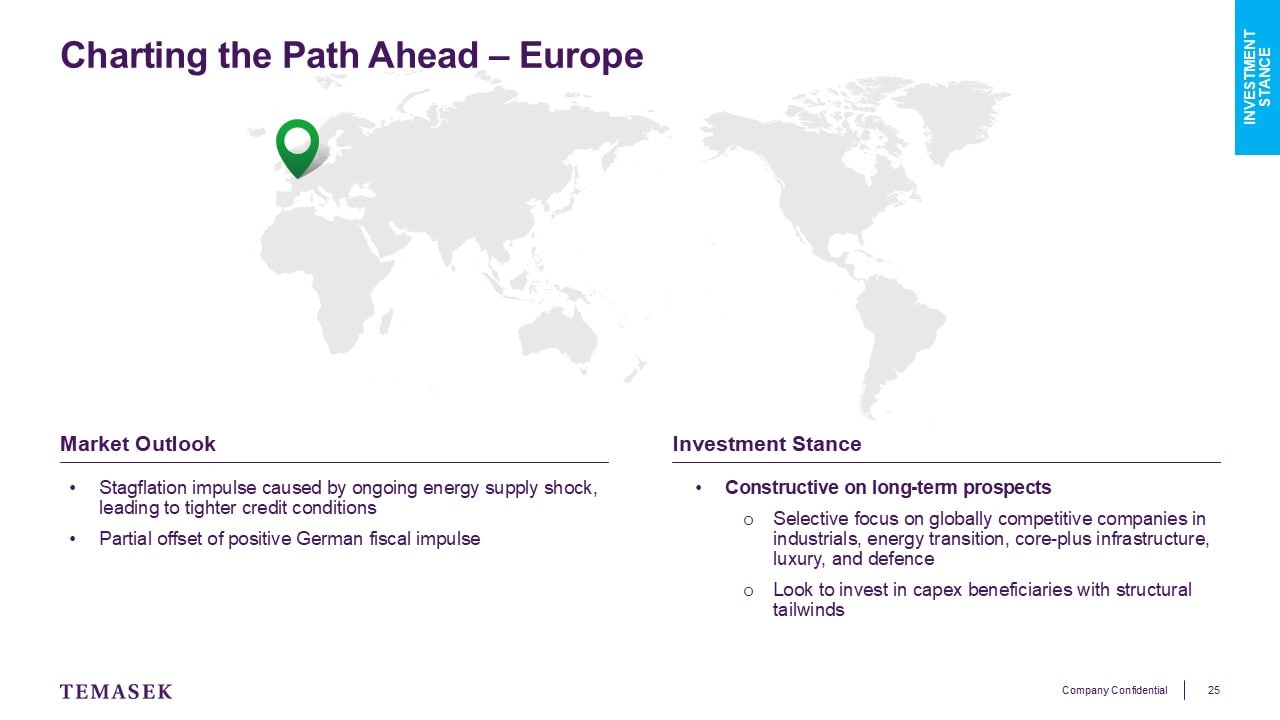

On to Europe.

The environment remains challenging in the near term, but we see selective opportunities in globally competitive companies with structural tailwinds.

Areas of interest include industrials, energy transition, infrastructure, and defence, as well as businesses that benefit from long-term capex trends.

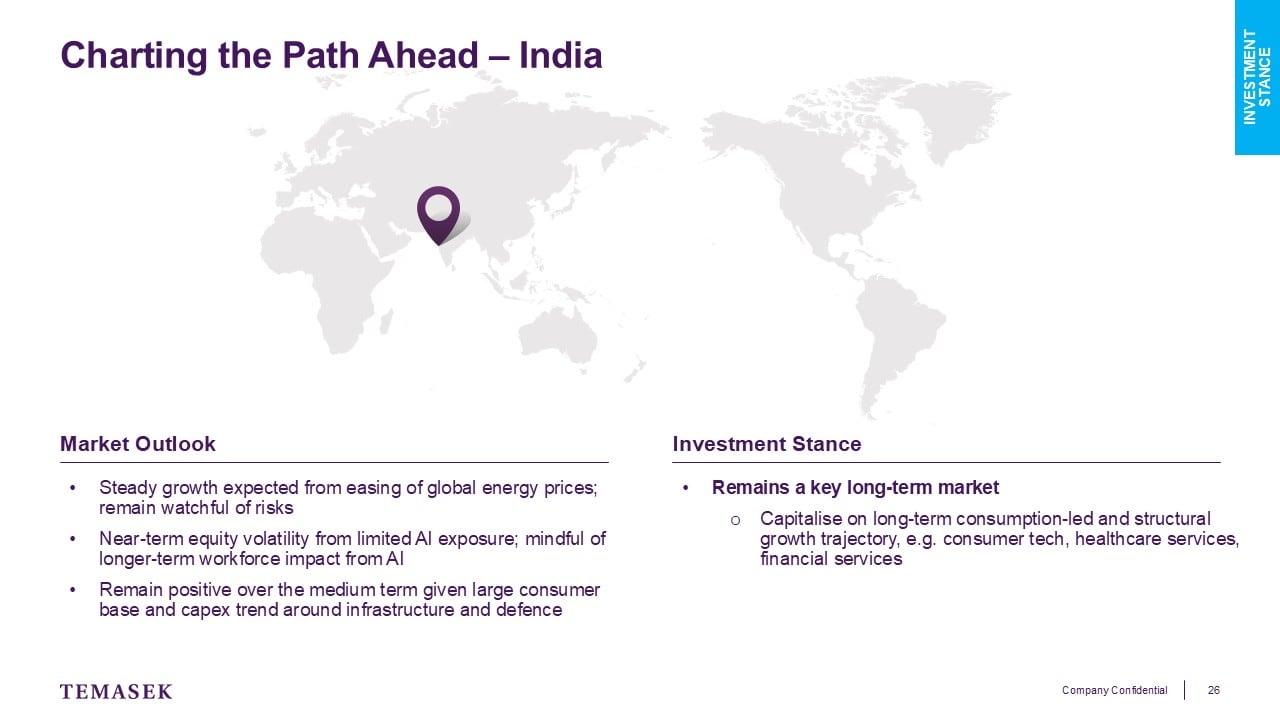

Moving on to India.

India remains an important long-term market for us.

While near-term equity volatility and energy-related pressures may persist, we are constructive on the country’s structural growth outlook – supported by its large consumer market, infrastructure development, and growing middle class.

Our focus is on capturing opportunities in sectors such as consumer, financial services, and healthcare, where underlying structural growth trends remain strong.

Nearer to home in Asia Pacific excluding China and India.

Here, opportunities vary by market.

We remain selective and focused on sectors aligned with our structural trends, including technology, consumer, and healthcare. Specifically, within Japan and Korea, we will focus on partnering local champions and private equity firms.

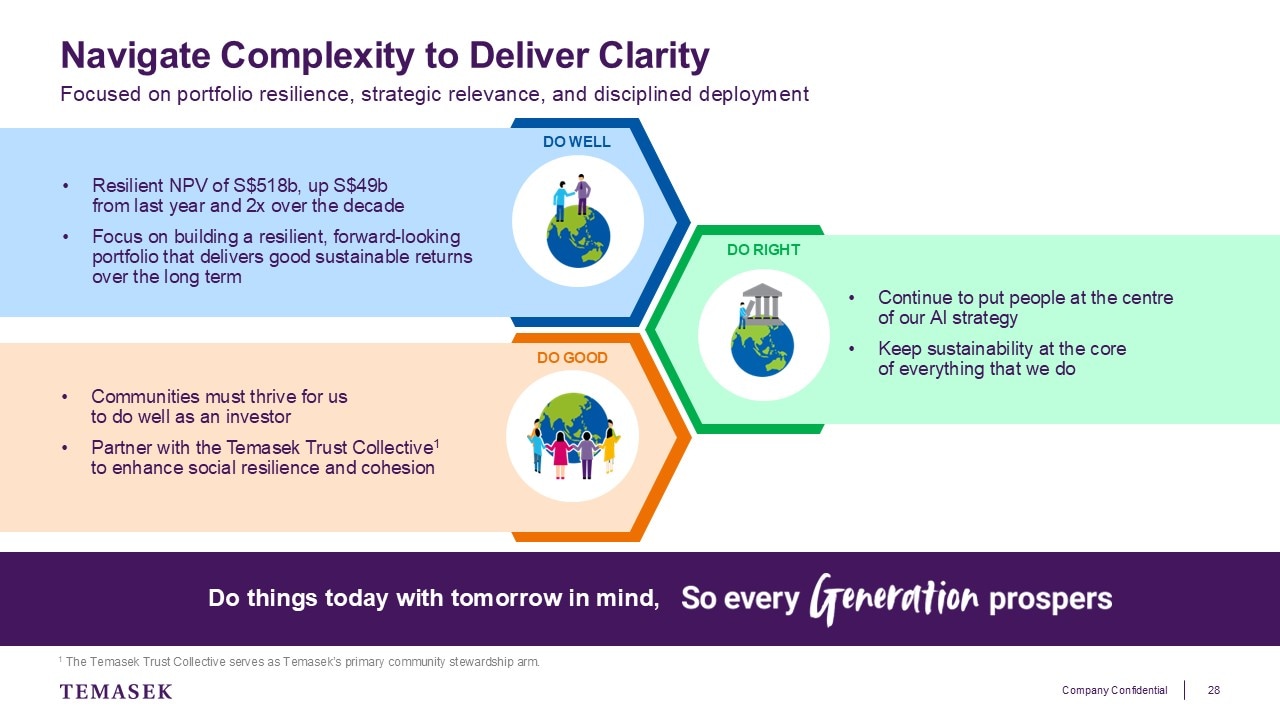

As we reflect on the year, our theme “From Complexity to Clarity” has guided us on our response to an increasingly challenging environment.

We are focused on building a portfolio defined by portfolio resilience, strategic relevance, and disciplined deployment.

This is reflected in how we seek to deliver good sustainable returns over the long term. We ended our last financial year with a resilient Net Portfolio Value, and will continue to focus on enduring value creation across our three portfolio segments.

At the same time, we are committed to doing right as an institution by putting people at the centre of how we approach AI and embedding sustainability at the core of everything that we do.

Last but not least, we strive to do good by the wider community that we operate in.

Through the Temasek Trust Collective, we support communities, build capabilities, and strengthen social resilience.

Ultimately, we are guided by a simple yet enduring ethos of doing things today with tomorrow in mind, so every generation prospers.